Equity valuations, though not as drop-dead gorgeous as they once were, still look attractive enough to produce good equity gains going forward. Even so, many in the financial community hesitate, citing two interlinked objections in particular. One suggests that corporate earnings are unsustainable, that recent gains are the result of cost cutting and will eventually fail. The second reflects back on the suspect earnings and questions whether price-to-earnings (P/E)1 multiples can hold existing levels. Both objections, though understandable, miss critical considerations. To start, corporate earnings, though they have outpaced revenues growth, are not, as so many suggest, the product of unsustainable cost cutting. Rather, they are the solid, reliable result of operating leverage in American business. They have a reflection in all past recoveries and, if anything, likely will continue, at least to some degree. They certainly are not likely to fail. That fact alone makes multiples look more secure, but even more, historical relative valuations suggest that they have room to expand.

Reliable Earnings

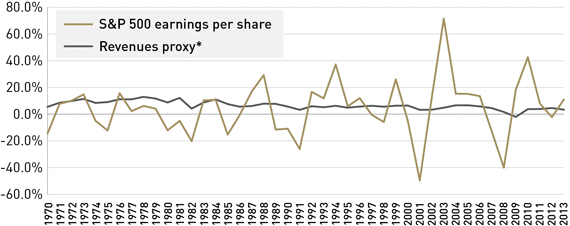

The main fear on earnings lies in how they have outpaced revenues. In 2010, for instance, the first full year of economic recovery, the earnings of companies in the S&P 500® Index2 rose 49.5%, far faster than revenues, which expanded only 6.0%. In 2011–12, the difference between earnings and revenues growth narrowed, but still, over the entire three-year stretch through 2012, the gap remained large. Earnings grew at an annual rate of about 17.0%, while revenues expanded at only a 6.3% rate. Last year, earnings outpaced revenues again, expanding about 11.0% on preliminary figures, compared to only 3.6% growth in revenues.3

It is easy to see in these differences why many have worried that earnings have a less than solid base. But the popular explanation that they result from unsustainable cost cutting misses the mark. Such differences are too vast to yield to suggestions, as some have made, that managements engineered this earnings surge by cutting out frills, such as first-class travel, or essentials, such as maintenance. Even suggestions that they have held back on bonuses cannot explain the difference. On the contrary, the huge disparity between earnings and revenues growth invites a more fundamental, durable, and reliable explanation. The answer is operating leverage.

This is fundamental, especially in the United States, where business is highly capital-intensive. Robotics, computers, systems, and other facilities allow companies to do more with fewer employees. The effort has enhanced productivity, efficiency, and profitability. At the same time, however, it has raised fixed costs, for whether times are good or bad, whether firms use the powerful equipment and systems or not, they must continue to pay, to maintain them, and to service the debt they often incurred to obtain them. When times are good and all this equipment is effectively employed, much of the revenue it generates flows to the bottom line instead of to the workers for whom it substituted. But when times are bad, firms cannot lay off the equipment, as they can workers, leaving much of the revenue shortfall to come out of the bottom line. Then in the recovery, as this equipment comes back on line, the earnings catch up. And because the revenues number is huge compared to the profits number, the percentage moves in earnings, up and down, are vast.

The pattern is evident in this cycle. In the last great recession, as revenues fell 16.5% from the September quarter of 2008 to the December quarter of 2009, the fixed costs brought most of this loss to the bottom line, creating a more extended drop in earnings that from its peak in the June quarter of 2007 to its trough in the June quarter of 2009 amounted to more than 90%. But as even the sluggish recovery that followed began to bring this equipment back on line, almost all the additional revenues flowed into earnings having the opposite, positive impact described above.

Source: FactSet.

*Uses national income and product account proxy for revenues growth.

