Assessing the Impact of Financing Currency on Gold Price Performance

In our weekly commentary we follow up our discussion from last week with a brief overview of the impact on performance of diversifying the financing currencies used to make gold purchases. We also compare “Gold/Basket” performance versus gold financed with a number of different, single currencies. For the purposes of this analysis we define the Gold Basket as a gold financed with an equally weighted basket of four currencies, the dollar, euro, yen and pound; the portfolio is also assumed to be rebalanced weekly.

By way of recap in our last discussion paper we highlighted the benefits for the medium to long-term gold investor to increase the number of financing currencies used for gold purchases. When an investor buys gold they are explicitly expressing a currency view (usually that they are bearish on the dollar versus gold) and to the extent they do not have a strong directional view on the currency it might make sense for them to seek ways to reduce concentrated currency risk and gain “purer” exposure to gold. By increasing the number of financing currencies used to make gold purchases, the change in the gold price becomes a function of factors that drive the relative value of each of these currencies as well as factors that impact the relative value of gold. And to the extent that these various risk factors impact the currencies in different ways (i.e. they are not perfectly correlated), the combination of the four currencies achieves a diversification benefit that dampens down the impact of any individual financing currency on the overall gold price.

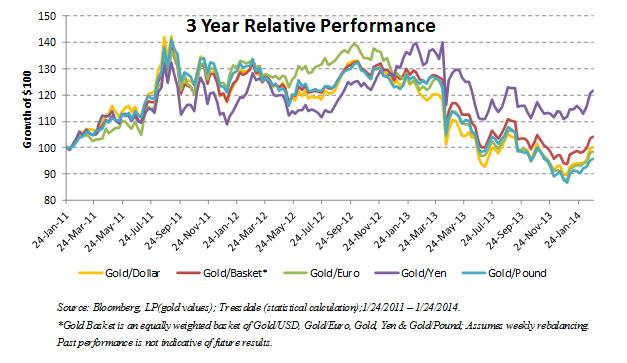

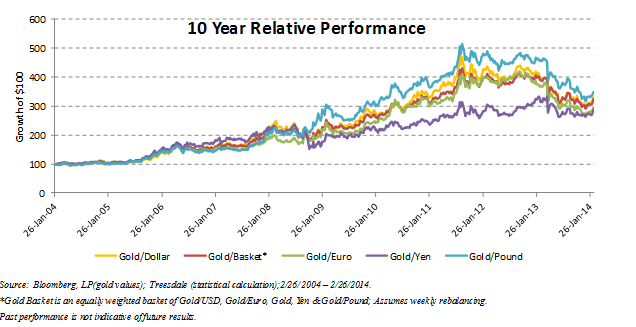

Using a ten year look-back period we compare the price of gold in dollar terms versus the price of gold in euro, yen, pounds as well as a basket of the four currencies. We also provide some summary statistics in the table below.

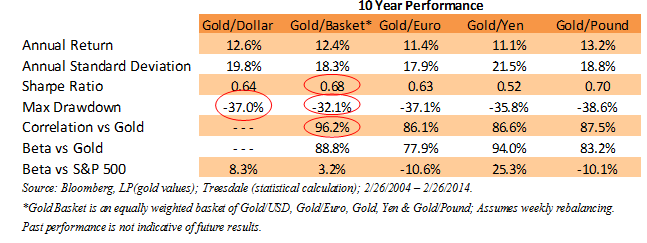

Comparing Gold/Dollar and Gold/Basket the benefits of diversification are immediately clear with the basket strategy showing lower standard deviation as well as a significantly lower drawdown. On a performance basis the two strategies put in similar returns with the Gold/Basket underperforming Gold/Dollar but with its lower standard deviation it has a marginally higher Sharpe ratio over the observation period. The peak-to- trough drawdown for Gold/USD during was -37% from September 2011 to June 2013 during which the market experienced a broad period of dollar strength and hence gold weakness. The improved drawdown for the Gold/Basket strategy can be attributed primarily to its diversification away from the dollar as the sole financing currency towards a basket of four currencies. Some other relevant observations from the 10 Year summary statistics table are the 96.2% correlation of the Gold/Dollar returns to the Gold/Basket returns showing that while the basket benefited from the diversification benefit of multiple financing currencies its return profile was still highly correlated to gold market risk factors. Secondly the magnitude and direction of the betas relative to the S&P 500 Index were similar and indicated that both had low correlation to the market portfolio. And finally the performance of the Gold/Basket as shown by the 10 year graph always sits somewhere between the best performer (Gold/Pound) and the worst performer (Gold/Yen). This should be unsurprising given that the performance of the Gold/basket, by definition, is an average of its components but this again highlights the diversification impact of using two or more financing currencies.

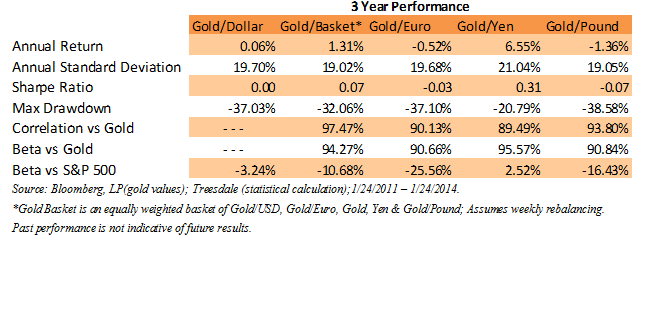

Finally we drill down to the most recent three year period during which there was a substantial fall in the price of gold versus the dollar. The maximum drawdown for Gold/Dollar was 37% driven by the strength in the dollar over the period. This is also reflected in the Gold/Euro price which experienced a similar drawdown. The best performer over this period was Gold/Yen which managed a positive return of 6.55% per annum in contrast to the 0% return of Gold/Dollar. This was of course driven by the significant (>27%) fall in the value of the yen versus the dollar which offset the gold price weakness. This serves to highlight the concentrated nature of the currency exposure that an investor is exposed to when they purchase gold using a single financing currency. And while this may be entirely consistent with the investor’s investment objectives it is important always that they understand that they are explicitly expressing a strong directional view on the financing currency – in this case the view that they expect the yen to weaken both versus gold and the dollar. In contrast the Gold/Basket returned 1.3% but with 10% lower standard deviation and also with a 97% correlation versus Gold/Dollar.