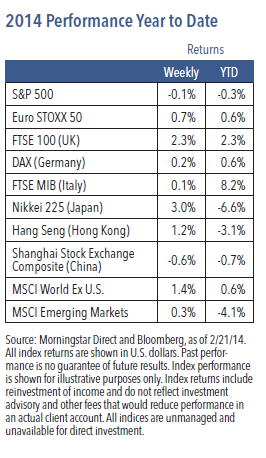

U.S. equities finished mixed after the shortened holiday week.¹ The broad market narrative did not change, as additional disappointing economic data was largely attributed to the impact of adverse weather. Comfort that the recovery may be gaining traction was evidenced through Fed discussions and the January FOMC minutes, with consensus expectations for tapering to continue at a measured pace. Some renewed concerns about a growth slowdown in China surfaced but had little impact.

Weakness May Be an Overhang, but Fundamentals Appear Intact

Weaker-than-expected economic data has not accelerated fears about the recovery slowdown that weighed on stocks in late January and early February. The recent reprieve has primarily been due to extremely adverse weather that will probably distort the data over the near term. Softer activity data is anticipated to continue and can be seen as a greater-than-expected payback for the strong inventory and capex in the second half of last year. Our view is that the economic expansion is mid-cycle, marked by a time of stationary growth expectations. We think more emphasis should be placed on where the economy is in the business cycle, rather than simply trying to anticipate GDP growth for next quarter.

Weekly Top Themes

1. The earnings per share growth rate of more than 8% for the fourth quarter has been strong.² Approximately 90% of the S&P 500 companies have now reported earnings. Top and bottom line growth trends are positive and support our forecast for growth acceleration in 2014. The S&P 500 appears to have broken out of the nearly flat revenue per share growth that stretched for five quarters during 2012 and 2013, and earnings per share has followed suit.

2. Ukraine should not cause financial or economic contagion because of its smaller relative size in the broader global economy and markets. The country has been mismanaged for so long that it is unlikely to be a catalyst for global risk. The only concern would be if Ukraine becomes a venue for new confrontation between Russia and the West.

3. The anticipated M&A boom could begin. Favorable signals include recession- like nominal GDP, vast cash reserves on corporate balance sheets and a growing activist investor base.

The Big Picture

After several weeks of a risk-off environment, conditions have been less negative but remain choppy. The overall backdrop in the developed world is unchanged, despite abnormal weather resulting in lackluster economic data in the U.S. and weakness in parts of Europe. We maintain a relatively upbeat economic and earnings forecast for the developed world, based on trends in leading economic indicators, hiring plans and profits. This assumption, combined with pro-growth central banks in the major economies, leads to our cyclically positive stance on equities and negative outlook for bonds, as well as a mildly positive view for the U.S. dollar.

The Great Recession resulted in substantial spare capacity in global product and labor markets that has not yet been absorbed because of the subdued economic recovery in recent years. The key to ensuring a successful transition to a more sus- tainable economic expansion and higher earnings conviction is for central banks to avoid pulling away the punch bowl prematurely. Outside of a handful of troubled emerging market nations, no major country has taken steps to increase interest rates nor encouraged a stronger currency. The Fed, the European Central Bank, the Bank of Japan and the Bank of England are all determined to lag the economic recovery, which bodes well for equities but negatively for bonds.

Forward P/E multiples in the U.S. have expanded by more than 25% over the last two years,³ and earnings growth must now justify this expansion. The good news is that a turning point in profitability seems to have arrived. The bad news is that the loss of momentum in many economic indicators could present an obstacle to the earnings recovery. It may take until the spring thaw to ascertain the pace of the confusing economy and markets.

1 Source: Morningstar Direct, as of 2/21/14. 2 Source: FactSet, “Earnings Insight,” February 21, 2014. 3 Source: FactSet, as of 2/21/14.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuations, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliateof Nuveen Investments, Inc.

GPE-BDCOMM4-0214P