In our previous commentary “Gold and the US dollar – a love hate relationship” we used a normalized time series of the price of gold expressed in US dollars and an index representative of the value of the US dollar on currency markets to show the inherent relationship between the price of gold and the financing currency. As the financing currency strengthens on currency markets, one would expect the price of gold expressed in that currency to fall. We used the gold price in dollar terms as an example. As would be expected when the dollar falls, the price of gold in dollar terms would tend to rise. This result should not be surprising- when a currency is weak, an asset priced in that currency should increase in value, relative to that currency.

In this week’s commentary, we explore this relationship further focusing on historical events where there was a flight to quality, evidenced by a surge in demand for high quality US dollar assets (typically US government treasury bills). These will serve to highlight one of the potential risks of owning gold priced in dollars as a defensive asset. While gold priced in dollars does indeed show characteristics as a safe haven asset, financing gold purchases using only US dollars can, under certain market conditions, detract from gold’s performance during these stress periods. The reason is self-evident and related to our initial discussion about the relationship between gold and the financing currency used.

During periods of stress, the dollar has historically strengthened in value on currency markets as investors sold non-dollar assets for dollar-assets to hold as a defensive move against market declines. In fact in recent history, absent a viable alternative, the US dollar has been the defensive currency of choice and typically strengthened in value versus other currencies including gold as investors bid up its value in their search for financial safety. This arguably remains the case today for a number of reasons in particular i) the strong regulatory regime in the US, (ii) high liquidity and (iii) the size and diversity of US financial markets unrivalled anywhere else in the world. And following the logic of our initial discussion as the dollar strengthens, the price of assets financed in dollars, including gold, will tend to fall in value relative to the dollar.

An investor that buys gold financed in US dollars is expressing a strong directional view on both gold and the dollar – in market speak they are long gold, short USD. And it is this explicit short position on the dollar that creates the potential vulnerability for gold during periods of high market stress, as the dollar strengthens. As we have discussed in previous commentaries a viable strategy for investors to reduce dollar exposure is to diversify the financing currency used to make gold purchases across two or more currencies i.e. follow a “diversified gold” strategy. In effect this would reduce exposure to the dollar and thereby reduce the risks to holding gold from a surge in the value of the dollar.

We caution that history does not always repeat and the perceived defensive premium of the dollar will vary over time but we illustrate the potential benefits of this approach below by comparing the relative performance of gold priced in dollars versus gold priced with an equally weighted basket of dollars, euro, yen and pounds, over four recent periods of market stress. In each case the outperformance of the diversified gold strategy was driven by its smaller, short dollar weighting and hence it’s reduced exposure to a strengthening dollar. Ultimately for investors that do not have a strong view on the dollar we believe that such a diversified gold strategy represents an efficient approach to gold investing that may also offer the benefit to investors of lower drawdowns during periods of high risk aversion.

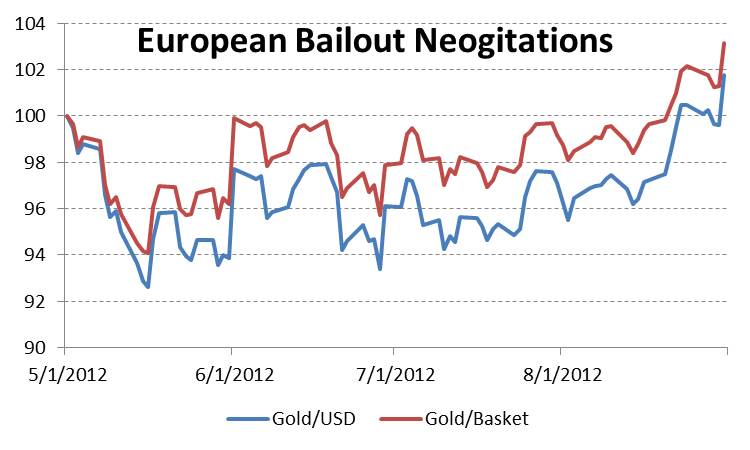

5/1/2012-8/31/2012

Soaring bond yields in the European periphery to record highs underscored wide spread pessimism amongst investors over the prospects for the survival of the European Union. The period saw steep falls in the S&P 500 as well as a broad strengthening in the dollar versus most currencies especially against the euro.

