“Get your facts first, then you can distort them as you please. ”

– Mark Twain

“The beat goes on, the beat goes on

Drums keep pounding

A rhythm to the brain

La de da de de, la de da de da”– Sonny Bono

“Just because everything is different does not mean anything has changed. ” – Irene Peter

Greetings from a thawed out Savannah! Q1 of 2014 will be remembered for a number of things, but the most prominent were the erratic weather patterns and arctic-blast temperatures that most of the country experienced. I missed writing my Q1 letter for the first time in ten years due to a nasty bout with pneumonia in mid-January. For those of you who have never had pneumonia, I do not recommend it! However, one of the outcomes of my illness was that our readers missed my first-of-the-year prognostications, which is probably a good thing, as I have always found those annual predictions make you look far smarter or dumber than you deserve. However, time waits for no one, and for the remainder of the year we are focused on the following:

- Vladimir Stepping Over the Line

- Affordable Care Act Gone Wild

- China – What to Believe

- Japan and Currency War

- The Fed Is All That Matters

VladimirStepping Over the Line

Vladimir: You draw line in sand with Syria?

Barack: Yes.

Vladimir: And Syrians step over line?

Barack: Yes.

Vladimir: And America does nothing to enforce line?

Barack: Yes.

Vladimir: Ummmm… We take back Ukraine.

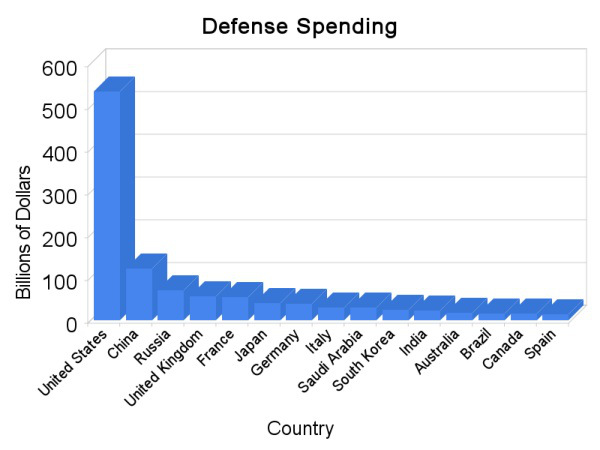

On March 3rd, Russia decided to take back a piece of the mother country and essentially invaded Ukraine. This international military action should act as a stimulant to the defense industry and comes just in time, as the US Congress is debating cuts in defense spending. Tax dollars will flow needlessly to build aircraft, cruise missiles, drones, and other defense weapons. In my opinion, Americans have grown weary of supporting the US as the policeman of the world. And frankly, most of the world has tired of the US trying to enforce its will in foreign lands where we are seen as the problem and not the solution. Vietnam, Iran, Iraq, Syria, and Afghanistan have proven to be US policy and military failures, as conventional wars are being replaced by cyberwarfare and terrorism. Americans want to see the billions of dollars that are currently being spent overseas diverted back home to fix roads, maintain other critical infrastructure, and fund schools that effectively prepare graduates for 21st century jobs, spurring economic growth in the USA.

From the graph above it is clear to me that in order to attack US budget woes, cutting defense and letting the rest of the world fight their own battles is in our best interest. The recent events in Syria and now the Ukraine have exposed the underbelly of the US military and our inability to take on multiple police actions in foreign lands. Invasions of foreign lands have a poor track record of restoring order in countries with a history of despotism and dictatorship. As painful as it is to watch the citizens of an Egpyt or Iraq take years to choose and elect their form of government, US intervention only puts a band-aid on a flesh wound and earns us a bad rap in the eyes of the world.

Medicare, Social Security, and national defense are inefficient and unsustainable in their current forms. If the US is going to become a fiscally responsible country again, then conservatives need to stop pretending defense can’t be touched, and liberals need to cease their wailing over entitlement programs.

“ But each proposal must be weighed in light of a broader consideration; the need to maintain balance in and among national programs – balance between the private and the public economy, balance between the cost and hoped for advantages – balance between the clearly necessary and the comfortably desirable; balance between our essential requirements as a nation and the duties imposed by the nation upon the individual; balance between the actions of the moment and the national welfare of the future. Good judgment seeks balance and progress; lack of it eventually finds imbalance and frustration.” – President Eisenhower

The Un-Affordable Care Act

What have I learned during 2014 tax season? Virtually every Excelsia client has commented they are paying more taxes this year than last, and the reason: ObamaCare, 3.8%. Healthcare costs continue to escalate. The combination of Baby Boomers entering retirement and thus drawing benefits from Medicare and Medicaid and the already-retired living longer makes the current system unaffordable. In 1967, when Congress originally forecast the long-term costs of Medicare, they thought that in 1990 Medicare would cost taxpayers $12 billion. The actual cost in 1990 was $110 billion. I predict we are in for a similar fate with the Affordable Care Act, due to the following factors:

- No risk premium is being paid for pre-existing conditions.

