Having spent a large proportion of my career prior to joining GMO working at investment banks, I’m well aware of what Andrew Smithers describes as “Stock Broker Economics,” the second tenet of which is “The market is always cheap.”1 Over the years I’ve witnessed many attempts by the practitioners of this most dark art to justify why tried and tested measures of valuation are no longer meaningful, or occasionally create new measures of valuation that purport to show the market to be cheap.2

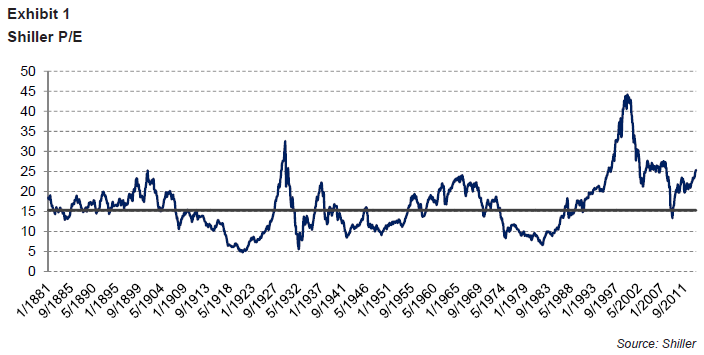

A recent outbreak of precisely this brand of sorcery has surrounded the Shiller P/E (price relative to 10-year moving average earnings adjusted for inflation as shown in Exhibit 1). Wizards range from the seemingly ever optimistic Jeremy Siegel to any number of Wall Street strategists, and even a blogger whose work I generally enjoy.3 Given that one should always look for evidence that may prove one wrong, I’ve spent some time thinking about the issues they have raised and have summarized my thoughts in this short paper.

One of the criticisms of Shiller’s Cyclically Adjusted P/E (CAPE) that I’ve come across is that it hasn’t given a cheap signal in a long time; that is to say that it has not mean reverted of late.

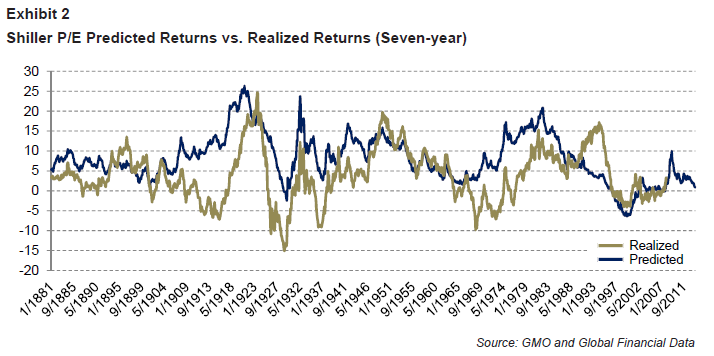

I am, however, less than convinced by this argument. There is nothing contradictory between the predictions based on the Shiller P/E and the returns that we have witnessed. Exhibit 2 shows the simplest way that I can imagine of transforming the Shiller P/E into a forecast return. We simply revert the P/E towards average over the course of the next seven years and then add a constant to reflect growth and income (let’s call it 6% for simplicity’s sake). It does a pretty reasonable job of capturing realised returns. If anything, it tends to overpredict returns, rather than underpredict them (which is another of the charges levelled by the critics).

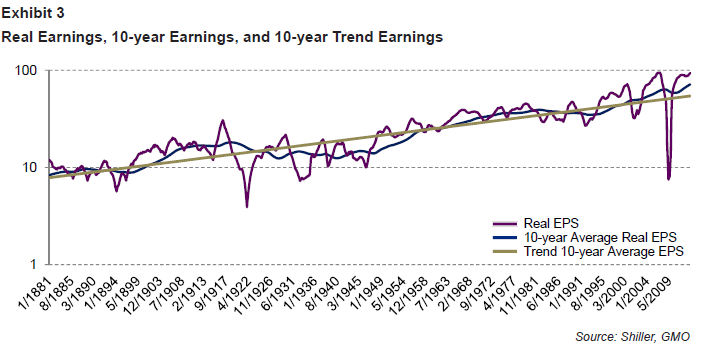

I’d actually suggest that the Shiller P/E is quite possibly too optimistic currently (the complete opposite of the critics’ claim). This is because 10-year earnings are currently high relative to their trend. Exhibit 3 shows real earnings, their 10-year average, and a trend line fitted through the 10-year average. Real earnings are currently massively above their 10-year average (accounting for the difference between the spot P/E and the Shiller P/E). However, 10- year average earnings are also significantly above their trend, suggesting that earnings have been above average for a prolonged period (more on this a little later).