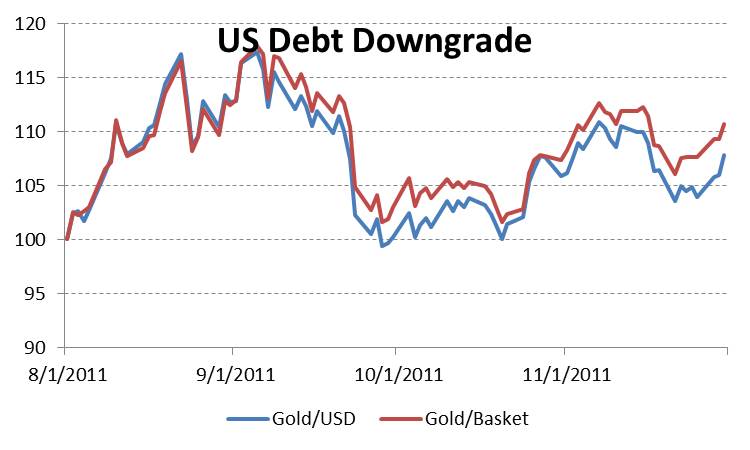

8/1/2011-11/30/2011

Continued stalemate in Congress over the debt ceiling negotiations and the ensuing S&P downgrade of US debt both combined to unnerve investors resulting in a so-called “risk-off” environment, a sharp decline in the S&P 500 and a sharply rising dollar. The European Union was the focus of concern as the debt crisis intensified amid sharp differences from European governments over the appropriate policy response.

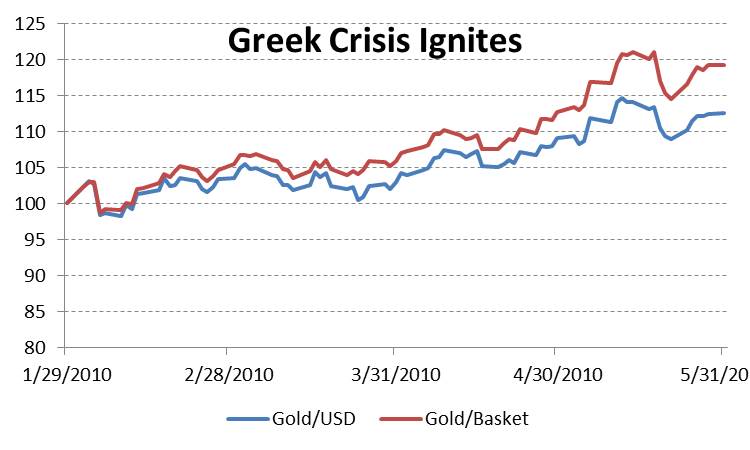

1/29/2010-5/31/2010

The revelation of the true extent of the Greek government’s indebtedness caused a large flight of capital out of the European Union in the US as investors reevaluated the risks of a breakdown in the common currency.

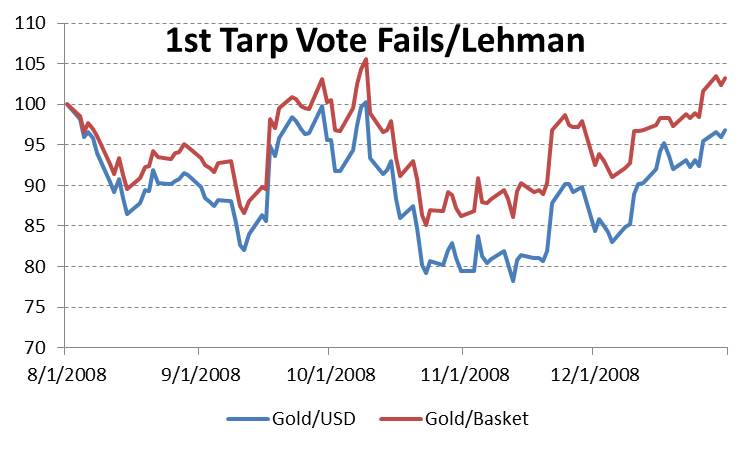

8/1/2008- 12/31/2008

The failure of the first Troubled Asset Relief Program (TARP) vote in Congress and the Lehman bankruptcy in September 2008 triggered a sharp 40% decline in the S&P and a dramatic flight to quality as investors sought the safety of US government treasury bills.

Source: Bloomberg LP; Treesdale Partners calculations; Gold Basket is gold financed with an equally weighted basket of USD, Japanese yen, European euro and British pound – daily rebalanced. Past performance is not indicative of future performance

(c) AdvisorShares