Choppy Week Focuses on Fed

Domestic economic data was largely of the disappointing variety, but economists were quick to cite bad weather as the key culprit. The largest swings in equity markets came on Wednesday and Thursday. Minutes from the latest Fed meeting dragged markets lower on Wednesday, as there was an indication that interest rates could rise sooner than anticipated. On Thursday, however, markets rallied on news of a major acquisition by Facebook.

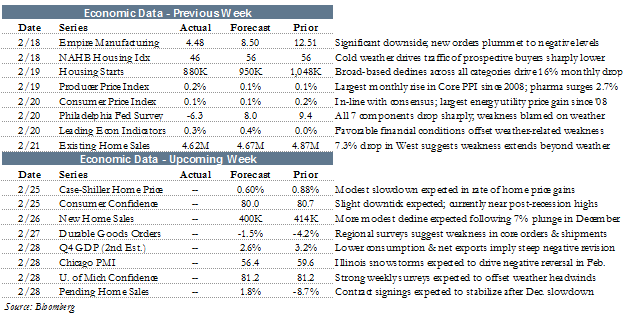

On the domestic front, data surrounding housing starts and existing home sales was notably weaker in January. On a seasonally adjusted annual basis, existing home sales came in at 4.6 million in January, down from 4.9 million in December. It was the latest in a series of slowing monthly figures, and economists quickly placed blame on the poor weather conditions throughout the country. That is partially true, but some of the steepest year-over-year sales declines occurred in the West, which was noticeably free of the polar vortex. More likely is the spillover impact from increased mortgage rates that we saw in the middle of 2013.

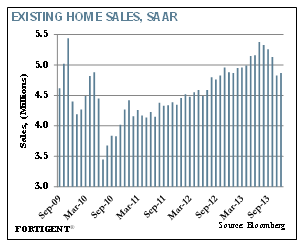

Weather did play a prominent role in housing starts during January. Overall starts dropped from 1.04 million in December to 880,000 in January, with regions such as the Midwest down 47% in the past twelve months.

The latest reading on inflation continues to paint a muted picture of prices. The consumer price index increased 0.1% in January and is up 1.6% in the past year. Within the sub-components, a consistent theme is beginning to emerge. In January, the cost of goods declined 0.1%, and is now down 0.3% year-over-year. That contrasts with services, which posted a 0.2% gain and are up 2.3% in the year-over-year period.

On Wednesday, minutes from the January FOMC meeting left markets mildly surprised. The surprise was due to chatter from “a few” individuals that a change to forward guidance on the fed funds rate could occur within the next several months. That raised the possibility of interest rate hikes coming sooner, rather than later, and spooked market participants. During an interview at the end of the week, Federal Reserve Bank of St. Louis President James Bullard was quick to mention that his previous estimation of a 2014 rate hike is likely to move to 2015 because of recent weather-induced weakness.

Time To Worry About Europe Again?

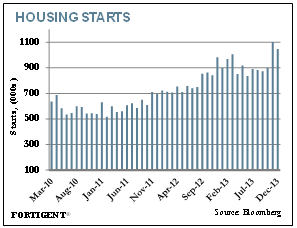

The European sovereign debt crisis has all but faded from investors’ minds since ECB President Mario Draghi’s famous pronouncement on July 26, 2012 that he would do “whatever it takes” to save the monetary union. Since that time, equity markets in Europe rallied sharply as accumulated risk aversion fell away.

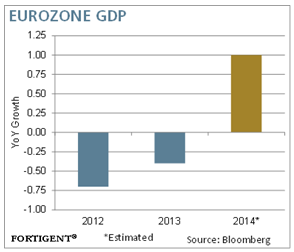

Markets climbed despite rather tepid growth from the Europe block; in fact, the monetary union remained mired in a record-long 18-month recession until mid-2013. Economists are more sanguine about the region’s prospects in the coming year, with calendar year 2014 GDP expected to grow 1.0%, according to a Bloomberg poll of economists.

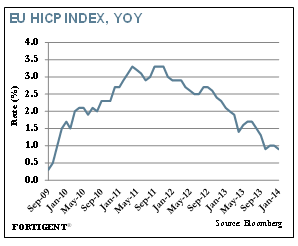

But are those expectations well-founded? As we have noted in recent months, a troubling emergence of disinflation is gripping the region, sparking fears of a deflationary spiral. In January, Europe’s HICP (harmonized index of consumer prices) fell 1.1% month-over-month, and stands at 0.8% year-over-year. That is down from 2.0% levels just twelve months ago, and is the second lowest reading of the past 4 years (behind only October’s 0.7% figure). Sub-one percent inflation is certainly far below the 2.0% target sought by the central bank.

Officials in Europe have largely dismissed these concerns as cyclical in nature. Unlike the Fed, which aggressively purchased assets to stem a disinflationary trend in the US following the financial crisis, the ECB has not engaged in quantitative easing. Indeed, such a practice is forbidden by the ECB’s own statutes, and members like Germany have staunchly opposed monetizing the profligacy of the peripheral nations.

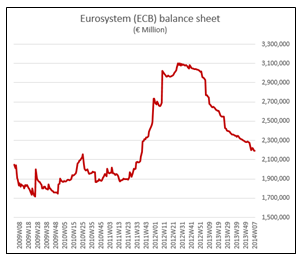

As the research shop Sober Look notes, “while the ECB has been on the sidelines, the balance sheet of the Eurosystem has been contracting fairly sharply – all in the face of unusually tight credit conditions.” Thus, liquidity conditions provided by the European Central Bank stand in stark contrast to the United States, which has seen an unprecedented expansion of its balance sheet. This may be contributing to the Eurozone’s lack of credit growth and, in turn, economic activity. Loans to euro area households and non-financial corporations stand at their lowest levels in years.

Source: Sober Look

There is concern that the ECB is doing too little to combat this very serious problem of disinflation – the precursor to deflation. Thus far, the bank has quieted fears of a systemic collapse via the simple promise of backstopping the financial system. Even November’s modest benchmark interest rate cut of 25 bps was largely seen as symbolic. But with organizations like the OECD calling for the ECB to begin quantitative easing, further declines in the rate of inflation may compel the ECB to produce tangible action, rather than make empty promises.

On Friday, investors receive their first look at the “flash” estimate for February. Barclays Research expects that figure to come in at 0.6% year-over-year, which would be the lowest level of price increases observed since shortly after the financial crisis. With Japan serving as a roadmap for the devastating effects of deflation over the past two decades, investors comforted by the famous Draghi bumblebee speech should recognize the difference between posturing and action. While European officials have thus far been effective with the former, how they stack up on the latter may ultimately decide the fate of the region.

The Week Ahead

It is likely to be a busy week around the globe, with domestic data on home prices, consumer confidence, new home sales, durable goods, and 4th quarter GDP being released.

Outside the U.S., inflation data is released in Europe and Japan, along with manufacturing data in China.

Earnings season is winding down, but markets will closely watch results from Best Buy, Gap, Home Depot, JC Penny, Macy’s, and Target.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value