The growth of ETFs has been nothing short of tremendous. What started as a product designed to provide investors with broad equity or sector exposure in the US, the ETF landscape now includes a myriad of geographies (Europe, Asia) and asset classes (FX, rates, credit, commodities). Research consultancy firm EFTGI estimates that there are almost 5,000 ETFs globally with total AUM in excess of $2 trillion. This compares to less than 300 ETFs with total assets of just $168 billion 10 years prior. Amidst this impressive growth in products and assets under management, the increasing popularity of volatility linked exchange traded products (ETPs) stands out. In this note, we explore this growth and discuss the implications for this growth on the dynamics of the US equity derivatives market. We conclude that “this is not your father’s vol market”.

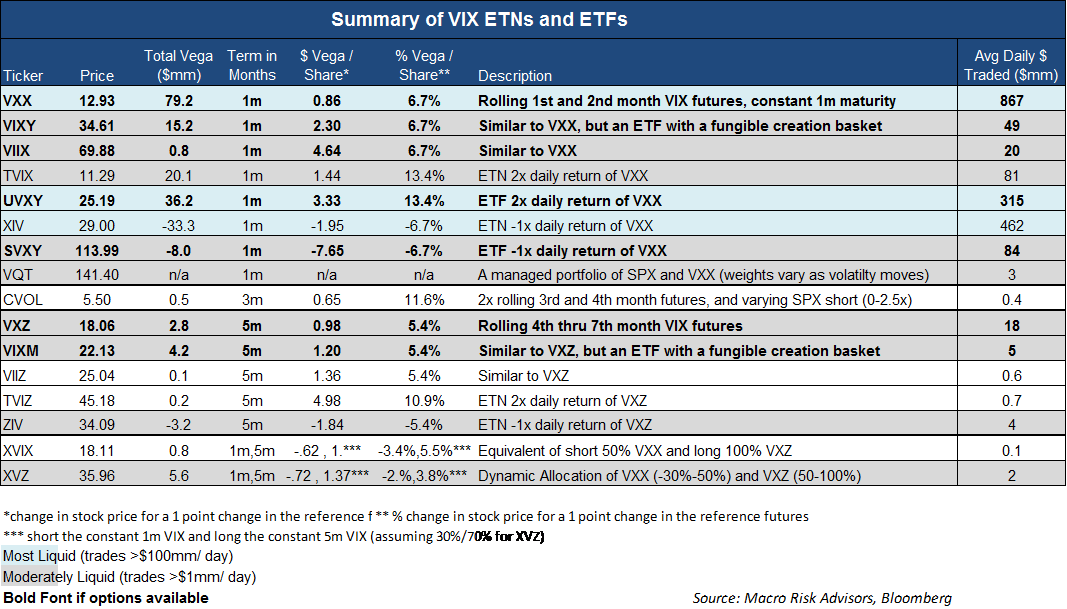

In January 2009, the VXX was launched. This exchange traded note provides exposure to SPX volatility through a mechanical strategy of owning a combination of the 1st and 2nd month VIX futures. Over time, the market for volatility ETPs has grown in complexity and is now comprised of leveraged, inverse, and curve focused volatility products. In fact, there are now even options on some of these leveraged volatility products creating leveraged volatility on leveraged volatility products! We provide a summary of the product set in the table below.

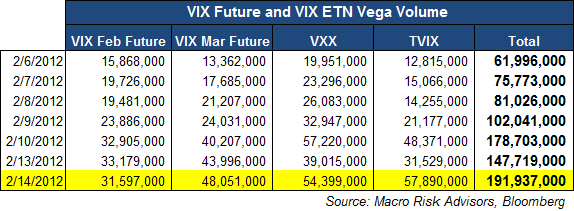

All told, the aggregate AUM for the VIX ETP universe is roughly $3.6 billion. Importantly, this constitutes approximately $200 million in option vega. The size, scope and impact of these new products came into focus in February 2012 as the shares outstanding of the TVIX (a 2x levered VXX) exploded in a short period of time. These inflows were substantial enough to cause a surge in VIX futures volume and to meaningfully move SPX implied volatility up and down. The table below illustrates this surge in volume.

