EASING TENSIONS BOLSTER MARKETS

An easing of geopolitical risk led to positive performance for equity markets, pushing the DJIA up 0.8% and leading to a 1.0% increase in the S&P 500.

A wide range of data in the U.S. offered positive support for the economy, despite concerns that weather-related slowness would continue to impact economic releases.

Manufacturing was an encouraging bright spot last week. The ISM Manufacturing Index rose to 53.2 in February following a sharp deceleration in January. Readings above 50 indicate expansion in the manufacturing sector. Positive momentum was apparent in new orders, which suggests that manufacturing should have some forward momentum entering the spring season.

The service sector took a divergent path in February after it was announced that the U.S. nonmanufacturing ISM Index dropped to 51.6 in the month from 54.0 the month prior. It turned out to be the weakest reading since early 2010 due to a pronounced slowdown in the employment component. Winter weather was widely attributed as the cause for the slowdown and economists took solace from the fact that new orders actually rose slightly, suggesting that the weakness would be fleeting.

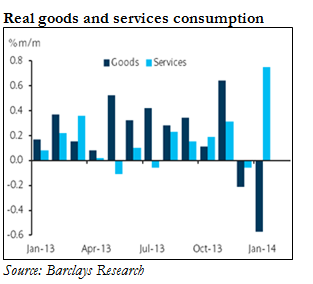

Data on consumer income and spending painted a mixed picture for January. Personal income jumped 0.3% and personal consumption rose 0.4%. Spending data was less robust than first glance, with the goods component falling 0.6% and services increasing 0.9%. The strong rise in service spending was largely a result of a 1.6% jump in health care spending, which was directly correlated to recent signups for the Affordable Care Act.

Markets closed out the week with the closely watched nonfarm payrolls report on Friday. Despite the weather-related crutch that many economists are citing, job growth proved stronger than expected in February. A total of 175,000 jobs were added to the economy, with the private sector contributing 162,000 jobs and government employees regaining 13,000 positions.

Weather did have at least a marginal impact on labor markets in February with average weekly hours moving lower by 0.1 to 34.2 in the month. Counteracting that mild disappointment was a 0.4% bump in average hourly earnings for the private sector.

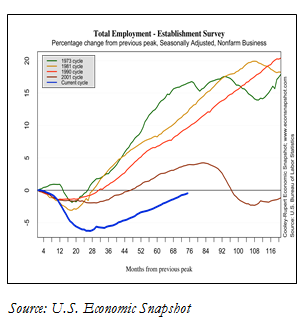

As an interesting aside, payroll employment is gradually nearing its January 2008 peak of 138.365 million jobs. In the latest month, there were 137.699 million people employed. Calculated Risk Blog estimates that a new employment peak will be established by June 2014.

TECH BUBBLE 2.0?

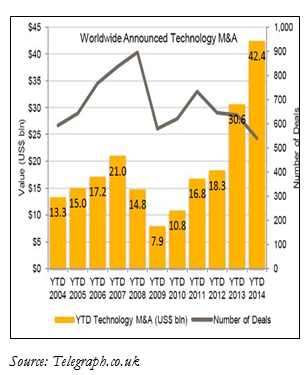

The $19 billion acquisition of WhatsApp by Facebook in late February put an exclamation point on several high profile takeovers in the technology space in recent months. Sizeable deals such as Google’s $3 billion acquisition of Nest and Facebook’s $3 billion offer for SnapChat have fueled the idea that an indiscriminate buying spree in the technology space a la 1999 could set up financial markets for another valuation bubble.

As noted by UK-newspaper Telegraph, Facebook’s WhatsApp acquisition was the fourth largest technology acquisition in history. Furthermore, the $42.4bn in technology M&A through the first six weeks of the year is the highest transaction dollar amount observed worldwide in 14 years.

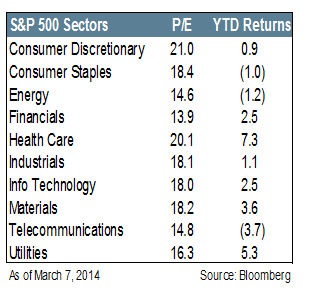

Despite the concerns, a first glance at the technology sector performance in 2014 shows the component index up just 2.5% through last Friday – slightly ahead of the headline S&P 500, but tied for fourth among the major GICS sectors. Nor do valuations look relatively expensive, with the S&P 500 technology sector trading at an 18.0x P/E multiple – squarely in the middle of the sector pack.

What an analysis of the S&P 500 masks, however, is the clear bifurcation between old and new technology in the US equity market. A more holistic look at the Russell 3000 index – which includes large, mid, and small cap securities – reveals a clear division between the largest, bellwether names in technology (think the Cisco’s and Intel’s of the world) and newer up-and-coming companies.

The nine members of the Russell 3000 technology index that are larger than $100 billion in market cap posted an average return of 3.7% through last Friday. After excluding Facebook, however – the relative newcomer to the space – the average of that group falls to just 0.6%. Furthermore, the median price-to-earnings multiple for that group is just 13.3x. At more than 56% of the index, these eight bellwether names tend to skew the headline level statistics.

A look at the bottom 400 or so companies in the sector tells a different story. The average return of that group is 6.6% thus far in 2014, while the median P/E multiple stands at 34.0x times. While one could attribute this discrepancy to a small cap effect, recent trends bear out the thesis that smaller cap names have been bid up in the technology sector. Since late 2011/early 2012, when both the bellwether tech names and the rest of the Russell 3000 technology index traded below 20x earnings, there has been a clear divergence in valuations: mega caps trended down below 15x, while the median multiple of non-mega cap names more than doubled.

The strong outperformance of many securities in 2013 lacking on fundamentals was well documented, as many of the most highly shorted companies rallied sharply. This was a headwind for many hedge funds last year and has contributed to lighter short books generally in 2014. However, as investors become more discriminate with regards to stock selection, a normalization effect could impact many of these securities.

Thus, the implication for investors is to invest wisely within the technology space in 2014. In a world where ETF usage is increasingly common, market participants may want to be more selective in a space that has clearly become bifurcated. Indeed, many of the “old” tech bellwethers have found their way into value investors’ portfolios – a once unthinkable development. While the word “bubble” probably does not apply to today’s technology market yet, greater discretion certainly does.

THE WEEK AHEAD

Economic releases will quiet down this week, but central bank meetings will pick up the slack.

Releases that bear monitoring in the U.S. include February retail sales, the producer price index, and consumer sentiment.

On the central banking side, meetings to watch are those in Japan, New Zealand, Korea, Thailand, Peru, Chile, and Russia.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value