Stocks Slide in Quiet Week of Economic Data

Stock markets fell sharply last week, despite a lack of major negative news and positive intimations from Fed minutes released Wednesday. The Dow Jones Industrial Average shed 2.3% and S&P 500 fell 2.6% on the week, pushing both indices into negative territory for the year.

FOMC minutes from the Fed’s March meeting painted a more accommodative picture than first observed in last month’s press release. Many interpreted the removal of the unemployment rate threshold for initial rate hikes as a hawkish move. However, the transcript suggests the change was made to stave off a premature hike: "With respect to forward guidance about the federal funds rate, all members judged that, as the unemployment rate was likely to fall below 6.5 percent before long, it was appropriate to replace the existing quantitative thresholds at this meeting." Equity markets moved higher on the report, but sharp losses on Thursday and Friday pulled the indices lower.

There was limited economic data for investors to digest last week, with the National Federation of Independent Businesses (NFIB) Small Business Optimism Index headlining the week’s reports.

The NFIB measure increased by 2.0 points, partially offsetting a sizable decline in the previous month. As noted by NFIB Chief Economist Bill Dunkelberg, however, the index continues to come in below 95.0, a level that has served as an upper bound since the recovery began five years ago. The index regularly stood above 100 prior to the financial crisis.

Six of the 10 component factors improved in March, led by expectations about real sales levels. Plans to increase inventories also experienced a significant gain. Slight declines were observed in business owners’ plans to increase employment and make capital outlays. Meanwhile, taxes and government regulations remain the biggest problems faced by small businesses.

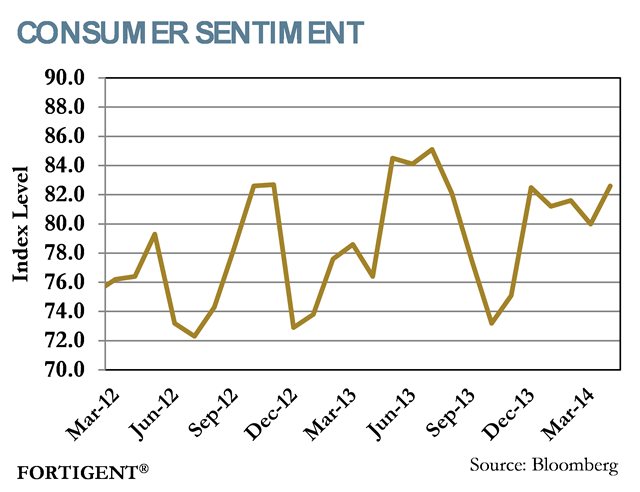

On Friday, the Reuters/University of Michigan Consumer Sentiment index reached its highest level in nearly a year, increasing to 82.6. At month-end March, the measure stood at 80.0. Both the current conditions and expectations components of the report improved, to 97.1 and 73.3, respectively. Gains in the expectations component is a turnaround from earlier measures, as more

optimistic views on the current state of the economy helped carry the headline figure higher.

From an earnings perspective, last week’s start to the season began in mixed fashion. While Alcoa’s earnings topped estimates (though revenues missed), J.P. Morgan’s first quarter figures came in below expectations as mortgage revenue and fixed income trading revenues declined sharply. Wells Fargo, on the other hand, surprised to the upside with a 14% gain in first quarter profits. The latter benefited from lower loan losses (down 41%) and trimming expenses in the period. Analysts generally expect first quarter earnings season to be challenging given the abnormally harsh winter conditions over the past few months.

Complacency Makes Volatility Markets a Dangerous Place

With a dissipation of economic stress in Europe, and a general strengthening of economic conditions in the U.S., equity market volatility has plunged to new lows. Some would argue that market intervention by central banks is acting as an unnatural dampener to market volatility, raising the question as to whether a gradual removal of those policies will cause volatility to resurface. So far, the answer is up for debate, but current positioning suggests many investors are becoming complacent and will be caught off sides if such a scenario emerges.

At the end of last week, the CBOE SPX Volatility Index closed at 17, right in line with its primary range of 12 to 18 in the past twelve months. Relative to 2011, when the European debt crisis was near its peak, the VIX was hovering around 45, nearly triple the current level.

Source: StockCharts.com

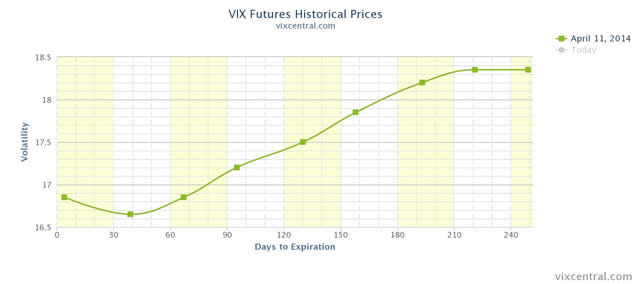

Volatility has gone through very brief spikes higher during the past year, but many of those volatility spikes have not been sustained. Somewhat interestingly, during last week’s sell off, we reached a point where short-term VIX futures were trading higher than next month contracts, a sign that traders were concerned about near-term volatility more so than intermediate-term volatility. This has been a classic pattern recently, showing that traders believe markets will generally snap back after any brief retrenchment.

Source: Vixcentral.com

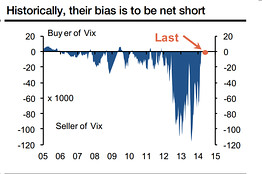

Historically, it has been commonplace for hedge funds and other institutional buyers to sell volatility, collecting a premium as they provide investors the ability to wager on a pickup in volatility. Given the compressed nature of volatility recently, those institutional buyers are vanishing, a clear indication that they do not believe there is enough premium to collect in advance of what many assume will be a rising volatility environment.

Source: Barron’s

Looking forward, natural geopolitical tensions, along with the pending finale of quantitative easing, suggests that volatility is only likely to move in one direction – higher. There is particular concern that the Fed’s botched attempts at providing forward rate guidance are setting the market up to be disappointed throughout 2014 and into 2015.

As Janet Yellen adapts to her new role as the head of the Fed, there are bound to be miscues and missteps that market participants are not prepared to grapple. Those events make it likely that volatility will resurface, creating new opportunities for investors with long volatility exposure in their portfolios.

The Week Ahead

Economic data picks back up this week, with retail sales, consumer prices, industrial production, and housing starts. The Fed also releases its latest edition of the Beige Book, a compendium of economic activity across the country that helps inform the central bank’s view of the country.

Important indicators such as retail sales, industrial production, and GDP are also due from China this week. Recent data suggests a material slowdown in economic growth; consensus expects first quarter GDP to slow to 7.3% YoY from 7.8% the previous quarter.

Central bank rate policy announcements are due from Canada, Egypt, Serbia, and Chile this week.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value