Over time, as the market for VIX futures has continued to deepen, the US volatility market has adapted to the changing landscape of products and their implications. Accordingly, investors should be very cognizant of how volatility ETPs can influence pricing dynamics in the derivatives market.

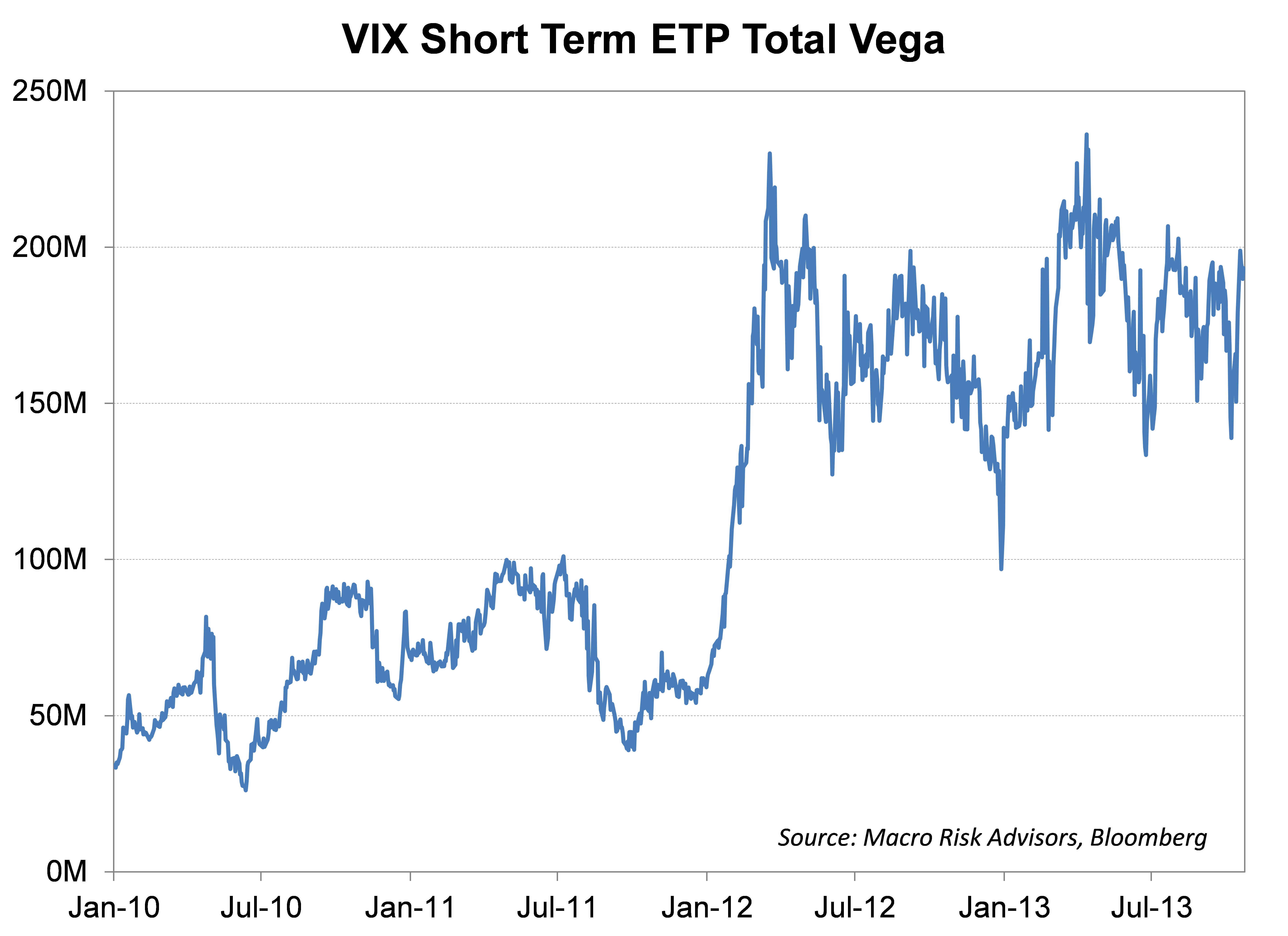

In the graph below, we show the vega of the 1st and 2nd month VIX future being indexed by large short-term VIX ETPs. These include the VXX, VIXY, TVIX, UVXY, XIV, SVXY and the front month weightings of XVZ. Notice the large jump in Jan/February of 2012 as a result of the TVIX growth. Interestingly, the assets under management have been pretty consistent over the past year and a half as investors have been more prone to trade these products on a daily basis and high frequency trading operations have become a larger part of the market.

These ETPs account for more than 1/3 of the net vega open interest of the front two months of VIX futures. One point to note is that some of the products are ETNs as opposed to ETFs and thus need only replicate the performance of the respective underlying index. Due to this distinction, ETNs do not necessarily need to hold the VIX futures, maintaining the flexibility to replicate the futures via SPX options or through OTC means like variance swaps.