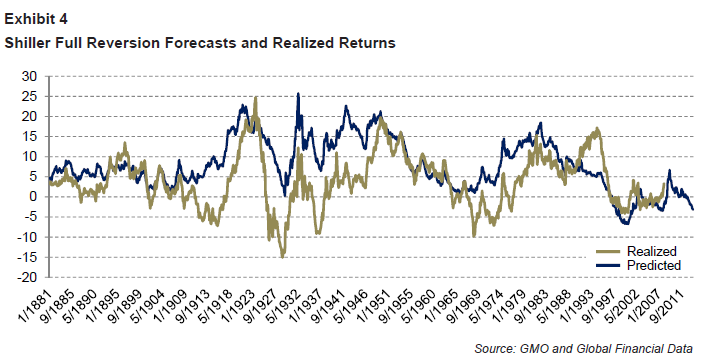

If one were to use 10-year trend earnings rather than current trailing 10-year earnings, the P/E would rise from 25x shown on the Shiller measure to 34x (see Exhibit 4). This trend measure actually has a better relationship with realised returns than the straight Shiller P/E. That is to say that some of the overprediction of the Shiller P/E has been caused by 10-year average earnings being inflated.

Another current criticism of the Shiller P/E is that the impact of goodwill impairment accounting (FASB 142) has led to a situation in which earnings are much more volatile than has been the case historically, thus invalidating the earnings series that underpins the calculation.

To some extent this criticism is already rebutted by the analysis above: 10-year average earnings are significantly above their trend. This is not suggestive of a situation whereby average earnings are being dragged down by the very low numbers recorded during the Global Financial Crisis. Much as it is tempting for those of a bullish nature to focus on the extent of the drawdown in earnings in 2008, they happily ignore the peak levels of earnings seen before the crisis, or indeed the rapid recovery in earnings (helped as it was by the suspension of FASB 157 on financials’ mark-to-market assets). This is why we average – it smooths out the highs and lows.

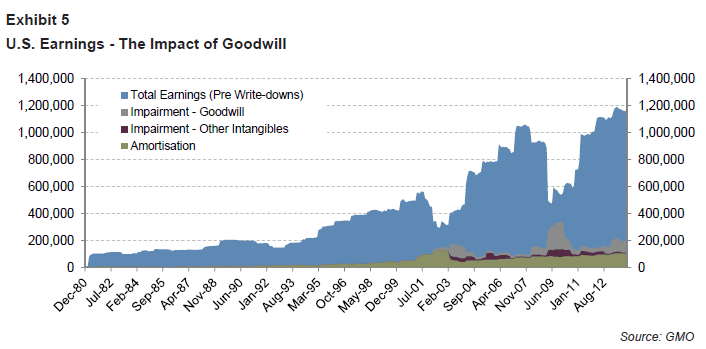

Before we head into some proposed solutions to the problems raised, I’d like to take a quick detour into some work that my colleague Simon Harris has been doing on understanding earnings and balance sheets. In the course of that work Simon examined the role of goodwill impairment in the collapse in earnings seen during the Global Financial Crisis. Exhibit 5 shows a summary of his findings with respect to the U.S. Look at the grey area, which represents the sum of earnings before any goodwill or other intangibles are written down or amortised (for our U.S. universe). They collapsed by about 60%. Ergo, much of the earnings collapse had nothing to do with FASB 142!

However, let us put this to one side for now, and instead consider one of the proposed “solutions”: to replace the GAAP reported earnings series with National Income Product Accounts (NIPA) profits. This strikes me as an odd move on many levels, not least of which is the fact that NIPA covers about 9000 companies of just about every shape and size compared with the narrowly focused 500 names within the S&P.

