Mixed Economic data leads to quiet week in markets

An otherwise uneventful week led to mixed performance for equity markets, as the Dow Jones Industrial Average gained 0.1% and the S&P 500 Index lost 0.5%.

Economic data was equally mixed, with consumer data supportive of a better economic environment, but housing data posting weaker than expected numbers.

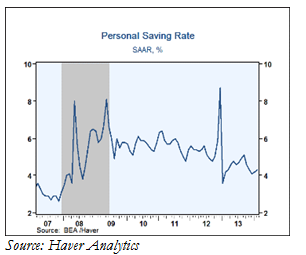

The February report on personal income & outlays offered a moderately positive snapshot of consumer income and spending in the month. Personal income grew 0.3%, matching the number seen in January. Following a patch of income declines in late 2013, recent strength is a welcome development for consumers.

On the other side of the ledger, consumer spending was up 0.3% in February, following a 0.2% increase in January. Spending was broad based, but a 0.7% rise in health care spending was one of the larger outliers.

Accelerated gains in income and moderate increases to spending ultimately bumped the personal savings rate higher. The savings rate continues to be at the lower end of its multi-year range, but it appears to have stabilized between 4% and 4.5%.

At the same time, consumer confidence showed another gain in March, jumping to 82.3, from 78.3 in February. Consumers were less enthusiastic about current conditions, but the expectations component showed a strong rebound. Interestingly, confidence grew in individuals over the age of 35, but fell sharply for people under 35. The consternation could be tied to concerns about the weak outlook for employment.

Source: Econoday

Housing markets received two bits of disappointing information, and one piece of good news. The disappointing news came in the form of new and pending home sales. In February, new home sales declined to an annualized rate of 440,000, down by roughly 15,000 from the previous month. Pending home sales also lost traction, dropping by 0.8% in February, which was the ninth consecutive month of declines. Strategists widely reported that difficult weather conditions were the culprit.

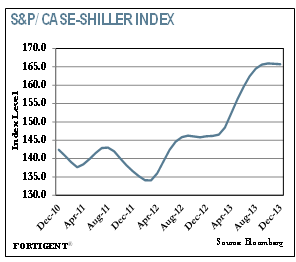

Despite weaker sales trends, home prices continue to exhibit strength. The Case-Shiller home price index gained 0.8% in January, and is now up 13.3% in the past year.

A Look At First Quarter Market Performance

As the first quarter draws to a close, equity markets appear poised to finish in positive territory despite a somewhat tumultuous news environment. As noted by Bloomberg, save for a sharply negative Monday period, the S&P 500 will close out a fifth consecutive quarter in positive territory for the first time since 2007.

A wide range of factors impacted first quarter performance, ranging from geopolitical tensions surrounding Russia’s annexation of Ukrainian peninsula Crimea, unusually harsh winter conditions that eroded economic growth, and Janet Yellen’s assumption of the chairmanship of the Federal Reserve. Idiosyncratic concerns in emerging markets such as Argentina and Turkey complemented broader fears of a slowdown in China to contribute to the negative global outlook.

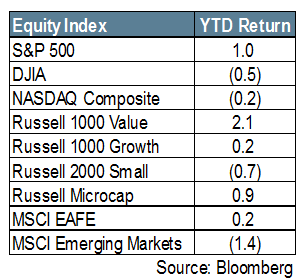

Despite this overhang, risk assets generally managed their way through the start of 2014. Through last Friday, the S&P 500 was up 1.0% on a total return basis (including dividends), while the Dow Jones Industrial Average was down 0.5% and NASDAQ was down 0.2%. While the Dow’s concentrated nature lends itself to some deviation from the other blue chip indices, the NASDAQ’s growth bias was a headwind as value stocks outperformed growth by approximately 2% across the market cap spectrum.

Small cap stocks, as represented by the Russell 2000 Index, were less immune to macro concerns as they struggled to a 0.7% loss. Micro cap stocks, on the other hand, added to their strong 45% 2013 with a gain of 0.9%.

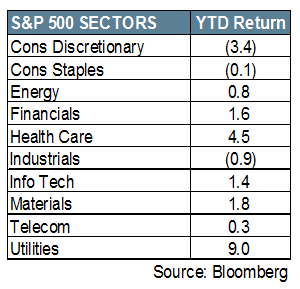

From a sector standpoint, 2014 returns have been highly barbelled. Healthcare stocks and utilities are by far the top winners of the year, with consumer discretionary and industrials lagging far behind. The rest of the group falls plus or minus the zero line by a couple hundred basis points. The month of March has wreaked havoc on these figures, with health care and discretionary falling by more than 2%, and telecom rebounding over 4% in the period.

Non-US stocks were similarly benign, with the MSCI EAFE essentially flat at 0.2%. Emerging Markets were slightly more disappointing, shedding 1.4%, largely as a result of some of the concerns we previously mentioned. That is a highly disappointing result for many who expected emerging markets to following last year’s 35% lag behind the S&P 500.

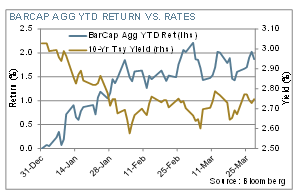

The surprise performer of 2014 thus far? Fixed income. Through March 28, the broadest measure of the fixed income markets – the Barclays Aggregate Bond Index – was outperforming stocks with a 1.9% return. High yield has done even better, rising nearly three percent through the first three months of the year as average option-adjusted spreads tightened.

Despite fears to the contrary, rates declined sharply in January as investors rebalanced from an extreme 2013-performance year and a sharp currency devaluation in Argentina incited a global flight to safety. This sent most of the broad fixed indices higher. The yield on the 10-year Treasury compressed from just over 3.0% at year end to a low of 2.6% in early February; since that time, rates have largely remained range bound.

So what do analysts believe is in store for the rest of 2014? The latest median consensus estimate for the S&P 500 for year-end 2014 is 1950, according to Bloomberg data. From current levels, that would suggest 5% of upside. Meanwhile, surveys across various sell-side research groups generally agree that equities are the most attractive asset class right now, with fixed income looking far less interesting – particularly after this year’s early retrenchment in rates.

Ultimately, earnings growth will drive 2014 returns; after a year in which multiple expansion was responsible for most of the equity market’s gains, fundamental improvement will be needed to propel this market forward. Second quarter earnings season, just one week away, should provide more insight on that front.

The Week Ahead

The economic calendar will be focused on Friday’s nonfarm payroll report, and current expectations look for a gain slightly above 200,000. Secondarily, markets will key in on the ISM Manufacturing report, factory orders, and the trade gap.

The central bank calendar is mostly quiet, but meetings in Australia, India, Brazil, and the Euro area will be closely watched for indications of easing, or comments on weakness in emerging market economies.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value