STOCKS GAIN ON EARNINGS, FED

Stock markets rebounded last week from the prior week’s losses with the biggest gain of the year. As measured by the S&P 500, it was also the largest weekly gain since July 2013, despite being a holiday-shortened period. Gains were distributed through the first three days of the week, with Thursday coming in a bit quieter. For the week, the S&P gained 2.7% while the Dow Jones Industrial Average climbed 2.4%.

A few factors were at work last week, but corporate earnings were arguably the biggest headline driver of stock market performance. Citigroup got things off to a good start Monday, followed by strong results from Coca-Cola and Johnson & Johnson. And despite negative blips from Google and Bank of America, other blue chips like Yahoo! and Intel surprised to the upside. While on the aggregate the early results suggest a somewhat softer start to this earnings season, positive surprises from several index stalwarts appeared to boost investor confidence last week.

Janet Yellen also ingratiated herself with market participants by reaffirming the Fed’s commitment to keeping interest rate low as long as inflation remained contained and the job market was troubled – a turnaround, which she noted, would likely not occur for at least two years. In the speech before the Economic Club of New York, Yellen appeared to backtrack from the less dovish comments she made at her first FOMC meeting announcement last month.

Economic data also contributed to the string of equity market gains, both at home and abroad.

On Monday, retail sales posted a very robust 1.1% monthly increase in March, coming in slightly ahead of expectations. Even better, however, was an upward revision of February’s initial estimate of 0.3% to 0.7%.

Investors were particularly pleased with the core measure of retail sales, which excludes automobile and gasoline sales. That measure increased 1.0%, doubling the expected 0.5% gain. Improvement was observed across the majority of the measure’s component sectors, including housing related industries that may be rebounding from harsh winter months earlier in the year.

Industrial production also came in above expectations in March, albeit partly fueled by the utilities sector. The headline reading increased 0.7% in March, above the 0.4% consensus, while the prior month was also revised significantly higher. All three components of the indicator were positive, led by mining’s 1.5% increase and utilities’ surprising 1.0% rebound. Manufacturing growth was still solid, however, at 0.5% for the month.

Housing starts were the primary disappointment for the week, increasing nearly 3% but still coming in below expectations. Below the surface, however, the report was better than at first glance: single family housing starts grew at a fairly robust 6.0% pace. A decline in the more volatile multi-family housing component masked this otherwise positive development.

Outside of the US, the major economic figure for the week was China’s first quarter GDP estimate of 7.4%. While coming in at the slowest rate since Q2 2012, the composition of growth suggests officials are gaining ground in their attempts to transition the economy away from a capital investment based to a consumer driven one. According to Forbes, the consumption component of GDP comprised 76.7% of growth in the first quarter – the second highest share since the data series began in 2009. On the other hand, that increase was driven less by actual growth in consumption than it was in a sharp decline in property construction. Despite these mixed signals, market participants largely took the figure’s surprise beat as a positive.

TAXES ARE THE PITS, BUT NOT FOR EVERYONE IT SEEMS

A number of Americans breathed a joyful sigh of relief last week after closing the books on their 2013 income taxes. The annual rite of passage rarely elicits excitement when addressed in conversation, and this year was unlikely to be any different. But, the latest tax data suggests the economy is gaining speed, news bound to make even the most hardened filers crack a smile.

It is inevitable that around this time of year, opinion polls ramp up tasking any number of people how they truly feel about tax season. The commonly held assumption is that everyone would view taxes as tedious and downright awful, but data suggests that is not entirely accurate.

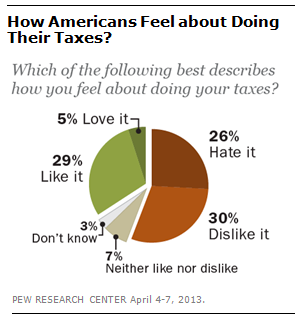

In fact, a recent poll from Pew Research Center found that 34% of Americans liked or loved doing their tax returns, likely due to the sense of accomplishment accompanying such a daunting task. Astute readers will notice that still leaves 56% on the other end of the spectrum as hating or disliking the task.

