Global investors have been experiencing an ongoing drag on returns to the extent they have had exposure to Emerging Market (EM) equities. It is difficult to abandon the asset class given historical performance, relative economic growth, current valuation discounts, and portfolio management tenets regarding diversification. But the fact that the U.S. has been such a strong performer, along with its size and prominence in the press, creates questions about why any non-U.S. stocks should even be in the portfolio. For experienced investors, the real question centers on how to exploit the eventual recovery and what might trigger such a move. In this article, we attempt to review all of these issues in a short-hand, summary fashion.

The EM Case

- EMs are too important to ignore with 82% of the world’s population and 32% of its income;

- EMs have an abundance of natural resources;

- Emerging economies have been growing consistently faster than developed markets for a long period of time;

- The emerging consumer is becoming more important with middle class membership increasing substantially in many countries. For instance, growth in consumption is far outpacing what is being seen in the U.S.;

- Investment spending is outstripping DM and is expected to continue to expand;

- Portfolio benefits are compelling with higher long-term returns and diversification benefits.

EM Differentiation

- With the case made for EM, it then seems counterintuitive to belittle the investment management profession and call the space a contrived asset class. Yet, the differences amongst countries’ fundamentals are considerable.

- Currently, the fear of tapering and attendant rise in interest rates has created a potential scenario whereby countries with a current account deficit find it difficult to fund their shortfall. However, there are many EM countries with strong external fundamentals – current account surpluses, exceptional foreign reserve balances, etc. These countries are as cheap as those that have funding issues.

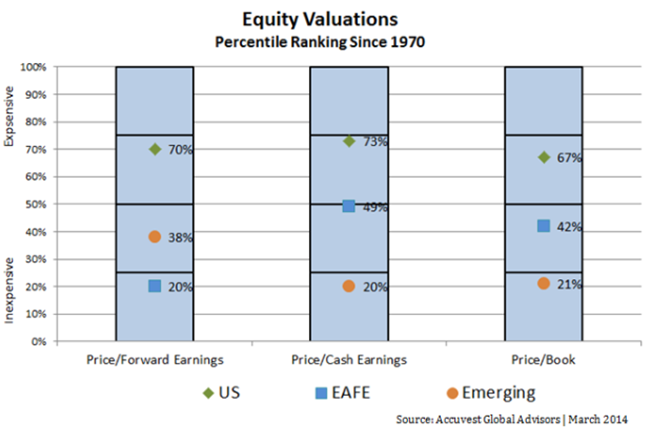

- Fundamental and risk metrics are varied amongst all countries and perhaps more so in EM. Valuations, however, are universally cheap. On average, there is a 4 point discount in P/E’s for EM vs DM. China, as an example, is trading at a 27% discount to its 10-yr average which is 90th percentile cheapness to its own history. Relative to APxJ, EM is at its 98th percentile cheapness to its 10-year history.

EM Performance Triggers and Outlooks

- Valuation is a necessary condition for EM countries to attract attention and see prices move higher. However, it is not a great timing tool.

- EM needs to see growth outlooks stabilize and the Yellen-led Fed to confirm its accommodative stance. Avoiding a currency crisis is paramount. As of now, that does not seem to be a problem.

- So, we could be very close to a rotation out of what is a relatively expensive US market into countries that have fundamental and valuation profiles that are attractive. The cycles seen historically as EM countries gain attention and assert their relative growth advantages can be strong, long-lasting and highly rewarding. In the spirit of “buy low, sell high” there is no doubt that many EM countries pass the test of being “low”. Investors need a process to select those countries and a commitment to value-based principles that will produce strong outperformance from current levels.

Disclosure: The opinions expressed in this report are those of the author. The materials and commentary are strictly informational and should be used for research use only. This bulletin is not intended to provide investing or other advice or guidance with respect to the matters addressed in the bulletin. All relevant facts, including individual circumstances, need to be considered by the reader to arrive at investment conclusions that comply with matters addressed in this report. Charts and information used in this report are sourced from Accuvest Global Advisors (AGA). Past performance is not indicative of future results. Remember that investing involves risks, as the value of your investment will fluctuate over time and you may gain or lose money. Investment risks are born solely by the investor and not by AGA.