With this recovery, prosperity has always been just around the corner. It wasn’t supposed to be this way. True, the massive fiscal and edgy new monetary measures enacted in the wake of the 2008 crisis kept the economy’s heart beating. The Fed deftly executed its role of lender as last resort, and for this we should all be grateful. What has become steadily less clear is why, five years after the crisis, the Fed remains committed to its zero rate policy. Are artificially low rates truly the secret sauce that takes a weak recovery and makes it strong?

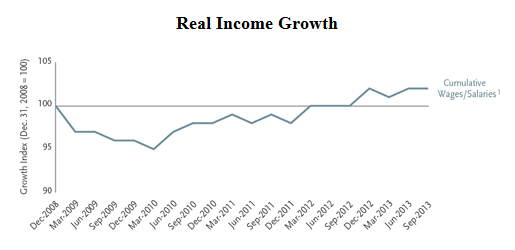

The Fed’s recipe for recovery has been predicated on the Keynesian principle that boosting aggregate demand is a recession cureall. By setting rates low, the Fed “stimulates” credit creation which begets more spending which supposedly lifts national income. For this reason, the Fed has understood its job as one of keeping the credit aggregates growing until the “animal spirits” recover from their 2008 trauma. Trouble is, even a cursory glance at equity and real-estate prices ought to convince any skeptic that investors are nothing if not “spirited.” Yet, all the sound and fury stirred up on Wall Street contrasts sharply with the stagnant wages and incomes on Main Street. Exactly what kind of “recovery” do you have without rising incomes? Not a durable one.

Source: BEA, TCW

1 Including employer contributions for employee pension and insurance funds and for government social insurance.

Empirically, we’ve lived with five years of extraordinary “stimulus” and that stimulus has done much for asset prices and precious little to raise incomes. No matter how “inspired” an individual might be, you can’t spend what you don’t earn. Want earnings to rise and jobs created? We all do. Then properly incentivize the business owners, entrepreneurs, and employees who are the economy’s actual innovators and productivity enhancers. In a market economy, growth flows most naturally from grass roots decision makers, not from grandiose centrally planned epiphanies. Firms and individuals need interest rates and asset prices that are reflective of the realities of the actual economy. However, rather than concentrate on normalizing rates to market levels, the Fed has targeted aggregate spending. More spending means more income, so says the Fed. Alas, the Fed’s causation is reversed: your spending rises in proportion to your income growth, not the other way around. No individual or business can thrive by using leverage to expand his spending, unless that current period spending results in a proportionate economic return in a later period. This truth is as applicable to the individual as it is to a whole society. Using debt to finance consumption will, over time, impoverish a society as surely as it will an individual. You sow before you can reap. But, the Keynesians maintain, everybody’s spending is someone else’s income, so go forth and spend what you have. Then, borrow so you can spend what you don’t have. If everyone would just do this, so the thinking goes, the economy would soar.

The thinking is as specious as any that promises a free lunch. “Stimulus” is all about lowering rates to below market levels. Artificially low rates lead to artificially high asset prices. False asset prices send false signals that cause individuals and businesses to make inefficient decisions. “Wrong” stock prices in 2000 and distorted real-estate values in 2006 did not promote enduring recoveries in their time. Neither will today’s zero rate regime. Market based pricing of rates may not be perfect, but it is more trustworthy than Fed based pricing.

Why is this? The market is comprised of millions of decision-makers who “own” the fragmented and specialized real-time knowledge we call “the economy.” The Fed “owns” econometric models which know the relationships between what did or didn’t happen when rates were here or there or asset prices did this or that. Which would you rather trust: an econometric model that purports to understand what is happening in our complex ever-changing economy or a market system armed with an aggregation of specialized knowledge that franchises success and bankrupts failure? Neither will be perfect, but the market system can self-correct in a way that a model never can. Importantly, even the very best econometric model cannot understand the subjective human dimension to decision-making. Individuals are not inert automatons whose preferences can be predicted or even reliably described by historical regressions. Rather, people are self-aware, active decisions-makers whose preferences shift and evolve in ways that may not always be fully comprehensible even to the individual himself. No model can get inside your mind and “know” what you are going to do about the fact that the stock market went up by 30% last year. Cash in your chips? Stay for the ride? Buy a car? Save it for retirement?

Alas, monetary policy is not magic and rate setting is a blunt instrument. While the Fed can control the quantity of credit created, it cannot ensure that the credit is put to good use. Our recovery remains weak not because of some quantitative failure by the Fed to sufficiently expand the aggregate supply of credit. Rather, the subpar recovery has resulted from a qualitative failure of the broader economy to efficiently utilize the credit that has been created owing to its systematic mispricing by the Fed. As a result, too little of the credit created has gone into productive, job creating endeavors and far too much has been used for consumption, mal-investments, and in support of an asset price inflation. Rather than piling on still more “stimulus,” the economy needs credit pricing to converge back towards proper market levels so that it is used most productively. No market clears at zero and hence mispricing credit is tantamount to pretending that real capital resources are more abundant than they actually are. The sooner we return to some semblance of market based pricing of credit, the more we ensure that credit goes to its highest, best uses. Allowing the market to properly use and allocate credit is ultimately the only way to grow out of our malaise. The Fed’s insistence on masking the economic reality with falsely priced credit means this recovery will go on waiting for its Godot.

For Information Only

This publication is for general information purposes only. Past performance is no guarantee of future results. While the information and statistical data contained herein are based on sources believed to be reliable, we do not represent that it is accurate and should not be relied on as such or be the basis for an investment decision.

Subject to Change

Any opinions expressed are current only as of the time made and are subject to change without notice. TCW assumes no duty to update any such statements. The views expressed herein are solely those of the author and do not represent the views of TCW as a firm or of any other portfolio manager or employee of TCW. Any holdings of a particular company or security discussed herein are under periodic review by the author and are subject to change at any time, without notice. In addition, TCW manages a number of separate strategies and portfolio managers in those strategies may have differing views or analysis with respect to a particular company, security or the economy than the views expressed herein.

MetWest is a wholly-owned subsidiary of The TCW Group, Inc.