Source: Pew Research Center

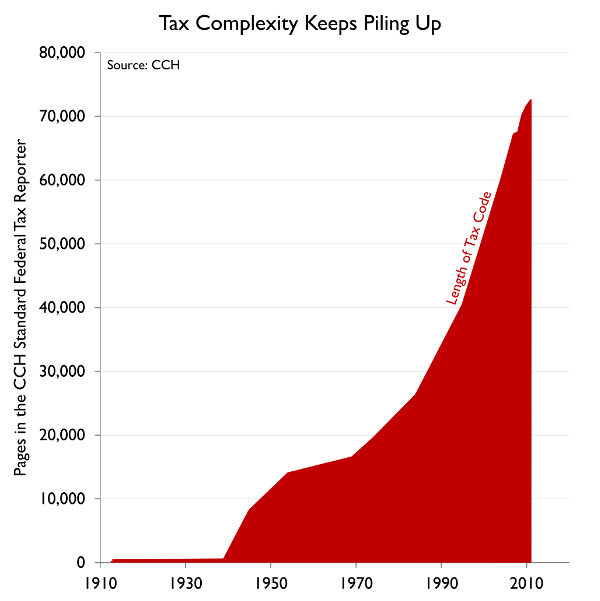

A major source of the negative attitude centers on the overall complexity of the tax code. According to the Tax Foundation, the tax code now reads in excess of 73,000 pages, up from 40,500 in 1995.

Source: Tax Foundation

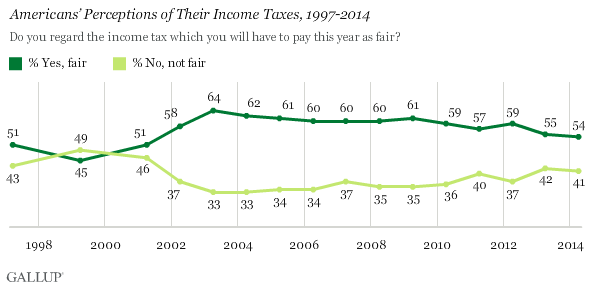

Despite objections to the process itself, the majority of Americans actually find their share of the tax bill to be fair. According to Gallup, 54% believe their income taxes are fair and 41% believe it is unfair. Those numbers have converged in recent years, after the gap reached as high as 64% indicating it was fair and only 33% believing their income tax bill was unfair.

Source: Gallup

Opinions are likely to continue converging because of tax changes during the fiscal cliff and the Affordable Care Act. The Hill reports that taxpayers saw an average 1.8% tax increase due to the fiscal cliff agreement, which continues to be a contentious political issue.

Over the shorter term, there are signs that economic improvement is taking hold. In the week leading up to April 15, the IRS reported that it received more than 112 million tax returns, roughly equal to the same period in 2013. Another 12 million filers already requested an extension. As tax rates have increased, government coffers are beginning to run flush. In March alone, the Treasury Department collected $216 billion in taxes, a 16% increase from last year.

While this has been good news for the government, some worry about its broader impact on the economy. Mark Zandi of Moody’s Analytics estimates that the greater share of the burden placed on high earners dampened growth by 0.2% in 2013. He worries the expiration of the payroll tax was an even greater headwind.

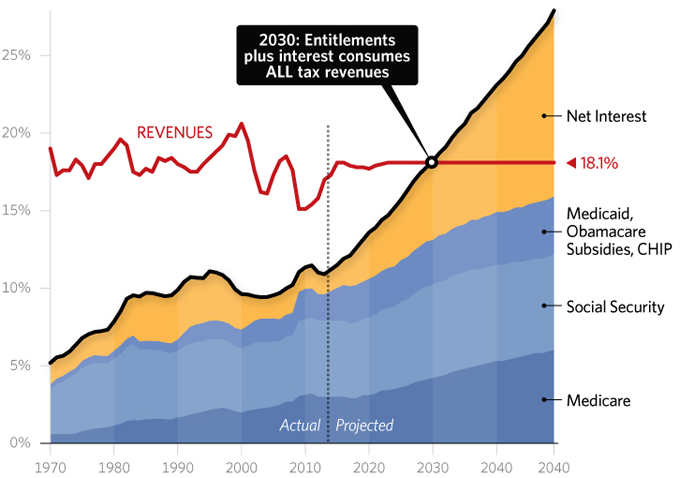

Moving forward, growing tax collections will make government officials feel good, but it could be transitory. Last year, entitlements such as Medicare/Medicaid and social security represented 49% of federal spending. By 2030, it is estimated that entitlements plus interest on the debt will consume 100% of yearly tax revenue, up from 66% in 2013.

Source: Heritage Foundation, CBO

Tax season elicits groans from many a weary filer, and for good reason. The growing tax burden is not expected to ease at any point in the near future, so the best recommendation for filers may be to grin and bear it. In the decades ahead, the situation will only become more complicated by growing federal expenditures, and with it, we should all expect a further expansion of the tax code.

THE WEEK AHEAD

Bouts of economic data coming out this week include the leading economic indicators index, the home price index, existing and new home sales, durable goods orders, and consumer confidence.

Earnings season continues with notable releases expected from Halliburton, Comcast, and Microsoft.

A number of central banks are slated to meet this week. These include Thailand, Turkey, New Zealand, Egypt, and Russia.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

(c) Fortigent