Currency Markets Heat Back Up, and Will Likely Remain that Way

MACRO CONCERNS CAUSE FLIGHT TO SAFETY

Equity markets retrenched last week following two straight weeks of gains, pulling the Dow Jones Industrial Average back into negative territory for the year. The S&P 500 remains slightly positive year-to-date through last Friday. Last week the two indices returned losses of 2.3% and 1.9%, respectively.

Geopolitical issues in Ukraine stoked a bout of risk aversion, heading into a weekend vote by Crimea on secession from the country. Russia’s attempts to annex the Ukrainian region are furthering tensions between Russia and the West, with US officials going as far as to declare the actions “illegal.” The yield on the 10-year Treasury fell nearly 20 bps last week during this flight to safety.

Adding to concerns was weaker than expected data in China. Industrial production rose 8.6% year-over-year in the first two months of 2014, down from 9.7% in December and the slowest start to a year since 2009. Retail sales, meanwhile, grew 11.8% in January/February, nearly two full points below expectations with broad-based declines observed. According to Bloomberg News, that was the slowest pace since 2004. The data reinforces concerns about growth levels in the world’s second largest country.

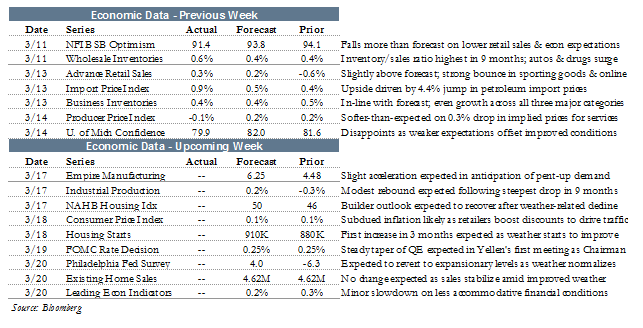

In the US, there were a few notable economic reports for investors to digest; as has become standard fare for economic data as of late, the results were decidedly “mixed.”

The biggest report of the week, retail sales, edged out consensus slightly with a 0.3% month-over-month gain in February. However, any optimism over this uptick was undercut by a negative revision to January’s initial 0.4% contraction; the revised figure revealed a 0.6% decline in the month.

February’s retail sales number showed general gains across the underlying components. The core measure, which strips out more volatile automobile and gasoline sales, also rose 0.3%, suggesting no undue influence from those factors.

The National Federation of Independent Businesses (NFIB) released their monthly small business optimism survey on Tuesday. February’s figure was a disappointment, as nine of the 10 components were flat or negative. The index fell 2.7 points to 91.4, the lowest reading since March of last year. NFIB Chief Economist Bill Dunkelberg noted that readings of this level are “historically associated with recession and periods of sub-par growth.”

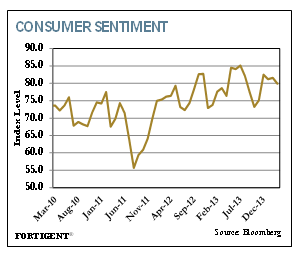

The other major indicator of the week was consumer sentiment’s mid-month update. In a validation of the consumer confidence report two weeks ago, the headline reading for consumer sentiment weakened while underlying data appeared more positive. In both reports, consumers’ assessment of current conditions actually improved, while future outlooks dimmed. Many analysts put more weight on the current assessment components of these reports, making Friday’s sentiment report slightly more encouraging.

CURRENCY MARKETS HEAT BACK UP, AND WILL LIKELY REMAIN THAT WAY

Long dormant after the financial crisis, foreign exchange markets are beginning to heat up, offering ample trading opportunity for asset managers. The U.S. dollar was widely viewed as being the best long trading opportunity for 2014, but so far, that has not played out, with activity in the Euro, Chinese Yuan, and other currencies impeding dollar strength.

Of most surprise has been the strength of the Euro relative to the U.S. Dollar. From a policy perspective, it was assumed that continued monetary easing in Europe would weaken the Euro, while a wind down of programs such as the taper in the U.S. would lead to dollar strength.

Source: Federal Reserve Bank of St. Louis

In reality, the Euro has moved consistently higher this year, recently breaching the $1.39 mark. Recent strength in the Euro is being attributed to “inaction” on the part of Mario Draghi and his European Central Bank (ECB) counterparts, but risks of a stronger Euro may require intervention on the part of the ECB.

Recent inflation trends across the Eurozone suggest a markedly weaker price path. Year-over-year through January, prices in Europe are up 0.7%, but the path has clearly been lower since 2011. With the Euro moving higher against many of its trading partners, European exports become less competitive and place additional pressure on the Eurozone from a pricing standpoint. Mr. Draghi may have no choice but to intervene, or risk tempting a painful deflationary downdraft.

Source: Haver Analytics

Some are now arguing that the Euro will strengthen no matter what, as there are indications China is actively diversifying its currency reserves away from the dollar and towards partners such as Europe. At the end of 2013, China held roughly $3.8 trillion in currency reserves, and the announcement that Chinese officials intended to liberalize the trading band of the U.S. Dollar relative to the Chinese Yuan suggests that changes are happening. If China is behind the latest Euro strength, it may be difficult for anyone to combat further Euro strength.

But, as the Euro strengthens and China struggles to revamp its monetary policy, there are other clear developments working towards a stronger U.S. Dollar. In particular, our neighbors to the north are dealing with a weakening commodity market, softening labor markets, and a housing market that is rolling over.

Source: Federal Reserve Bank of St. Louis

Entering the year, the common mantra was that 2014 was the year for dollar bullishness. That may still play out as the Fed accelerates the taper and begins the process of discussing interest rate hikes. For the moment, though, the Euro appears to have the force of the Chinese behind it, which should prompt further support for that currency. Other currencies are offering trading opportunities, such as those seen in Canada, and the environment for currency trading is expected to remain robust.

THE WEEK AHEAD

Economic news picks up sharply this week, highlighted by the FOMC’s first meeting under new Chair Janet Yellen on Tuesday and Wednesday.

Major economic data is also due including industrial production, housing starts, consumer inflation, and existing home sales. Important regional manufacturing reports from the New York and Philadelphia Federal Reserve Banks should also provide further insight into the US manufacturing picture two weeks before the ISM manufacturing index is released.

With Crimea overwhelmingly voting to secede from Ukraine and Russia promising to expedite its annexation of the region, geopolitical tempers could flare this week.

Other global central bank meetings take place this week in Turkey, Switzerland, Colombia, and Mexico. Minutes are also due from the Bank of England’s most recent policy meeting.

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value