Retirement sounds pretty sweet, doesn't it? Exotic holidays. Finally writing that novel. Never having to rely on an alarm clock to wake up early. Being your own boss. Retirement goals are as varied as people themselves.

So, when can I retire?

You can retire when you have sufficient income and capital available without working to cover expenses. Your retirement income comes from investments and other assets, your retirement accounts, maybe a pension, and Social Security. Your expenses in retirement may be lower or higher, depending on your goals. Start with an estimate of your life expectancy, which varies with age, sex, health, heritage, and other factors. In general, at age 65 you can expect another 20 years to live, with a one in 10 chance of living 30 more years.

Unfortunately, the Employee Benefit Research Institute projects that as of year-end 2013, 43% of early boomers — those retiring now — will not have enough money to cover their basic expenses.¹ Your IRAs, 401(k)s, pensions, and Social Security stand a good chance of not being sufficient to cover long-term risks such as fluctuating markets, inflation, and health care.

The average monthly Social Security benefit is about $1,230 per month.² Plus, if the system doesn't change by 2033, that benefit could be reduced.³ Without significant retirement savings outside of Social Security, you might have to settle for a hammock in the backyard. Social Security will not be nearly enough to fund a junket to Italy or other retirement goals. Nor was it ever intended to be.

Can I count on Social Security?

Maybe not. It is, after all, a government income redistribution program and therefore subject to political forces. Started in 1935 to administer worker retirement benefits, the Social Security Administration also provides survivors and disability benefit programs. Social Security is both a "safety net" for the disadvantaged and a supplement for the middle class, rather than a complete benefits system. Because politicians constantly seek votes, Social Security has made unfunded promises regarding future payouts. It relies mostly on income transfer taxes on employed persons rather than accumulated assets. With the leading edge of the baby-boom generation already dropping from the labor force into retirement, the number of employed persons (the true "asset" behind Social Security) is steadily declining relative to those receiving benefits (the "liability"). And sadly, you may pay Social Security taxes for years but receive nothing in Social Security retirement benefits, as happens should you die early or otherwise be ineligible.

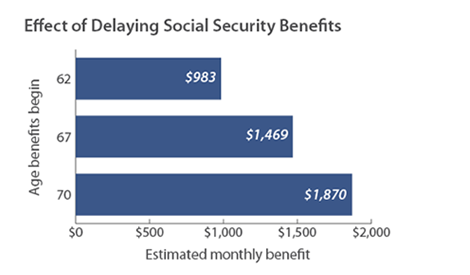

Source: Social Security Administration website "Quick Calcuator." Calculations assume earnings at national average wage of $44,321 annually with no increases over time and a date of birth of June 15, 1960.

The full-benefit Social Security retirement age is now 70

Your monthly Social Security retirement benefit is based on your age when you start taking it and your history of tax payments. For each year you delay taking Social Security after age 62 until you reach age 70, your basic benefit increases by 8%. Thus the maximum-benefit retirement age is now 70. Retire before age 70, and you will never receive your maximum monthly retirement benefit. This is because of the dual forces of the early eligibility age enacted in the 1950s and the Delayed Retirement Credit dreamed up in the 1970s. The first idea was to accommodate those in the labor force who could not work until 65 (for example, hard laborers), and the second was to prolong the system's solvency by reducing the benefit: those who take retirement early permanently receive a lower monthly benefit, and those who wait get more but for fewer years. Note there is no value in not claiming your full retirement benefit upon your 70th birthday.

Changing demographics

When Social Security was first enacted in 1935, Congress set the retirement age (the age at which you can receive benefits) at 65.4 At that time, life expectancy for men was 62, and for women it was 66.5 From those figures, it's clear that Congress intended Social Security "Old-Age Benefits" to be a safety net for those who outlived their ability to work or outlived their savings, or both, and not as a sole source of retirement income. It stands to reason they didn't expect people to retire from the workforce at all. The Social Security system unintentionally incentivized retirement at age 65, regardless of ability to work, and conditioned generations of Americans to expect their golden years would resemble an extended vacation.

In the years following, our society underwent profound changes. Transformative advances in health care, food supply and safety, transportation safety, and worker safety (among many other changes) have contributed to an increase in life expectancy. Now men can anticipate living to age 76, and women to age 81.6

Yet, the Social Security retirement age has not kept pace – plus, nine out of 10 people age 65 and older receive Social Security benefits.7

The Social Security tax rate is now 12.4%.8 For employees, the payment of this tax is split with employers. For the average worker earning $44,322 annually, that's $229 monthly out of pocket, with employers paying another $229 per worker. With the average payout around $1,230, it takes roughly 2.7 workers (and employers) paying into the system for every one retiree collecting a benefit. But by 2033, there will only be 2.1 workers for each beneficiary.4

The fact that people live longer and tap their Social Security benefits longer has compounded the difficulty in funding those benefits. Indeed, many of us question whether Social Security will even exist when we retire. These lurid prognostications have some basis in fact. Social Security Trustees anticipate that by 2033 tax revenues will only be sufficient to cover three-quarters of "scheduled benefits." They reason that this deficit will be caused by the twin actions of the "large baby-boom generation entering retirement and lower-birth-rate generations entering employment."3 With fewer workers generating tax revenue for the Social Security program, and more people to pay (and pay longer), this "entitlement" cannot continue unchanged.