The same pattern is evident in past cycles, as Chart 1 makes clear. In the 2001–02 recession, for instance, revenues only flattened out, but operating leverage caused a 30.8% collapse in the annual averages of earnings used here. But, then, also consistent with the pattern, earnings came back stronger in the recovery, jumping at a 17.7% annual rate from 2001 through 2006, while revenues expand only about 6.0% a year. The same picture emerges going even further back. In the 1974–75 recession, for instance, real economic activity shrank by 1.2% cumulatively, though the high inflation of the day, more than 9% at an annual rate, kept the nominal revenues figure rising. Earnings, however, fell 17.5% in 1975. And consistent with the effect of operating leverage, earnings in the recovery outstripped revenues, rising almost 19% a year for the next two years. Much was inflation, of course, which nonetheless accounted for a far greater proportion of the 11.1% revenues growth.

Attractive Multiples

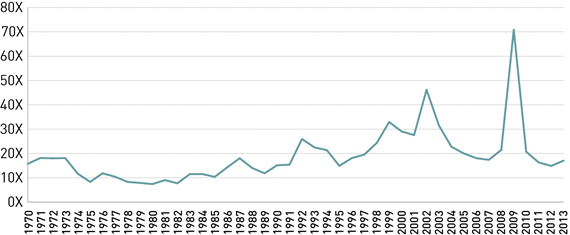

If, as should be apparent, the earnings figures are a reflection of basic business gains, then existing multiples look far more secure than some suggest. Beyond secure, several additional considerations suggest that they could easily move upward. For one, today's prices, at some 17.4 times last year's earnings, or 16.5 times consensus for this year, hover close to the long-term, 35-year average, as Chart 2 illustrates. Stocks at worse, then, can be described as fairly valued and at worst should track earnings. For another, the natural cyclical pattern of multiples, as the chart also shows, usually carry them through the long-term average as they advance from lows. On this basis, the historical pattern would suggest further multiples gains. Still more compelling, stock valuations relative to bonds and cash show ample room for a multiples advance.

Source: FactSet.

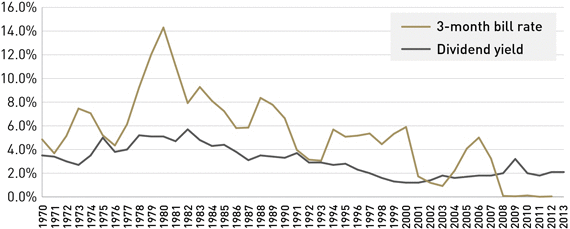

The difference relative to cash is striking. Today, the best an investor can do with cash is to get 30 basis points (bps). Against that, the stocks in the S&P 500, even after last year's impressive market gains, offer a dividend yield of just less than 2.0%. As Chart 3 reveals, short rates typically run higher than dividend yields, not dramatically lower, as they are today. In fact, short rates on average over the last 35 years or so have stood a bit more than 200 bps above the index's dividend yield. Even in the unlikely event that firms add no more to their dividends, the equity market in this context could not rise enough to reestablish this historical norm. Obviously, this is no forecast, but it gives an idea of the extreme value imperative existing at the moment.

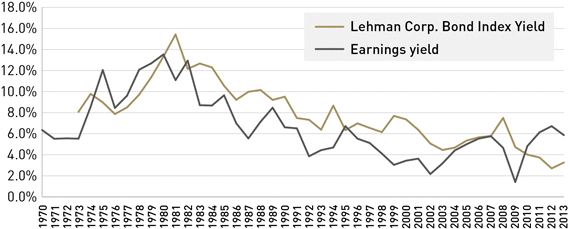

The comparisons to bonds are a little more complex, but no less compelling. The most common way to compare stock valuations to bonds is to invert the P/E multiple to express earnings as a yield on the price of stocks. This so-called earnings yield today stands near 6.0%, some 250 bps above the yield on the popular Barclays Corporate Bond Index.4 But, as Chart 4 shows, bond yields typically run above the stock index's earnings yield, not below it. Even in the unlikely event that earnings do not rise a jot and bond yields were to rise 150 bps, the multiple on the S&P 500 would have to rise to 40 times to reestablish the historical relationship to bonds, for a gain of more than 140%. Again, such an adjustment is implausible over any reasonable time span, but it does nonetheless give an additional perspective on the value imperative.

