Choppy Week Ends Higher

Equity markets finished higher last week despite a sharp sell-off on Friday. Ironically, Friday’s decline followed an initial gap higher that pushed the S&P 500 to an intra-day record high. For the week, the S&P 500 gained 0.4% while the Dow Jones Industrial Average climbed 0.6%.

Investors were treated to a few important economic data reports in the lead up to Friday’s government jobs report. The general tone of data last week was one of tepid improvement in the US economy.

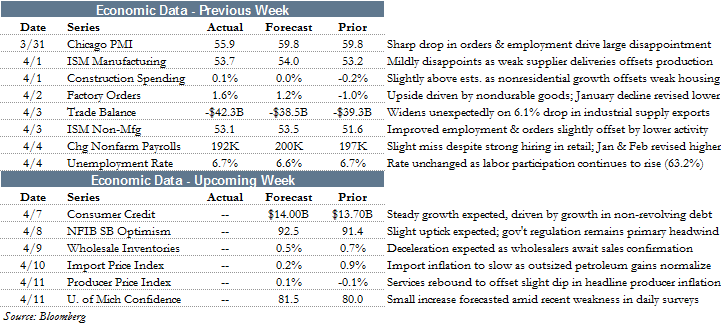

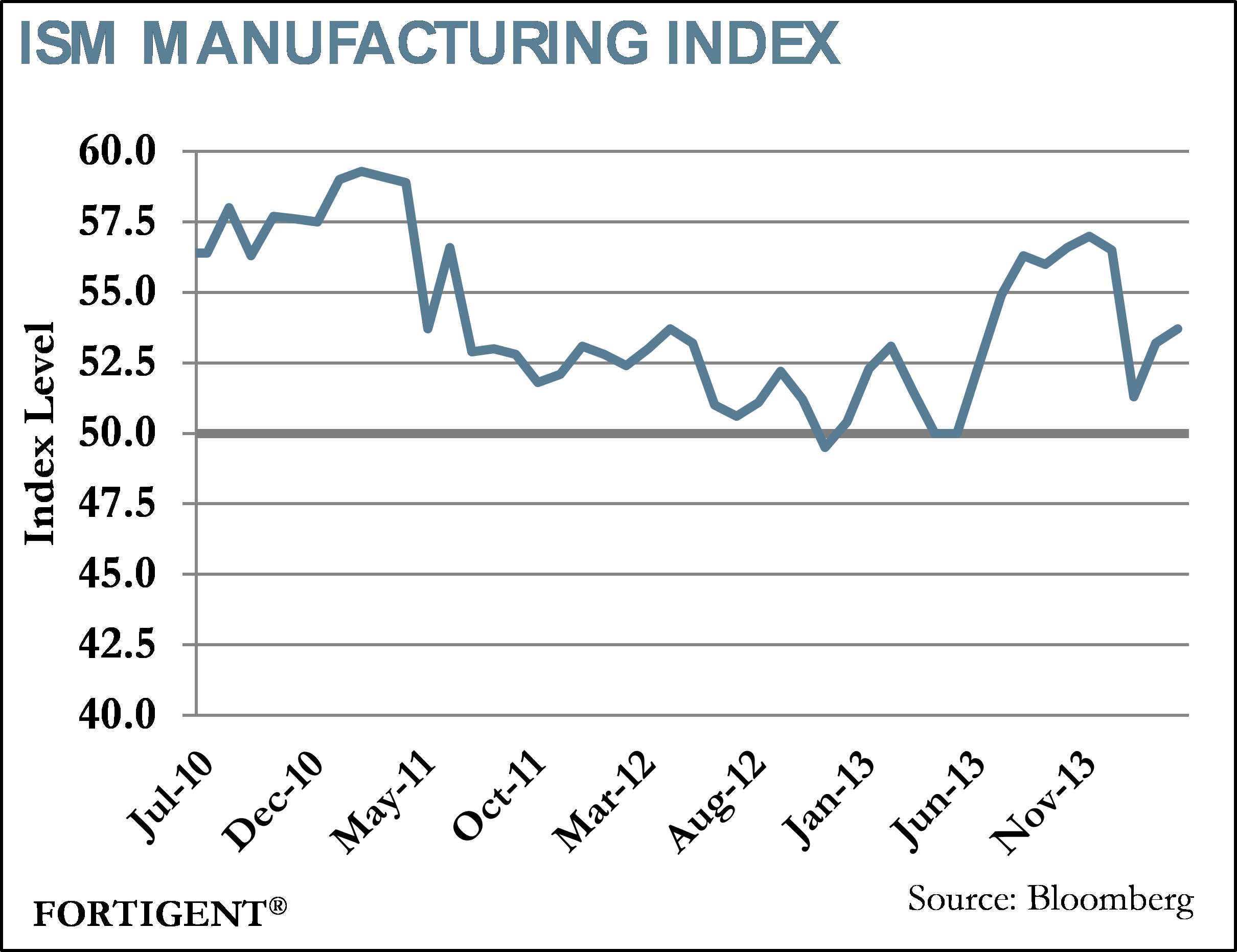

On Tuesday, the Institute for Supply Management (ISM) released its monthly diffusion index regarding the state of the manufacturing industry. March’s reading came in at 53.7, a modest improvement from February’s 53.2level and a few tenths under consensus estimates. Nevertheless, the index remains far healthier than that observed in January, when the measure plunged to 51.3.

Under the surface, the ISM Manufacturing report was invariably mixed, with five components increasing and five components falling flat or negative. The index’s key component, new orders, did improve marginally. Always important production surged nearly 8 points to rebound from contractionary territory. On the negative side, employment and supplier deliveries fell. ISM Chairman Bradley Holcomb noted, “Several comments from the panel reflect favorable demand and good business conditions, with some lingering concerns about the particularly adverse weather conditions across the country.”

Further information on the manufacturing sector was made available via the Census Bureau’s factory orders report. Following two consecutive month declines, the measure of new orders for manufactured goods increased 1.6% in February. Shipments also rebounded following two soft months, increasing 0.9%.

According to the Census release, transportation equipment led the February increase with a 7.0% gain. Consumer durable and non-durable goods were also positive, as well as motor vehicles and parts. Capital goods were highly bifurcated: while defense capital goods were up a whopping 13.7%, nondefense goods contracted by nearly 3%. General softness in the manufacturing space outside of aircraft, motor vehicle, and the defense industry is a source of consternation for many economists.

