Predatory Trading ? Just How Big an Issue is High-Speed Trading?

High-frequency trading (HFT) is a topic institutional investors and traders have been battling for years. A new book titled Flash Boys by author Michael Lewis of Moneyball fame, investigations out of U.S. regulators and a 60 Minutes spot on a recently developed exchange, IEX, brought this topic from Wall Street to Main Street. In this article, we’ll take a walk around the issue, educate our investors, and hopefully, quell any concerns.

Before we dive in, let’s look back to a spring day in 1792 when 24 stock brokers gathered under a buttonwood tree at 68 Wall Street and signed an agreement that established the New York Stock Exchange. The NYSE was to be a non-profit entity that was run for the greater benefit of public companies – the heart of U.S. equity capital markets. Since its establishment, the U.S. equity market structure has evolved. Yet it always remained the hub where U.S. and foreign companies would access capital and list for their shareholders’ benefit.

In 1972, the SEC became concerned when stock prices at regional exchanges (Chicago, Pacific, Boston) would vary from the price on the NYSE, the primary listing. This inefficiency was an opportunity for predatory trading – fast traders who would buy and sell on different regional exchanges, commit little capital and capture only the spread. In 1975, Congress authorized the SEC to enact a national market system. From 1975 – 2001, the U.S. equity market structure was simple – a listed auction market on the floor of the NYSE and over the counter market, NASDAQ. The structure was in near perfect alignment with the agreement signed centuries prior – a non-profit entity run for the greater good.

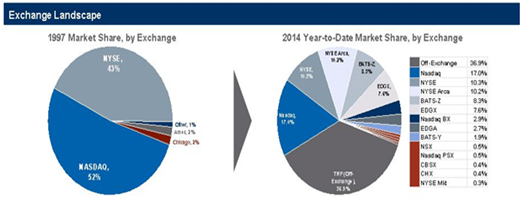

The 2000s were marked with much regulation, culminating with Regulation National Market System (Reg NMS) in 2007. In the 2007 version of Reg NMS, the regulators aimed to promote competition among exchanges and allow for greater ‘access’-- an effort to harmonize quotes across different exchanges and trading centers. In the years that followed, new exchanges, dark pools and alternate trading systems (ATS) were formed and the U.S. equity markets fragmented (Exhibit 1).

Exhibit 1:

In less than seven years, we broke our simple structure, injected competition and fragmentation, and high frequency was born. Today in the U.S., we have 13 exchanges and an estimated 50 dark pools and ATS. High-frequency is a general term that includes many strategies. Some, quite frankly, are harmless; some are more predatory in nature. The more predatory natured high-frequency strategies are highlighted in Lewis’s latest book and will be the target of regulator investigations. The first focus will be on latency arbitrage. With faster connections to exchanges, high-frequency firms are able to get faster signals, and “jump ahead” of slower orders. With significant investments in technology, HFT traders hold a big speed advantage, which has yielded huge profits.

Example: An HFT firm places a sell order on an exchange. When executed, HFT signaled: “There is a buyer of the stock.” HFT quickly race to take supply from all other exchanges. More times than not, the stock price then slides higher and HFT sells stock at a higher price. Buyer loses; HFT wins.

While HFT is a new term to many, there are many gray hairs on investment managers heads as we fight to protect our clients. Through years of rigorous and detailed analysis, most investment managers have effectively fought back. Minimum fill rates, venue analysis and frequently querying brokers for detailed analysis all work to protect our clients’ execution. While investment managers invested heavily in speed and joined the race, some of us decided to tap the brakes and relevel the playing field at the exchange level. At Columbia Management, we have embraced the work of IEX (60 Minutes, 3/30/14) and will continue to stand with any firm or exchange that focuses on what is best for the integrity of the execution vs. what’s best for the bottom line of the exchange/broker. IEX is a venue with a large speed bump on the entrance ramp. The speed bump eliminates speed advantage and removes the HFT “edge.” Execution on a level playing field is good for our clients, and thus something we embrace.

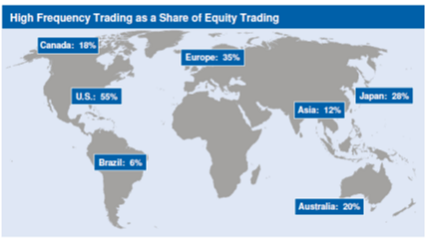

Developments in recent weeks increased the amplitude of concerns regarding HFT. As a result of awareness, predatory HFT firms, exchanges and Wall Street dealers in the U.S. will be forced to answer difficult questions. We believe the opportunity for HFT in U.S. equity markets has peaked. However, inefficiency will reappear in other asset classes or regions around the globe (Exhibit 2). Columbia Management will continue to face this directly and implement tools to protect our clients’ best interests. We stand with those original 24 brokers – a U.S. capital market structure maintained for the greater good of the companies and their investors.

Exhibit 2:

Source: RBC Capital Markets

Disclosure

The views expressed are as of 4/7/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

897382