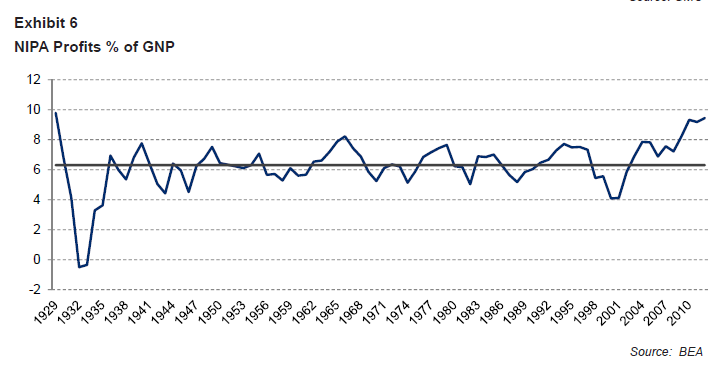

As I have discussed before,4 NIPA profits are at record highs, and have been significantly elevated for a prolonged period. As such, using NIPA earnings embeds a very high profit margin assumption into the valuation framework. Over the last 10 years profit margins from NIPA have averaged 8% of GNP, compared to the long-term average of 6% (see Exhibit 6).

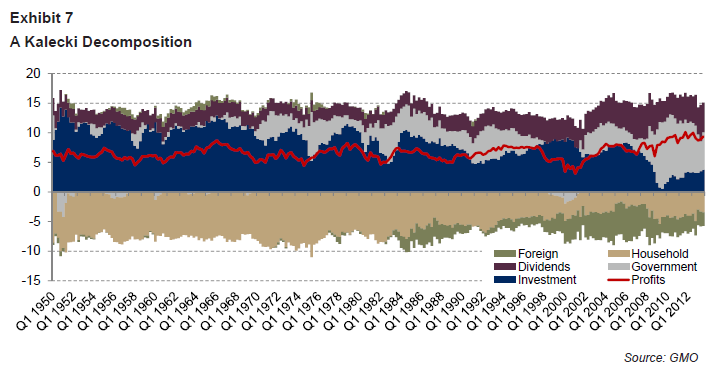

As regular readers know, we favour the Kalecki profits equation for thinking about the sources of the very high profits margins. This equation says that profits are the result of net investment plus dividends minus savings (carried out by some combination of the household, government, and foreign sectors).

Exhibit 7 shows the breakdown of profits into various components. As we have written before, in the wake of the Global Financial Crisis net investment collapsed and has only recovered very slowly. The key reason profits have held up is because of fiscal deficits run by the government. Given that the deficit is “forecast” by such august bodies as the Congressional Budget Office to decline significantly over the next few years, it will take either a remarkable recovery in investment spending or a significant re-leveraging by the household sector to hold margins at the levels we have witnessed of late.5 Thus, embedding such high margins in a valuation seems optimistic to me.

I suspect that the rationale for suggesting replacing GAAP as reported earnings with NIPA earnings is that NIPA earnings track profits from current production and as such ignore capital gains and losses from M&A activity and write-downs from bad debts (they look more like so-called “operating earnings”). Let me put aside my concerns about the validity of using NIPA as the basis of a valuation approach and instead look at what doing so shows.6

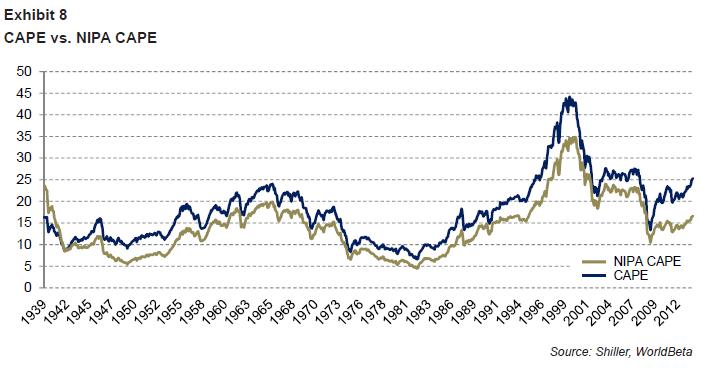

Exhibit 8 represents an attempt to reproduce the approach that Jeremy Siegel has proposed in which NIPA earnings are deflated by share issuance to make them comparable to the per share concept of earnings used in the Shiller methodology. The chart shows the standard Shiller P/E and the NIPA-based P/E. The NIPA-based CAPE is almost always lower than the more familiar Shiller P/E. The mean for the Shiller P/E over this sample is 18x, whereas the NIPA CAPE has an average of 14x. Therefore, we shouldn’t be surprised that the current NIPA CAPE is below the Shiller P/E. The current standard Shiller P/E is at 25x and the NIPA CAPE is at 17x. Regardless of which measure is used, both are above average. Yes, the NIPA CAPE shows less overvaluation than the standard Shiller P/E, but it is an open question as to how much faith one should have in this finding given the odd mix of variables used in its construction.

