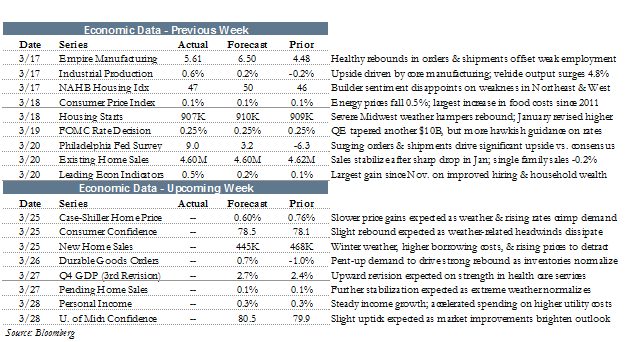

FEW SURPRISES IN ECONOMIC DATA

Equity markets continued their back and forth affair, bouncing back last week despite a sharp sell-off in the wake of Wednesday’s Fed announcement. The S&P 500 and Dow Jones Industrial Average rose 1.5% and 1.4%, respectively, while the BarCap Aggregate Bond index shed 40 bps.

Aside from the first FOMC meeting under new Chair Janet Yellen, which we discuss at length later on, economic reporting last week was decidedly middle of the road. Data continues to be questionable due to the severe weather conditions experienced in the first two months of 2014.

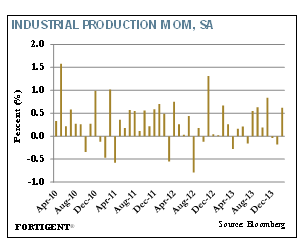

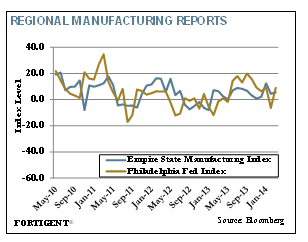

The week got off to a mixed start with better than expected industrial production (IP) results for February offset by a mildly disappointing Empire State Manufacturing Survey.

Industrial production rebounded from a 0.2% contraction in January to a 0.6% expansion in February. The manufacturing component of IP was even stronger, rising 0.8% off a deep 0.9% decline to start the year. This flip-flopped with the utilities component, which saw strong demand in January normalize the next month.

The Empire State index improved marginally, from 4.48 to 5.61; however, this figure came in below analysts’ expectations for March. Underlying components were a mixed bag, with new orders crawling out of negative territory (a positive sign for future readings) but employment conditions falling sharply.

The Empire State’s closely watched sibling report, the Philadelphia Fed Business Outlook Survey, exhibited much more robust improvement. The index jumped from a negative 6.3 reading last month to 9.0 in March, propelled by gains in new orders, unfilled orders, and shipments. This eclipsed the consensus 3.0 level, but, much like the New York report, the employment component also weakened. The picture painted by these two regional indices suggest manufacturing payrolls could be soft in the Labor Department’s upcoming jobs report.

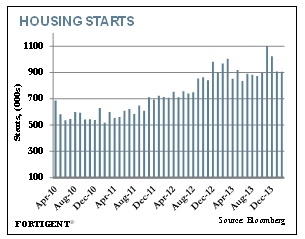

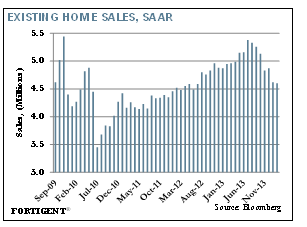

The housing market performed largely as expected, with both starts and existing home sales printing in line with expectations.

Housing starts advanced at a rate of 907,000 homes in February, a hair under consensus. Both single family and multi-family units experienced an improvement from sharp declines in January, albeit to just 0.2% and negative 1.2%, respectively. In the prior two months, largely offsetting revisions reduced December’s pace and increased January’s.

One notable standout from February’s report was a spike in housing permits of 73,000 to 1.018 million. This may suggest improvement in future housing start figures, although empirically that relationship has been mixed.