Source: FactSet.

Good to Great Return Prospects

No one pretends that these historical relationships will reestablish themselves anytime soon. There is a good chance, in fact, that rising bond yields and, in time, even rising short rates will begin to bring matters more into line from their side of the equation. But the gap is so vast that even in the face of rising rates and bond yields, it still gives ample room for a multiples expansion. It certainly leaves a powerful argument against any expectation of a drop in multiples, especially since at the same time the earnings figures look secure. With these parameters, it is possible to bracket market prospects using conservative and more aggressive assumptions.

On the conservative side, the place to start is with an assumption that the effect of operating leverage has run its course and that earnings going forward will only track revenues. There is actually every reason to expect operating leverage to continue to have its positive effect. According to the Federal Reserve, business still only uses 78.5% of its existing capacity, suggesting that firms have more to bring fully into production and so carry still more revenues to the bottom line. Even so, it suits a comfortable conservative baseline to assume an end to the operating leverage effect. On this basis, the consensus earnings growth expectation of about 6.0% this year looks about right. Nominal sales in the U.S. domestic market seem set to rise about 4%-2.5% real growth and 1.5% inflation. Since about half the S&P earnings come from overseas, much in the emerging markets, the overall revenue figure should come in closer to 5.0%. The per-share figures should edge higher because firms are doing a lot of repurchasing. Buybacks, according to recent figures, are running about 2.7% a year of outstanding shares, but accounting for options exercised and stock bonus plans, a 1.0% drop in outstanding shares should serve as a conservative figure. That gets to the consensus per-share earnings growth of 6.0%.

Source: FactSet.

If, to take a further conservative assumption, current multiples simply hold, then stock prices can rise in tandem with this expected 6.0% gain in earnings per share. The addition of the 1.9% dividend offered by the S&P 500 would then allow equities to offer investors a total return of about 8.0%, not the great gains of 2013, to be sure, but attractive nonetheless, especially given the alternatives in cash and bonds and that this is a conservative, baseline expectation.

But, of course, the above analysis shows that there is ample room for multiples to do considerably better than just hold at present levels. Without even suggesting additional help to earnings from operating leverage or that normal relationships to cash and bonds get reestablished anytime soon, a gain in multiples is far from out of the question, even as bond yields rise. Just for the sake of perspective, then, here are the total returns associated with various moves in multiples:

| Assumption | Total Equity Return | |

| The conservative baseline described above assumes an end to the operating leverage effect and no multiples expansion | 8% | |

| End to operating leverage effect and multiples move halfway to the 20x averaged in the 1990s | 13% | |

| End to operating leverage effect and multiples rise all the way to the 20x averaged in the 1990s | 24% | |

| End to operating leverage effect and multiples rise halfway to alignment with bonds after they have risen 150 basis points | 104% | |

| Source : FactSet. | ||

This is a wide range, and it shows the difficulty of any point forecast of the market. But it does give an idea of the potential, even in the absence of a lot of good news on economic activity or profitability.

2 All data within the article from FactSet.

3 The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

4 The Barclays U.S. Corporate Bond Index includes all publicly held issued, fixed-rate, nonconvertible investment-grade corporate debt. The index is composed of both U.S. and Brady bonds.

The opinions in the preceding economic commentary are as of the date of publication, are subject to change based on subsequent developments, and may not reflect the views of the firm as a whole. This material is not intended to be relied upon as a forecast, research, or investment advice regarding a particular investment or the markets in general. Nor is it intended to predict or depict performance of any investment. This document is prepared based on information Lord Abbett deems reliable; however, Lord Abbett does not warrant the accuracy and completeness of the information. Consult a financial advisor on the strategy best for you.