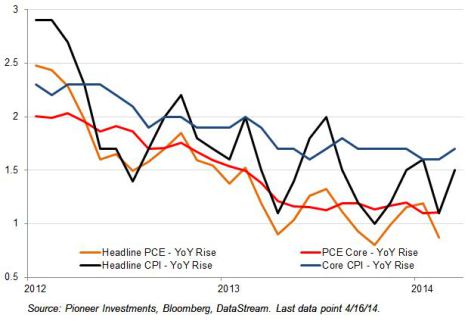

For more than a year the Federal Reserve Board has cited inflation below its targeted 2% level as one justification for maintaining its extraordinarily accommodative monetary stance. As of February, the core inflation rate was 1.1%, based on the Personal Consumption Expenditure (PCE) inflation series, the Fed’s preferred measure of inflation. But there is good reason to question whether the 2% target justifies current policy.

Fed Fixation: Inflation’s Downward Trend (%)

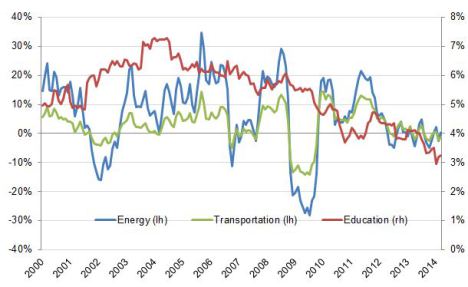

What’s Driving Inflation Lower?

Today’s low inflation is taking place in an economic environment that is far different from the conditions that triggered falling prices during the Great Recession. Those declines occurred as a result of severe debt contraction, a downward spiral in asset values across nearly the entire economy and a global banking crisis. The Fed’s actions to offset these damaging conditions were exceptionally timely and successful, and conditions are now the exact opposite. Values across a broad array of asset classes have seen significant appreciation, and many key economic sectors are exhibiting healthy competition and growth.

Good vs. Bad Disinflation

There is a difference between “good disinflation” and “bad disinflation.” Looking deeper at the inflation data over the past several years reveals that disinflation is the result of a variety of factors, including technological progress, new efficiencies in business models and strengthening competition. Let’s look at the commodity sector, one of the weakest areas within the inflation reports. Technology has had a tremendous impact on energy costs over the past few years. With horizontal drilling techniques and fracking, vast amounts of newly recovered U.S. oil and gas have been brought into production. We now produce so much oil & gas that we are considering changing laws so it can be exported once again. Energy CPI grew 0.4% year-over-year, and was an even lower -1.6% a year ago.

Sources of Disinflation: Energy, Transportation and Education

Source: Pioneer Investments, Bloomberg, Datastream as of 4/16/14.

Does This Course of Action Really Make Sense?

This begs the question: Don’t lower energy prices put more money in the hands of businesses and consumers? States involved in the fracking boom, such as North Dakota and Texas, have seen much faster rates of employment growth in good paying jobs. Of course, this has created a weakening of the coal sector with some bankruptcies and job reductions, but this has been overwhelmed by the growth overall. In addition, there have been many anecdotal reports of the manufacturing renaissance in the U.S., in part due to the significant energy cost advantage the U.S. now wields. Does it make sense that the Fed believes monetary policy needs to be so accommodative as to offset these clear macroeconomic benefits?

Consider the Following:

Education: After averaging nearly 6% annual price growth from 2000-2010, prices in this sector decelerated sharply to just 3.2% growth as of March 2014. Perhaps the lower price increases are attributable to weakening demographics, new ways of delivering education via online programs, or maybe the advent of for-profit education companies are all having a positive impact on pricing. Have not consumers, policy makers et al. been bemoaning the high price of education for years? A more price competitive model will allow more people to have greater options and opportunities to get the training they need. This new-found competition may result in greater numbers of mergers, or even bankruptcies in the sector, but isn’t this rationalization serving the greater good? Why the Fed feels compelled to create enough inflation to offset this positive circumstance is not inherently obvious.

Transportation: Prices in this sector fell 1.2% in March year-over year. Airfares have been particularly weak, down 4.1%. Everyone who travels knows that load factors have been generally high, with crowded planes - and the airline industry is experiencing decent financial trends now that the restructuring of several years ago has taken place. Transportation deflation doesn’t seem to be negatively affecting the economy, as access to flying continues to grow and airline credit quality is improving.

New auto prices have been another source of price weakness, declining 0.5% as of March. With auto sales reaching 16.3 million units on an annualized basis in March, is there really a demand problem? In 2009, annualized auto sales were less than 10 million units and factories were closing. In 2014, no U.S. automaker is near bankruptcy. In fact, all three U.S auto manufacturers have had credit upgrades over this period. If automakers are producing too many cars now, why should monetary policy be geared toward protecting automakers when auto demand and credit conditions are relatively normal?

Medical Care, Recreation and Apparel: These sectors have also seen very low or receding levels of inflation over the past year. All these sectors have important elements in common. They are all industries subject to either technological innovation that is having truly positive effects on greater supply and lower costs (the energy sector, computers, retail, etc.), or previously bloated, unreformed industries where new competitors with new business models (education, health care, airlines) are driving the need for change and new approaches.

Time for the Fed to Correct Course

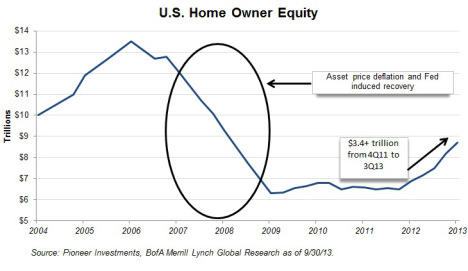

I don’t understand the Fed’s stance on these lower prices. Aren’t technological progress, new efficiencies in business models and processes drivers of economic progress? The truly worrisome deflation we should be concerned about is driven by asset price declines. When home values fell during the recent recession due to a confluence of unaffordable prices, poor underwriting, increased jobless rates and high leverage, they had a systematically disruptive impact on consumers, the financial system and the overall economy. When asset value and resulting debt value declines broadened beyond the residential housing market to most other sectors of the economy, the result was one of the worst recessions since the Great Depression.

Bad Disinflation: Falling Home Values Not an Issue This Time

We are clearly not in the debt contraction/asset price downward spiral that we faced during the recent recession. The reality is quite the opposite. I, for one, hope the Fed begins to distinguish the “good” disinflation from the “bad”, as I sense the markets have begun to enjoy the easy money party for a bit too long.