Existing home sales continued their extended slide, falling 0.4% in February to a pace of 4.6 million homes. The series has fallen six times in seven months since peaking at 5.38 million in July; as noted by research shop Econoday, the 7.1% year-over-year decline in sales is the biggest fall in almost three years. In sharp contrast to the fall in sales is a 9.1% increase in home prices, which, along with higher mortgage rates, may be factoring into the disappointing trend.

Finally, consumer inflation suggested no material deviation in trend from the past several months. Headline inflation ticked up 0.1% while year-over-year inflation remains mired just above the 1.0% level, which is about half of the Fed’s target. Core inflation remained at 0.1% over the month and 1.6% over the year.

JANET YELLEN ENTERS THE PICTURE

After bursting onto the scene earlier this year, Janet Yellen held her first official FOMC meeting last week. Rather than upset the apple cart, she held a largely status quo stance, but several comments raised more than a few questions.

At a high level, the FOMC elected to continue the path of recent precedent by electing to trim asset purchases another $10 billion and maintain the current low interest rate environment.

Yellen left her mark by indicating that the Fed will move away from using the unemployment rate as a gauge to raising interest rates, and will now instead rely on a broad range of economic indicators. In its statement, the FOMC said, “the Committee will assess progress toward its objective of maximum employment and 2 percent inflation.”

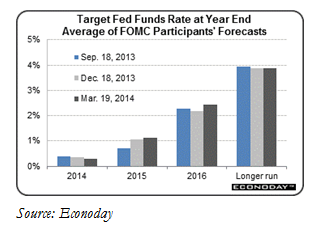

The FOMC also surprised market participants by bringing forward its expected date of higher interest rates. By the end of 2015, for example, the FOMC now expects overnight rates to stand at 1.0%, up slightly from the previous two meetings.

More specific to the issue of raising rates, during the Q&A session, Yellen indicated that the first rate hike could occur as soon as “4-6 months” after the conclusion of the taper, which caught the market very off guard. As the Q&A progressed, yields on the 10-year Treasury jumped from as low as 2.67% to nearly 2.8%, a quick acknowledgement by traders that they were not appropriately positioned for rate increases in the intermediate term.

During a period where economic data in the U.S. has slowed, in part due to recent harsh weather on the East Coast, such conviction on the timing of rate hikes was not well received.

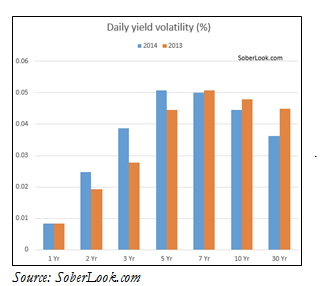

Fixed income markets will continue to grapple with the implications of Yellen’s comments, but the one thing most investors are certain of is that this year will bring higher volatility for fixed income markets. The year is off to a mostly strong start across the fixed income universe, but year-to-date volatility has been higher on the shorter end of the Treasury curve as compared to last year.

In her first official FOMC meeting, Yellen largely held the path set out by Ben Bernanke in his last few months. By all estimations, the Fed will continue to taper its asset purchases until later this year, when it will be fully out of the market. The only criticism of Yellen’s first meeting was the specific mention of rate hikes well before the market was ready. There is a possibility this will weigh on markets going forward and it could act as a countervailing force for the stability the Fed is trying to accomplish.

THE WEEK AHEAD

The first quarter nears the finish line this week with a few important indicators, including the Case-Shiller Home Price Index, new home sales, personal income & spending, and the final estimate of fourth quarter GDP. Analysts expect a mild uptick in Q4 GDP following a sharp second revision to 2.4% (from an initial 3.2% estimate).

Abroad, indicators to watch include various flash PMIs from the Eurozone and China, as well as a bevy of economic data from Japan.

Central bank policy decisions are due this week from Israel, Hungary, South Africa, Philippines, Taiwan, Norway, Czech Republic, and Romania. In a sign of the divergence occurring in emerging markets policy, Hungary is expected to cut rates by 10 bps while South Africa is forecasted to increase its repo rate by 50 bps.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value