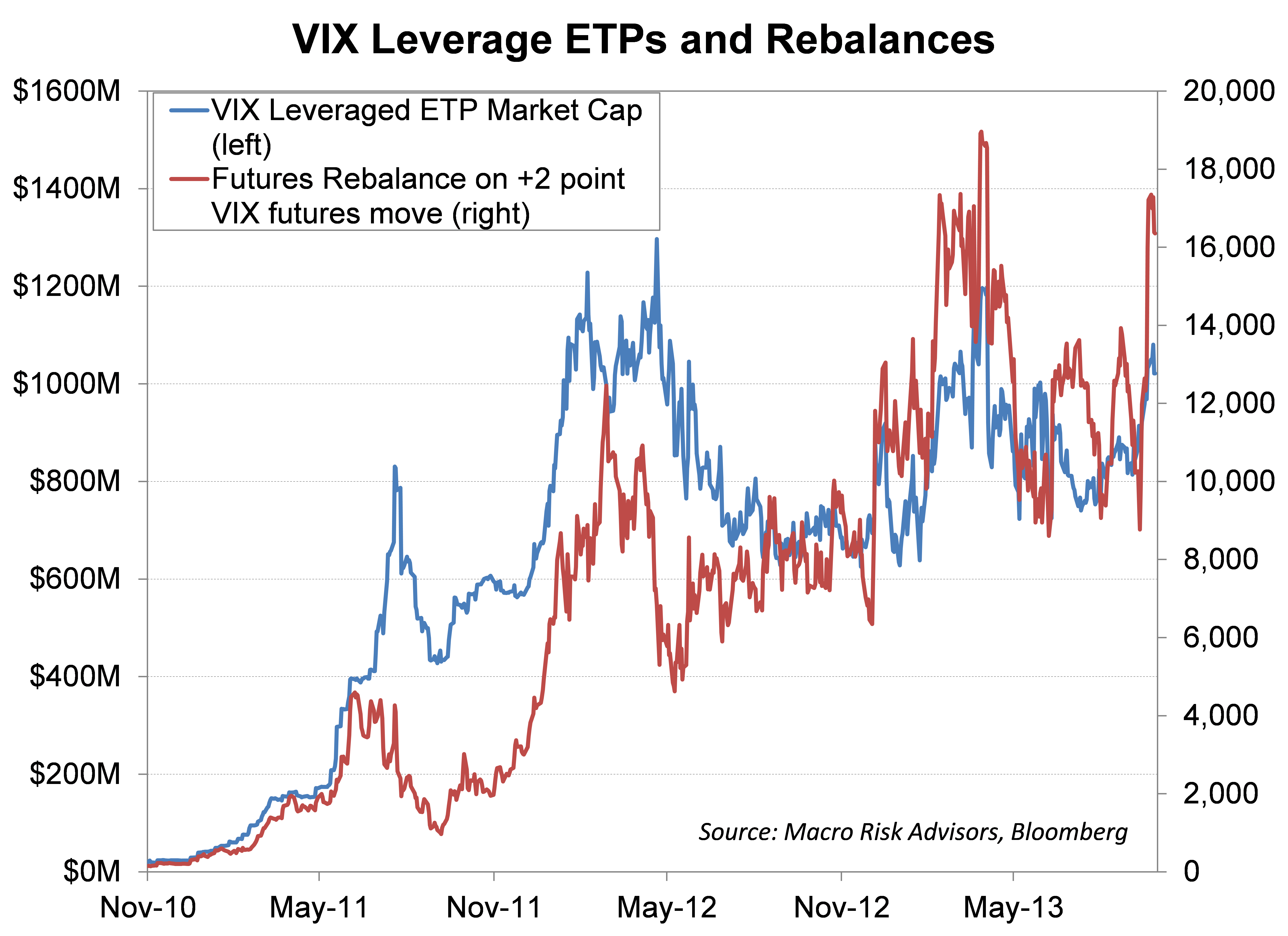

An important lesson from the February 2012 experience for the TVIX is around rebalancing of hedges for leveraged ETPs. The daily effort to rebalance near the end of trading can serve to accelerate the moves in implied volatility in the broader market. These leveraged products are forced to buy VIX futures when volatility is increasing and sell VIX futures when volatility is declining. In times of uncertainty when volatility is rising, the hedging requirements for leveraged ETPs can be substantial, potentially climbing in the face of an ever growing rebalance. Below we provide an illustration of how the rebalance can create a self-reinforcing demand for volatility. While US volatility levels are currently well behaved, this dynamic is certainly a factor to understand and watch for.

In the chart we show the market cap of the leveraged ETPs (TVIX, UVXY, XIV, and SVXY) and the total theoretical end of day rebalance required for +2 point move up in the 1st and 2nd VIX futures basket. If the futures are up on the day, the leveraged ETPs will need to buy futures to rebalance and the opposite if futures are down. The red line shows that currently a +2 point move in the front month future would necessitate the buying of 16,000 VIX futures to the close.

This clearly can have large effects on the market, especially on risk off days that result in huge end of day vega to buy. Conversely, the VIX has exhibited a tendency to drop much faster than had been the case prior to the introduction of leveraged volatility ETPs. For example, the