We get a lot of questions regarding the impact on portfolio risk of having an allocation to gold. In particular given the status of gold as a safe haven asset, focus has centered on its performance during periods of extreme market stress – what is the downside to gold during periods of high risk aversion? The high level answer to this question is that the financing currency used to make the gold purchase matters and as is often the case when discussing portfolio construction, “you ask a simple question, you get a complex answer”.

In last week’s discussion piece we presented an historical analysis of the relationship between gold financed in US dollars and the value of the dollar on currency markets. When an investor buys gold priced in dollars, they are explicitly expressing the view that they expect the price of gold to increase relative to the dollar. As such we would expect the price of gold in dollars to be at its highest when the value of the dollar (against a range of currencies) is at its lowest. And this is indeed the relationship we observe where the price of gold tends to move inversely to the value of the dollar on currency markets. Similarly when an investor buys gold financed in yen they are expressing the view that they expect the value of gold to increase relative to the yen. Further, we would expect the price of gold in yen terms to be at its highest when the value of the yen on currency markets was at its lowest. Following this line of reasoning we return to the original question posed at the beginning of this article and it becomes clearer why financing currency matters. The performance of gold during periods of market stress will be a function of both the value of gold versus the dollar and the value of the financing currency on currency markets.

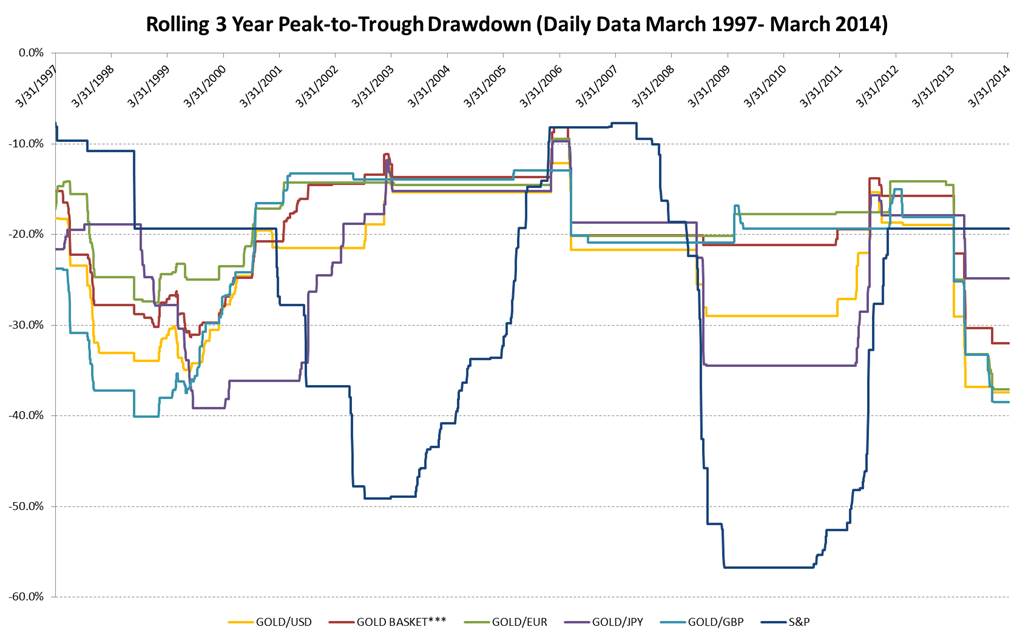

In this analysis we use the three year peak-to-trough drawdown as our measure of stress in financial markets. The chart below shows the historical peak-to-trough drawdown of an investment in gold financed in the number of different currencies – the dollar, euro, yen and pound as well as gold financed with an equally weighted basket of the four currencies with daily rebalancing (the Gold/Basket). For comparison we include data for the S&P 500. The chart is constructed using end of day daily data and as such does not capture intra-day volatility. The time series starts in 1997 so as to fully capture the market dynamics leading up to and beyond the bursting of the tech bubble in 2000.

Source: Bloomberg, LP; Treesdale Partners calculation. Gold basket is gold financed with an equally weighted basket of euro, yen, sterling and dollar, rebalanced daily. Past performance is not an indication of future performance.

There are a few interesting observations from the chart. Firstly, the large variability in the drawdowns incurred by each of the strategies. In each case the difference in the drawdown performance of a given strategy relative to Gold/USD was a function of the performance of the financing currency relative to the dollar. For example the large outperformance of Gold/GBP and Gold/Euro in 2008 during the height of the credit crisis was driven by the steep falls in the value of both the pound and euro versus the dollar. Secondly despite the variation in the drawdowns of the gold strategies, the troughs in their drawdowns broadly occurred at the same time i.e. despite the differences in financing currency the gold risk factor was still a key determinant that impacted drawdown performance. Thirdly the troughs in the drawdowns of the gold strategies tended not to coincide with the trough in the S&P drawdown indicating a certain degree of independence in the risk factors that drove their relative performance. Finally we note that the Gold/Basket had consistently similar or better drawdown performance relative to Gold/USD. This should be unsurprising as we have noted in previous commentaries , a gold position financed with a number of different currencies would be expected to gain some diversification benefit from the diversity in financing currencies versus a gold position financed entirely with dollars. The key takeaway perhaps for medium to long term gold investors that have an allocation to gold in their portfolios would be to consider using a “currency basket” financing strategy when making gold purchases which can potentially provide diversification benefits to investors which feed directly into better drawdown performance during periods of high market stress.