- No risk premiums are paid for age.

- Many among the healthy and the young are opting not to enroll in the program.

- An unhappy populace that knows they were deceived with the promise that they could keep their existing healthcare plans will vote for change in 2014.

My son is 22 years old, a student in accounting at Georgia State who last year earned just under $9,000 while working and going to school. He is faced with paying a monthly premium of $300 to be insured under the Affordable Care Act. His response to me:

“Why should I pay over $3,600 a year for insurance? I am young, healthy, and rarely go to a doctor. And if I do get sick or have a serious illness that requires hospitalization, then because I can’t be refused insurance for pre-existing conditions, I will go buy the insurance coverage if I need it.”

The Achilles heel of ObamaCare will be the failure to convince the population under the age of 35 to enroll and pay premiums. Add to lackluster enrollment the costs of covering pre-existing conditions as if they didn’t exist, and I fear our government has created a monster that resembles the vicious blood-sucking plant in Little Shop of Horrors: “Feed me, Seymour!” But what will we feed the Un-Affordable Care Act when premiums fail to cover claims and tax revenues decrease as more Americans try to control their level of taxable income in order to qualify for insurance subsidies? Why, more Fed-printed money of course!

From an investment perspective, we continue to see the Affordable Care Act as an impediment to business hiring and GDP growth. Corporate investment for future expansion will remain on hold until the CEOs and CFOs along with their boards have some assurance as to what their future liabilities will be under the Affordable Care Act.

“We have to pass the healthcare bill so you can find out what is in it. ” – Nancy Pelosi

American business is still trying to find out what’s in it!

Peering Over the Great Wall

What can we believe is going on in China? We read reports of impending loan defaults, a potential credit crunch, and possible contagion chaos in banking from failed derivative trades, all or any of which could cause another major financial crisis. I have seen the pictures of empty cities, the contamination of water supplies, and the ever-present air pollution. But what are we to believe?

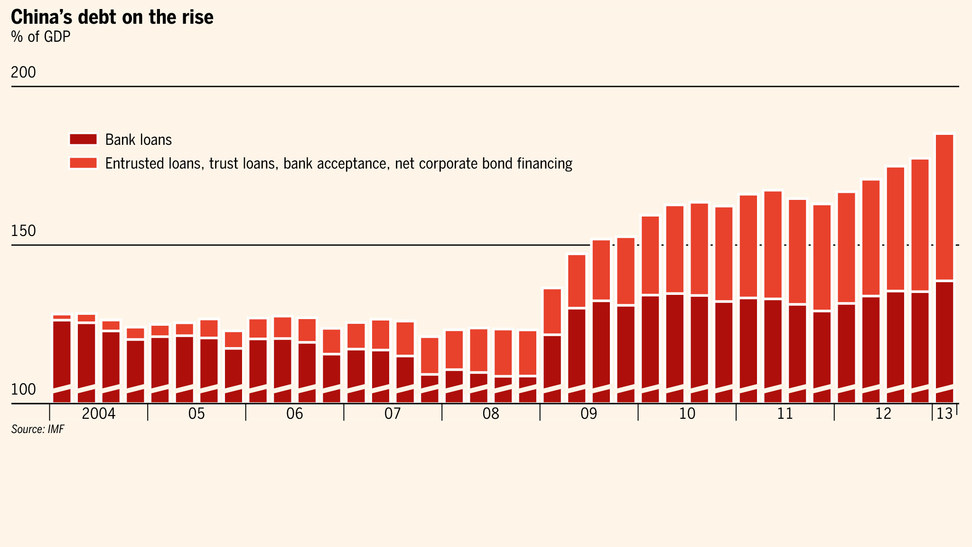

After the Chinese government allowed its currency to appreciate for most of 2013, the yuan collapsed in February of 2014, probably in response to declining Q1 China GDP numbers. I view the slowdown in China as a positive, not a negative, because China’s leadership is demonstrating a commitment to move to a more balanced and sustainable growth model as opposed to the current borrowing and investing in order to prop up growth. The short-term borrow-and-invest approach works for a while, up and until debt rises out of control and investments become less productive. As illustrated in the graph above, credit in China held steady at 130 percent of GDP for much of the 2000s. However, post-2008 it has shot up to nearly 200% of GDP, which is an increase of 55% in five years.