volatility market experienced extreme moves to the downside following the resolution to the fiscal cliff in December of 2012. At that time, the front month VIX future dropped 20% from 12/28 to12/31 and a further 12% the next trading day. On 12/31, VIX leveraged ETPs needed to sell 13,400 futures followed by 8,200 futures the next trading day compared to an average daily volume of 50,000 contracts for the front month VIX future contract. In these risk on/risk off events, one can quickly see how the broader equity market is affected by large moves in VIX futures.

To be sure, the growth of volatility based ETPs has complicated the world of hedging for investors. Much education remains necessary for users of these complex products. As the academic founder of the VIX, Robert Whaley recently said, ETFs on the VIX are “virtually guaranteed to lose money through time”. Such is a mathematical certainty in a persistently upward sloping implied volatility term structure. The flip side of this is that carry strategies that harvest the volatility risk premium have grown in prominence and been an important source of return in a low yielding environment. While these trades are certainly crowded, opportunities remain. However, they must be implemented with careful attention to risk control. The preceding discussion and analysis illustrates that in a substantial risk off event a large spike in volatility would create huge demand for VIX futures as leveraged VIX ETPs rebalance exposures.

Dean Curnutt is CEO and Danny Kirsch is a Strategist at Macro Risk Advisors.

MRAD <go> on Bloomberg