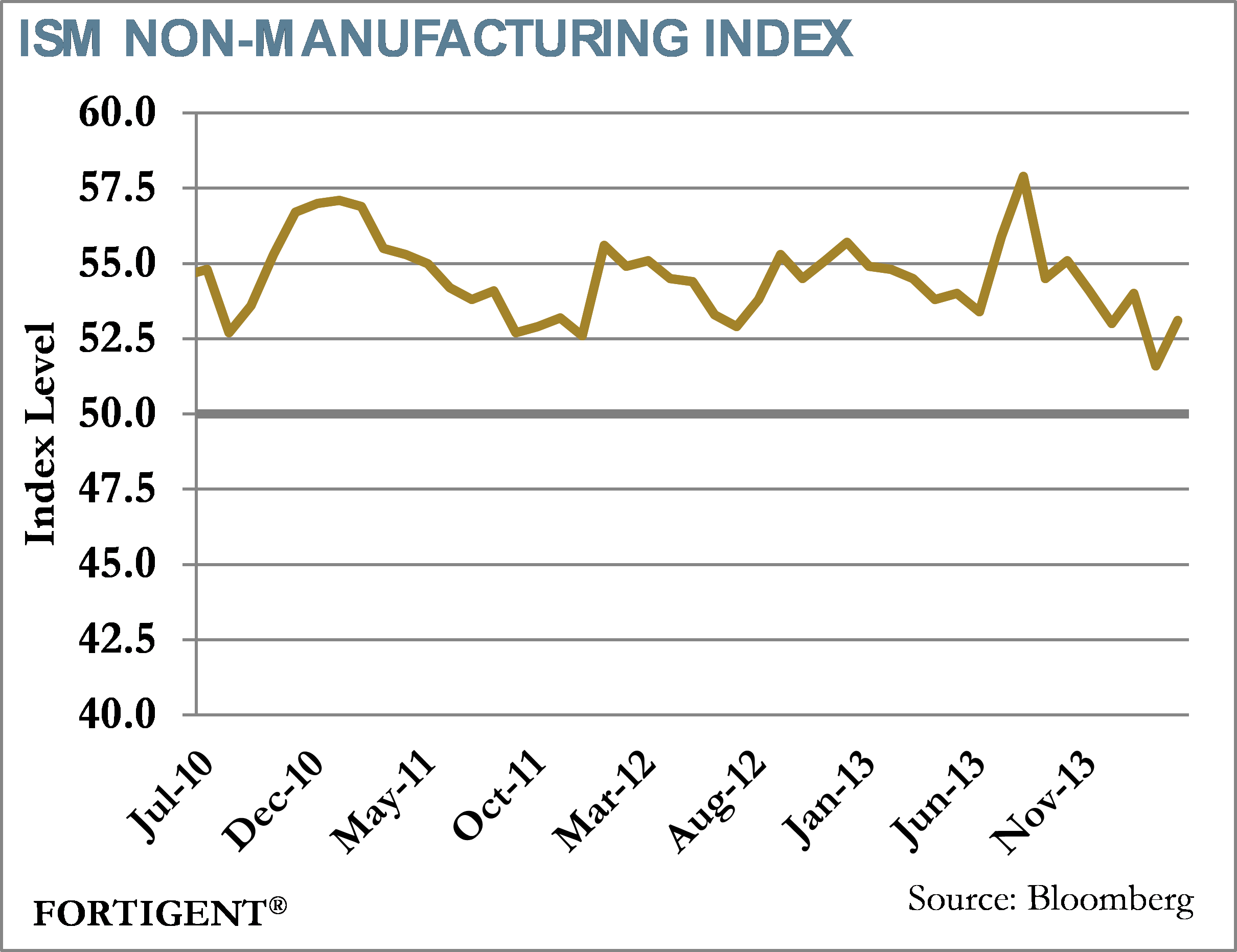

On Thursday, ISM’s complementary Non-Manufacturing Index was released. The less heralded report posted a solid gain of 1.5 points to 53.1, suggesting the US service economy remains healthy. By component, employment exhibited the strongest gain, increasing from 47.5 to 53.6. New orders also increased, and that component has now been in expansionary territory for 56 straight months.

LABOR MARKETS LOOKING FOR A SPRING BLOSSOM

With an unusually harsh winter finally ending, economists were excited to see if labor markets would rebound in March. By many accounts, they were left wanting for more, but the underlying theme in the March report was consistent, steady job growth.

Recapping the numbers, the economy added 192,000 jobs in March and the unemployment rate held steady at 6.7%.The government sector added zero net new jobs in March, placing the onus of growth on the private sector last month.Within the private sector, growth came from a number of sectors including professional & business services, education & healthcare, leisure & hospitality, retail, and construction.Manufacturing was one of the only areas to lose jobs, shedding approximately 1,000 jobs in March.

Structural issues continue to plague labor markets, though, from extended unemployment to a high number of people dropping out of the labor force.

According to the latest figures, there are 10.5 million unemployed individuals and 3.7 million of those have been out of work for 27 weeks or longer.The average number of weeks unemployed currently stands at 36.2, down from the peak of 42 in April 2012, but well above any prior peak.

Source: Federal Reserve Bank of St. Louis

A challenge for labor markets has been the declining participation rate in prime working age individuals (25 to 54 years old).This is a phenomenon that began well before the recession, but it has only continued because of the crisis.The only segment of the population showing an uptick in participation has been 55 and over, suggesting that many baby boomers are not ready to depart the workforce for various reasons, not least of which was the decimation of their retirement savings in 2008.

