There seems to be little debate on the potential impact of current and future consumer spending on economic growth. Our constructive outlook on the consumer supports our general economic optimism. What we believe is less well noted, however, is the prospective influence of higher levels of corporate expenditures, particularly capital expenditures (capex) in new equipment, facilities, and technology.

After several years of recovery, what could be driving this change now?

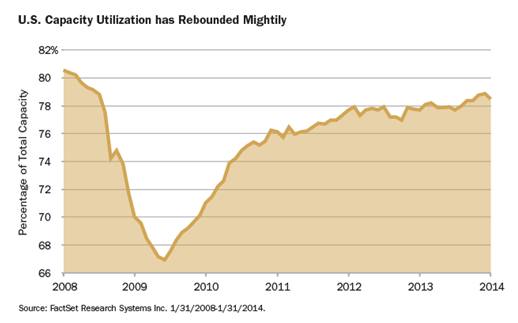

Reason #1: Businesses Will Need Additional Capacity

The financial crisis had a devastating impact on the levels of capacity utilization in the U.S. As the economy fell into a steep recession and demand for goods dropped sharply, corporate plants, facilities, and equipment operated well below their typical levels.

Since then, as the economy has recovered so has capacity utilization, climbing back to almost pre-crash levels. At this point, companies that want to continue on a path of growth will need to make additional capital investment so they can crank up production to meet the potential consumer demand.

Reason #2: It’s Overdue

Just as capacity utilization dropped during the financial crisis, so did Private Domestic Investment—a figure that, when described as a percentage of Gross Domestic Product (GDP), serves as a measure of corporate capital spending. What’s interesting about this data though, is that while it shows a meaningful rebound over the past few years, it remains nowhere near its pre-crisis level, and even falls well short of its historical average.

On its face this chart suggests the economy can readily absorb greater levels of corporate invest ment. We believe it also shows that higher levels of capex may be a necessary ingredient for GDP growth to accelerate.

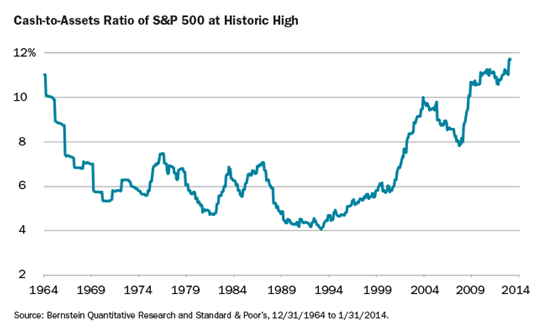

Reason #3: The Money is There

Motivated largely by the sense of caution that has followed the financial crisis, U.S. companies have accumulated hefty stockpiles of cash on their balance sheets. This is the product not just of the relatively modest corporate capital spending depicted in the preceding graph, but also of the improving earnings that have accompanied the economic recovery.

Given the severity of the past decade’s downturn—and perhaps more important, the extreme credit crunch that followed—it’s not entirely surprising that companies have sought to keep a little powder dry, and to build up some cash.

As the graph below shows, the ratio of cash to other assets is at a nearly 50-year high. (The graph excludes Financials stocks, whose distinctive capital structures can tend to skew the results.)

Simply put, many companies that need to make long-overdue capital investment also have the financial wherewithal to do so. In addition to cash on hand, cleaner balance sheets make it easier to obtain credit on attractive terms. In either case, the end result is that companies needn’t worry too much about finding the resources to fund a new, much-postponed round of capital expenditures.

Reason #4: Companies Say They’ll Spend

With companies, as with people, sometimes the best way to determine what they are likely to do is to listen to what they say. And right now, according to data compiled by the Kansas City Federal Reserve Bank, corporations are saying that they intend to significantly increase capital spending.

Historically, such data has proven to be more than talk. As this graph indicates, there has been a high level of correlation between these reported intentions and subsequent spending. So we consider this to be an important leading indicator, and one that we find especially compelling in light of the other data supporting higher capex levels going forward.

What Kinds of Companies can Benefit?

Just as with consumer spending, the impact of higher levels of corporate capital investment in buildings, machinery, and technology can permeate virtually every sector of the market.

One of the areas we believe stands to benefit is Engineering and Construction. These companies are engaged in building new facilities to serve a variety of industries, including power generation, petroleum refining, civil infrastructure, and chemical processing. All of these areas could face rising demand from an uptick in corporate expenditures. Transportation is another industry group poised to benefit, particularly stocks tied to the railroads and truckers needed to move equipment and materials to their destinations. From the Financials sector, Commercial Banks could also see an improvement in their business, as highly creditworthy companies seek loans to finance their new investment in plants and facilities.

Whatever the industry involved, we believe a disciplined, fundamental stock-selection process will be essential to identifying stocks that are not only in businesses that may benefit from this broad trend, but also have the financial soundness, reasonable valuations, and catalysts for recognition that can ultimately drive their stock prices higher.

How We’ll Monitor This Developing Trend

Even though we see many signs pointing toward an upturn in capex spending, our decades of experience investing in equities have taught us that nothing is a given. So we’ll be closely tracking additional leading indicators, including the CEO Confidence and Small Business Optimism indexes. These measures help us to see how corporate decision-makers are interpreting economic data.

As contrarian investors, we also believe in considering alternative viewpoints. Thus we’ll be mindful of turns in these and other important economic data that could point to an interruption in GDP growth. Given how long capex spending has been postponed, however, we believe that even a moderate level of economic expansion could be sufficient to support such spending for the foreseeable future.

Disclosure:

Past performance does not guarantee future results.

The statements and opinions expressed in this article are those of the author. Any discussion of investments and investment strategies represents the portfolio managers’ views when presented, and are subject to change without notice.

Economic predictions are based on estimates and are subject to change.

Data Sourced from FactSet: Copyright 2014 FactSet Research Systems Inc., FactSet Fundamentals. All rights reserved.

Gross Domestic Product (GDP)is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis.Kansas City Fed’s Manufacturing Surveyprovides information on current manufacturing activity in the Tenth Federal Reserve District. The survey monitors manufacturing plants selected according to geographic distribution, industry mix and size. Survey results reveal changes in several indicators of manufacturing activity, including production and shipments, and identify changes in prices of raw materials and finished products.Private Domestic Investmentmeasures the spending of private businesses, not for profit organizations, and households on fixed assets in the U.S. economy.US Capacity Utilization is calculated for the manufacturing, mining, and electric and gas utilities industries. For a given industry, the utilization rate is equal to an output index divided by a capacity index. Output is measured by seasonally adjusted indexes of industrial production. The capacity indexes attempt to capture the concept of sustainable practical capacity, which is defined as the greatest level of output that a plant can maintain within the framework of a realistic work schedule, taking account of normal downtime, and assuming sufficient availability of inputs to operate the machinery and equipment in place.S&P 500 Indexis an index of 500 U.S. stocks chosen for market size, liquidity and industry group representation and is a widely used U.S. equity benchmark. All indices are unmanaged. It is not possible to invest directly in an index.

2014144

© 2014 Heartland Advisors