Raise the retirement age

There are a number of things that could be done to improve the situation, but all have politcal difficulties:

- Raise the tax rate. This immediately reduces your take-home pay and increases your ire with Congress. When Social Security was first devised in 1935, the employment tax rate was 2% (split between workers and employers), only the first $3,000 of income was subject to tax, and the maximum collected per worker was $60 annually. Now, the federal employment tax rate is 15.3% (including the 2.9% Medicare tax and 12.4% for Social Security taxes), the first $117,000 of income is subject to tax, and the maximum collected per worker is 242 times larger at $14,508. Raising the tax rate is an unlikely political move, especially considering the 2011–2012 vote-buying 2% tax rate cut for economic stimulus. It's worth noting that higher-paid workers are already subject to employment tax increases in the form of continuing automatic increases to the base income subject to tax.

- Decrease benefits. This is a non-starter. Nobody wants "raging grannies" demonstrating in the streets of America.

- "Soak the rich." As mentioned earlier, Social Security is partly an income redistribution program with benefits not directly tied to the taxes you pay. For example, a worker taxed on $276,000 of income over the 20 years from 1998 to 2017 will receive a monthly benefit of $824 starting in 2018, according to the SSA's website. Another worker, taxed on double the income, $553,000 over the same 20 years, gets a monthly benefit of $1,118. So, paying 100% more in tax provides only 36% more in benefits. Such unfair treatment only incentivizes some richer folks to seek compensation in ways not subject to employment taxes.

- Increase income tax collected on Social Security benefits. This is another way to soak the rich. However, there is not much more to squeeze here, because already up to 85% of your Social Security benefits may be considered taxable income if your "combined" income is above $32,000 ($44,000 if married — a major tax penalty on marriage). In 2012, Social Security beneficiaries paid $45.9 billion in taxes on their benefits. This is double taxation, as Social Security taxes paid by employees are not deductible for income tax purposes. Many states further tax Social Security retirement income.

- Implement means testing. Reducing retirement benefits, possibly to zero, based upon your prior year's tax return would be easy to implement. It would starkly clarify the change from a social insurance program to a welfare program. It would penalize thrift and work in retirement.

- Find new ways to tax retirement plans. New limits on large balances in retirement accounts, such as IRAs and 401(k)s, are proposed. Outright confiscation of retirement accounts, as has happened in countries like Argentina, is unlikely.

- Encourage Inflation. If prices rise, money is worth less — the amount of goods and services you can buy with the same number of dollars is reduced. While inflation is bad for consumers (and savers), it allows governments to meet promises, such as underfunded Social Security benefits, with dollars that don't have much value. Consider that gasoline, for example, has increased 10 times in price, from $0.36 per gallon to $3.60 per gallon, over the last 40 years.9

- Privatize Social Security. The idea of privatizing Social Security, in whole or part, was championed during the last decade. Since private accounts restrict the income transfer foundation of Social Security, this is highly unlikely.

- Our view: Raise the retirement age. Raising the minimum number of years, now just 10, to qualify for retirement benefits will also help.

Although raising the retirement age might not be a popular choice, it makes the most sense because of the strains put on the system by Americans' increasing longevity and the accompanying demographic shifts. Other heavily indebted countries, such as Greece, Italy, France, and the United Kingdom are raising their retirement ages.

A 2012 study by the SSA's Office of Retirement and Disability suggested that raising the age at which workers are eligible for benefits would improve system solvency by the necessary amounts.10 This study focused on the effects of raising the "early eligibility age" and further raising the "full retirement age" over time, which in our view must be done.

Retirement is your responsibility

Barring revolution in America, Social Security is going to continue paying benefits. Today, $14,760 a year is only enough to cover 70% of average basic living expenses. In further defiance of economic reality, benefits are set to increase over time, although political partisans don't agree on the indexing method. Regardless, the country has built up a huge debt, in part because of generational wealth transfer programs such as Social Security, increasing the likelihood of future inflation. Living standards for many Americans have declined for some years — a trend expected to continue — for retirees and workers alike.

In recognition that Social Security isn't sufficient to fund your retirement, the current administration has decreed a new retirement savings program, the myRA. Employers will be encouraged to deduct a further amount from your paycheck each month, and send it to the government's "G Fund" program. We think no-load mutual funds with low-investment-minimum retirement accounts are better choices.