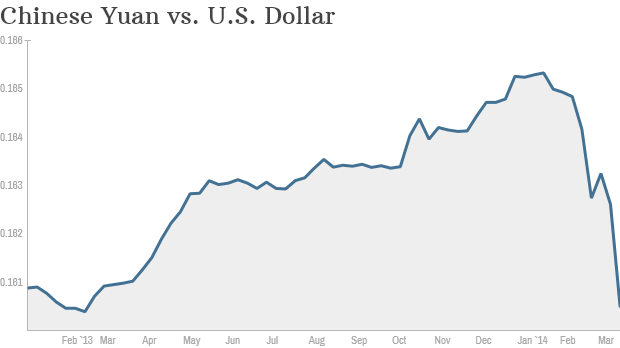

Not surprisingly, there has been a highly energized building boom over the past decade in China, with a tsunami of credit flowing into the system. Question is, will the government back the financial sector once the growth eases and defaults mount? There is a phrase in banking: “A rolling loan gathers no loss.” The question is, how much longer can Chinese private banking roll the economy? And more importantly, will the government continue the reforms needed to stabilize the country’s growth? The chart below shows the value of the yuan versus the dollar over the last year. China’s leadership obviously thinks a cheaper yuan is in the best interests of China.

China will no doubt be the largest economy in the world by 2030 if it can avoid a catastophic event in its financial markets. The recent move by the central bank to cheapen the currency has convinced traders that the Chinese economy will strengthen, emerging countries will avoid a crisis, and global growth will continue. However, I think China will need more than a cheaper currency to cure its leveraged financial balance sheets, because the quantity of potentially bad loans is simply too large. The central bank of China knows that it cannot bail out every company, and for the first time we are seeing bankruptcies of companies. We will steer clear of the China story in our investments and will remain keenly aware of the potential ramifications of any China crisis.

Japan: No Free Lunch

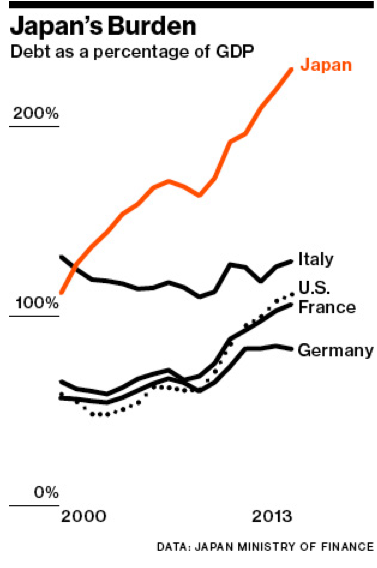

In September 2012 Abenomics was born, with the purpose of increasing Japanese inflation to 2% and devaluing the yen versus all other currencies. Today Japan faces a mountain of debt, with a debt-to-GDP ratio that reached 224% at the end of 2013.

With Japan’s birth rate below replacement level and a cultural resistance to immigration, it is easy to see that domestic demand for goods and services is going to decline in the coming years. Japan’s only hope for economic growth is to become a larger export economy. Rather than relying on innovation as an economic driver, the finance minister is going to compete on price. By lowering the yen, he is trying to make the price of a Lexus equal that of a Kia in US dollars. The huge amount of money creation in Japan is much larger than that in either the US or Europe. The intent is to fuel the economy with cheap yen, increased exports, and an appreciating stock market. In my opinion the party ended when Abe and Company increased the sales tax from 5% to 8%, effective April 1. The sales tax effectively kills the positive effects of QE in Japan. The thrill is gone, the pain begins, and I predict Japan is destined to repeat the same policies they enacted in 1997-98. A recovery had begun in 1997, and the government decided to raise taxes. Immediately their economy fell back into recession and remains mired in the bog of zero growth.

The effect of Japan’s massive action to devalue the yen evokes a response from other countries of “Oh no you don’t!” Even Germany’s Bundesbank stated on March 13 that it supports the European Central Bank’s ability to buy loans and other assets to support the Eurozone economy, marking a radical shift from its prior hard-nosed conservative monetary policy. Germany is an export-driven economy, and the Germans are not about to let the price of a Mercedes become 25% to 50% more expensive than a Lexus in terms of US dollars.

To understand the effects of a currency war, one should look to the 1930s race to the bottom but replace the United Kingdom of 1931 with the Japan of 2013. On September 19, 1931, the UK abandoned the gold standard and started printing money. By December the UK pound sterling had fallen 30% versus the US dollar and set off a chain reaction of “me too” from France, Germany, Sweden, and Norway. There is obviously no gold standard to abandon today, and I realize things will be different in this war. However, all the central bankers are currently staring at each other across the table, hoping no one is going to blink and start implementing trade protection, capital controls, and specific import taxes in retaliation for money printing and currency devaluation. Sooner or later someone will blink. Each new round of government stimulus that results in less and less GDP growth eventually creates an “every central banker for himself” mentality.

Short-term, Japan wins. Intermediate-term, the US wins as investors look for stability in what is called “the flight to safety” – and the dollar still has the advantage of being the world’s reserve currency. Long-term it will be China because of their central bank’s control of the yuan and their record purchases of gold reserves.