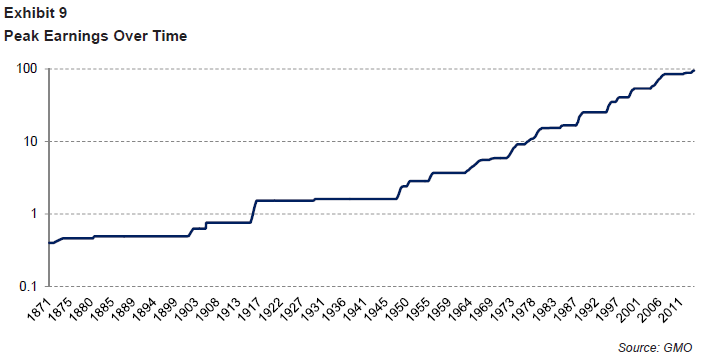

There are, however, alternative ways of dealing with some of the issues raised by CAPE critics without resorting to using NIPA earnings to create something of a Frankenstein’s Monster of valuation. For instance, a really simple approach is to price equities on the basis of their peak earnings. The first time I came across this approach was in the work of John Hussman, so I’ll call this a Hussman P/E.

The idea is actually beautifully simple (like almost all good ideas): take the peak earnings level over the past cycle as the basis for valuing equities. Peak-to-peak earnings should nicely capture the trend in earnings over time. The measure is optimistic because it assumes that peak earnings will once again be recaptured (obviously not valid at the individual stock level, but a pretty good assumption at the market level thus far).

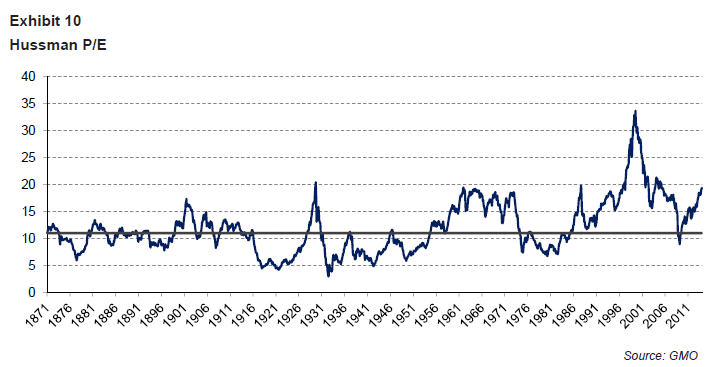

The advantage of this approach is that it avoids all the concerns over goodwill issues and write-downs, since we only care about the peak level that earnings attained (see Exhibit 9). Exhibit 10 shows the Hussman P/E over time. The average is 11x, the current reading is over 19x. Again, this suggests that U.S. equities (as represented by the S&P 500) are significantly overvalued.

Just as before, we can turn this signal into a return expectation by reverting the valuation to its average over the course of the next seven years, and then adding 6% to allow for the contribution of growth and dividend yield. This would give a current forecast of -0.6% p.a. in real terms over the next seven years.

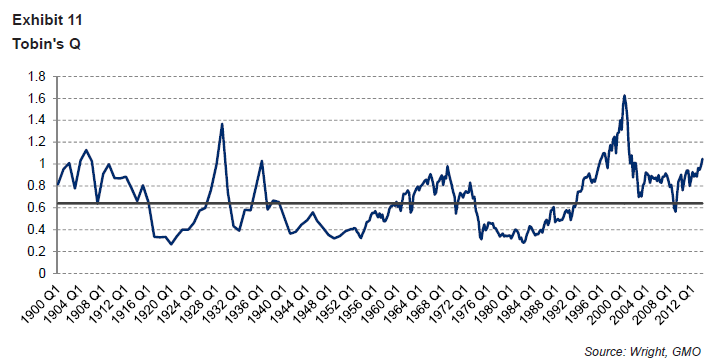

As a final check on these models we can turn to a model that doesn’t use earnings at all – Tobin’s Q,7 which compares the market value of companies to their replacement cost (Exhibit 11). This measure has its roots in Keynes’s Chapter 12 of The General Theory of Employment, Interest and Money in which he writes “For there is no sense in building up a new enterprise at a cost greater than that at which a similar existing enterprise can be purchased; whilst there is an inducement to spend on a new project what may seem an extravagant sum, if it can be floated off on the Stock Exchange at an immediate profit.”