Regardless of when you retire or start receiving Social Security benefits, there are things you can do now to lessen your dependence on a system that's essentially insolvent: Save. Invest. Start early. Take advantage of retirement savings plans like 401(k)s, IRAs, and their permutations. Max out your contributions, if you can. For the least pain, add your next pay raise to your retirement plan each month, rather than increase your spending. Avoid and pay off debt. These are good ways to increase your chances for a comfortable retirement and maybe even afford that big trip.

Footnotes

¹ VanDerhei, Jack, Ph.D. "What Causes EBRI Retirement Readiness Ratings to Vary: Results from the 2014 Retirement Security Projection Model." Employee Benefit Research Institute Brief, Issue No. 396, February 2014. Published online at ebri.org. The Employee Benefit Research Institute is a private, nonpartisan, nonprofit research institute based in Washington DC, that focuses on health, savings, retirement, and economic security issues.

² US Social Security Administration, "Retirement Planner: Full Retirement Age" (http://www.socialsecurity.gov/retire2/retirechart.htm)

³ Social Security and Medicare Boards of Trustees, "A Summary of the 2013 Annual Reports" (http://www.ssa.gov/oact/trsum/)

4 Social Security Act of 1935 (http://www.ssa.gov/history/35actinx.html)

5 US Department of Health and Human Services, Centers for Disease Control and Prevention, National Center for Health Statistics, "US Decennial Life Tables for 1989-91" (http://www.cdc.gov/nchs/products/life_tables.htm)

6 US Department of Health and Human Services, Centers for Disease Control and Prevention, National Center for Health Statistics, "Health, United States, 2012" (http://www.cdc.gov/nchs/hus.htm)

7 Social Security Administration, "Social Security Basic Facts", July 26, 2013. (http://www.ssa.gov/pressoffice/basicfact.htm)

8 US Social Security Administration, FAQ. (https://faq.ssa.gov/link/portal/34011/34019/Article/2076/Will-I-pay-160-higher-Social-Security-tax-rates-160-if-160-I-am-self-employed-than-if-I-work-for-someone-else)

9 US Department of Energy, Vehicle Technologies Office, Fact #741: August 20, 2012, Historical Gasoline Prices, 1929-2011. (https://www1.eere.energy.gov/vehiclesandfuels/facts/2012_fotw741.html)

10 Olsen, Anya. Social Security Administration, Office of Retirement and Disability. "Mind the Gap: The Distributional Effects of Raising the Early Eligibility Age and Full Retirement Age" Social Security Bulletin, Vol. 72. No. 4, 2012. (http://www.ssa.gov/policy/docs/ssb/v72n4/v72n4p37.html)

Copyright 2014 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 8 · No. 3

Important Disclaimers and Disclosures

This report is intended only for the information of the reader and is not to be used for or considered as an offer or the solicitation of an offer to sell or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries or affiliates ("Saturna"). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any other service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied, or distributed to any other party without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks, and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable, and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will change over time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials, including any containing materially different information, are brought to the attention of any recipient of this report.

Under no circumstances shall Saturna, its employees, or any affiliate be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to making any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal, or accounting advice. Investors should consult their own tax, legal, and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of US federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing, or recommending to another party any transaction or matter discussed herein.

The Dow Jones Industrial Average is a price-weighted index of 30 of the largest, most widely held US stocks. The S&P 500 is an index comprised of 500 widely held common stocks considered to be representative of the US stock market in general. The Russell 1000 Growth index is a widely recognized index of large-cap growth stocks. The Russell 2000 Index is comprised of US small cap stocks and measures the performance of the 2,000 smallest US companies in the Russell 3000 Index. The NASDAQ Composite index measures the performance of more than 5,000 US and non-US companies traded "over the counter" through the National Association of Securities Dealers Automated Quotation system. The MSCI EAFE Index, produced by Morgan Stanley Capital International, measures the equity market performance of developed markets in Europe, Australasia, and the Far East. The MSCI Emerging Markets Index, produced by Morgan Stanley Capital International, measures equity market performance in over 20 emerging market countries. Barclay's Capital US Aggregate Bond Index measures the performance of the US bond market. All indices shown are widely recognized unmanaged indices of common stock prices that reflect no deductions for fees, expenses, or taxes. Investors cannot invest directly in the indices.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price for, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuations that may have a positive or negative effect on the price or income of such securities or financial instruments. Investors in securities such as American Depositary Receipts — the values of which are influenced by currency volatility — effectively assume this risk.

Please consider an investment's objectives, risks, charges, and expenses carefully before investing. To obtain this and other important information about the Amana, Sextant and Idaho funds in a current prospectus or summary prospectus, please visit or call toll free 1-800/SATURNA. Please read the prospectus or summary prospectus carefully before investing.

The Amana, Sextant and Idaho Tax-Exempt Funds are distributed by Saturna Brokerage Services, member FINRA /SIPC. Saturna Brokerage Services is a wholly-owned subsidiary of Saturna Capital Corporation, adviser to the Amana, Sextant and Idaho Tax-Exempt Funds.