Source: Calculated Risk Blog

The positive news is that overall employment is only 0.3% below its pre-recession peak and private sector payrolls are at a new all-time high.While this does not account for recent population growth and new entrants to the workforce, it does suggest labor markets are loosening up and gradually getting better.Conversely, the Brookings Institution estimates that after accounting for new entrants to the workforce, there is still a 7.7 million “job gap.”Under average scenarios, the job gap will not dissipate until September 2018.

Source: Federal Reserve Bank of St. Louis

The March labor report was solid, but did not register the robust growth rate many were hoping.Severe weather conditions in portions of the country were expected to give way to a blossoming early spring labor market, but that simply did not happen.Any expectation that labor market improvement is accelerating is likely misguided based on recent trends in participation rates, average weeks unemployed and the stagnating unemployment rate.So long as labor markets remain fractured, the Federal Reserve will be expected to play a role in reviving those markets.

The Week Ahead

Economic data is on the light side this week, with NFIB’s Small Business Optimism Index and FOMC minutes among the highlights. Consumer sentiment and the producer price index are also on tap for Friday.

Earnings season unofficially gets under way this week, with Alcoa reporting on Tuesday and J.P. Morgan and Wells Fargo reporting on Friday. Extreme cold weather in the first quarter is expected to have an adverse impact on earnings to be reported over the next few weeks.

The Bank of Japan gathers for a scheduled two-day meeting starting Tuesday. Analysts do not expect any major deviation in policy. Additionally, the Bank of England meets on monetary policy on Thursday. Other countries meeting include Indonesia, Poland, Sweden, Peru, and South Korea.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value