All Hail The Fed! All Hail The Fed!

“Thus far, inflation has yet to raise its ugly head, and inflation expectations as measured by consumer surveys and market-traded instruments have remained stolid. However, with each passing day, constantly adding massive amounts to the monetary base will inevitably present a significant challenge to the FOMC, which must ultimately manage this high-power money so that it does not become fuel for sustained inflation above the committee’s 2 percent target once it is activated and flows into the economy.

“Thus, I was more than supportive of the collective decision of the FOMC to begin cutting back on our rate of accumulation of assets beginning in December. Over the course of our recent meetings, we have cut back from accumulating $85 billion per month in Treasuries and MBS to a present rate of $55 billion per month. This is still somewhat promiscuous. Even with the taper, the recent decline of mortgage supply has driven our absorption of the MBS market to 85 percent of fixed-rate MBS issuance. The fall in net MBS supply is outpacing the taper.

“At the current reduction in the run rate of accumulation, the exercise known as QE3 will terminate in October (when I project we will hold more than 40 percent of the MBS market and almost a fourth of outstanding Treasuries). We will then be back to managing monetary policy through the more traditional tool of the overnight lending rate that anchors the yield curve.” Richard Fisher, April 4, 2014

The investment world devotes tons of money and human resources to researching sales, GDP growth, corporate earnings, inflation, interest rates, commodity prices, etc., to ultimately decide whether we are in a bull or bear market. However, since March of 2009, there has been only one positively correlated predictor for the direction of stock prices, and that’s whether the Federal Reserve is easing or tightening. Simply look at the chart on the next page.

Will the Fed continue to taper if the market tanks? I predict the puke point for the markets will be when the taper lowers the monthly amount of asset purchases to the $20 billion mark. The Fed is currently purchasing assets and creating money at a rate of $55 billion per month. At the $20 billion mark tapering gets real; and as Dr. Fisher indicates, he anticipates QE3 to end sometime this fall. But will QE programs and Federal Reserve intervention ever truly end?

The markets have become addicted to their investment cocaine, and once the supply is cut off, then cold turkey withdrawal ensues. In my opinion, when the pain becomes too great and the powers that be start catching heat, then Dr. Yellen and Company will see their tapering plans torn up like a Walmart tent in a tornado. For now, they are still printing at a $55 billion-a-month clip, and with the release of last month’s meeting notes this week, it appears we still have a very dovish FOMC.

From an investment perspective, we will monitor the earnings and outlook of those companies we own. We will continue to run diversified portfolios that will always lag when stocks go parabolic, as they did in 2013. We have our eye on the euro, the yen, Ukraine, and other factors that could contribute to a crisis that the sell side and CNBC do not see coming. But most importantly, we will keep our focus on the Federal Reserve and the reactions of the markets to stated policy changes.

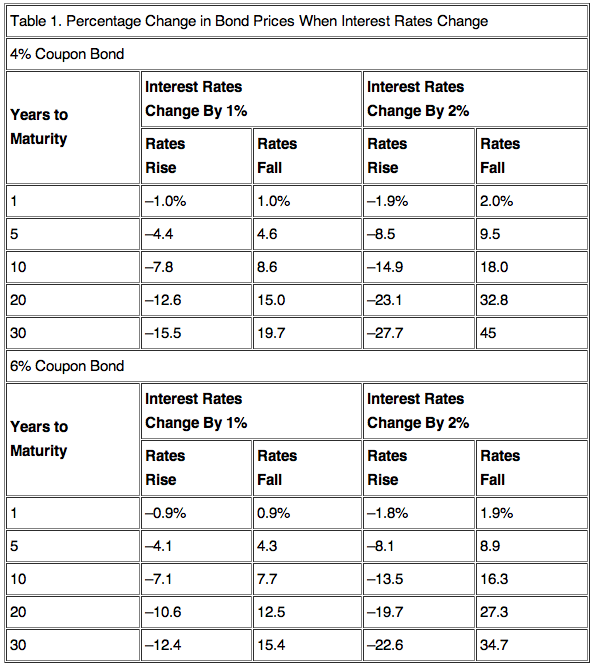

The Fed’s zero interest rate policy and suppression of interest rates causes investors to take risks they ordinarily wouldn’t take – be sure to understand your risk exposures. For example, note the 10-year and 30-year risk/reward of buying Treasury bonds:

Bonds appear to us to be today’s bubble investment. But there are other treacherous investments out there – good luck.

Your thawed-out, losing-weight portfolio manager, Cliff

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk; and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Excelsia, Inc.), or any non-investment-related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Excelsia, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Excelsia, Inc. is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Excelsia, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

© Excelsia Investment Advisors