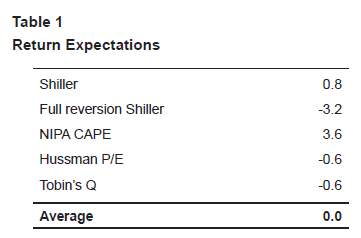

The table below shows the five models that have been presented in this paper converted in this way into total return expectations over the next seven years. They range from the most optimistic NIPA CAPE, with an expected real return of 3.6% p.a., to the version of Shiller, which incorporates a full mean reversion in 10-year earnings back to their normal trend, with an expected real return of -3.2% p.a. Across the five simple models presented here the average is zero. If one were to exclude the theoretically dubious NIPA-based CAPE, then the average drops to almost -1% p.a.

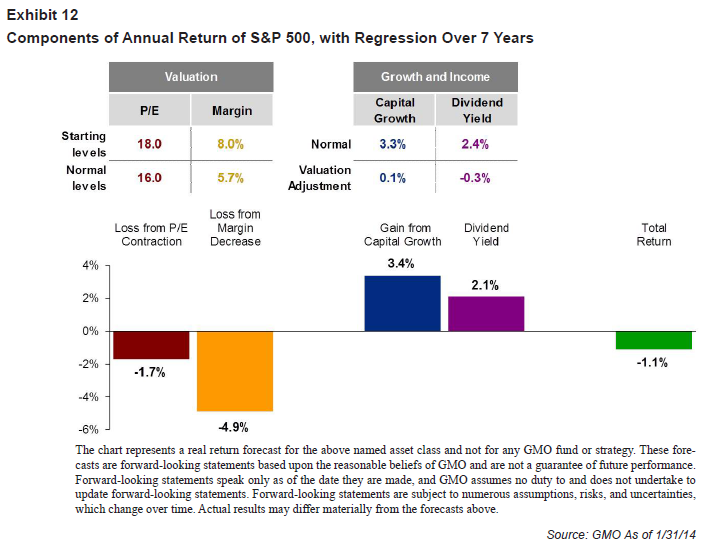

In our actual valuation work we use a variety of different models to estimate real expected returns. One of those is indeed the Shiller P/E, but it is the most optimistic model we use. The others are more cautious, because they essentially fully revert margins back to “normal,” whereas the Shiller model simply takes whatever is embedded in the most recent 10-year period. As a general rule we average across the various models we use to generate our best forecast as to where real returns are likely to head, rather than relying upon one signal model (without exceptionally good reason). Doing so currently results in our expectation of a -1.1% real return for the S&P 500 over the next seven years (see Exhibit 12). We continue to believe that the weight of valuation evidence suggests the S&P 500 is significantly overvalued at its current levels. Some call us “valuation bears”; we argue that we are simply valuation realists!

1 The first tenet is “All news is good news.”

2 Who can forget the insanity of eyeballs and clicks as indicators of valuation!

3 Philosophical Economics Blogspot.

4 J. Montier, “What Goes Up Must Come Down,” January, 2013. This GMO white paper is available to registered users at www.gmo.com.

5 At some point in the future I’ll write a paper on how the Kalecki equation encompasses many of the “explanations” we hear for high profit margins. Stay tuned.

6 A serious hat tip to Mebane Faber and Kip McCauley who provided me with an interpretation of what Jeremy Siegel has been using

7 This should arguably be called Kaldor’s V as he published it before Tobin (1966 vs. 1968).

Mr. Montier is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2009, he was co-head of Global Strategy at Société Générale. Mr. Montier is the author of several books including “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance; Value Investing: Tools and Techniques for Intelligent Investment”; and “The Little Book of Behavioural Investing.” Mr. Montier is a visiting fellow at the University of Durham and a fellow of the Royal Society of Arts. He holds a B.A. in Economics from Portsmouth University and an M.Sc. in Economics from Warwick University.

Disclaimer: The views expressed are the views of Mr. Montier through the period ending February 25, 2014 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security. The article may contain some forward looking state- ments. There can be no guarantee that any forward looking statement will be realized. GMO undertakes no obligation to publicly update forward looking tatements, whether as a result of new information, future events or otherwise. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to securities and/or issuers are for illustrative purposes only. References made to securities or issuers are not representative of all of the securities purchased, sold or recommended for advisory clients, and it should not be assumed that the investment in the securities was or will be profitable. There is no guarantee that these investment strategies will work under all market conditions, and each investor should evaluate the suitability of their investments for the long term, especially during periods of downturns in the markets.

Copyright © 2014 by GMO LLC. All rights reserved.

© GMO