“I am wiser than this man, for neither of us appears to know anything great and good; but he fancies he knows something, although he knows nothing; whereas I, as I do not know anything, so I do not fancy I do. In this trifling particular, then, I appear to be wiser than he, because I do not fancy I know what I do not know.”

Socrates (c. 470 BC – 399 BC)

Greek philosopher

Indicted for “impiety” in offending the Olympian gods, Socrates supposedly offered the above in a speech which came to be known as “The Apology” after his one-time student, Plato, wrote it in his dialogues. Socrates wasn’t really apologizing, at least not the way we today think about such things. To the ancient Greeks, to apologize (derived from the Greek word apologia) meant to offer a defense, not to make excuses for bad behavior. In investing, certain things are viewed as worth paying a lot for, if you “know” you’re going to get them. Akin to Socrates, we speculate that it may be wiser to admit that you do not know the future and therefore are unwilling to pay for these positive outcomes, than to falsely believe you can know the future with certainty and are justified in paying a high price.

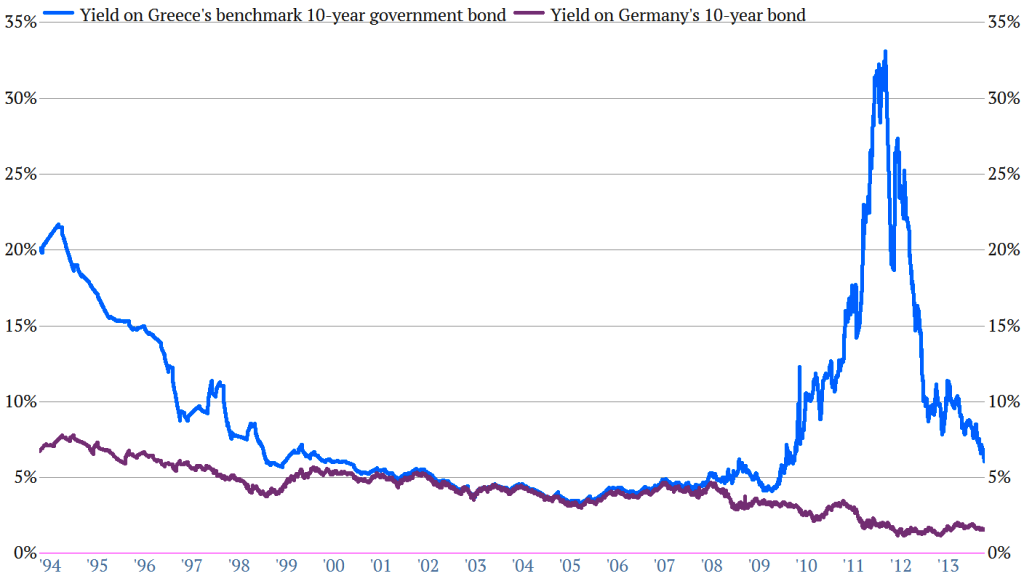

Unlike Socrates, who was ultimately executed when his “apology” for not honoring the gods was rejected, it appears modern Greeks need not apologize at all...for their past profligacy that is. Three years after the world woke up and recoiled in shock at Greece’s impossible debt burden, the world, or at least bond investors, appear to have fallen back into a peaceful slumber. When investors first awoke to Greece’s mounting fiscal difficulties, they pushed 10-year Greek bond yields above 30% and the Euro to the brink of collapse. Fast forward to today when bond investors ridiculously lend to the Greek government at 5% via newly issued bonds...and these somnolent investors wanted ten times more bonds than were originally available!

Keep in mind, this is a country that has been in default roughly half the time since it became independent from the Ottoman Empire. Memories are short and trust runs high. Greek public debt towers at an eye-popping 178% of GDP, even after private creditors suffered a more than 50% hair-cut (which is a nice way of saying default). Let’s compare this to Argentina, where three-year government bonds were recently yielding 13%. Agreed they also have a troubled government, but their debt to GDP at 43% is much lower than that of Greece (again 178%). We wonder whether Greece was perhaps able to get away with the recent issuance at low rates because these new bonds come due in five years, front-running all subsequent maturities. Perhaps this is why some investors feel they “know” that Greece is not a big credit risk. Maybe the reason for the enthusiasm is the European Central Bank’s recent indications that they may experiment with literally negative interest rates. It would indeed be interesting to see whether this unconventional move encourages banks to make more loans, as intended, or rather if it encourages banks to withdraw their money from the ECB’s electronic ledger and instead physically store it in paper form in their bank vaults. In central banking circles there has also been chatter about the ECB doing QE and buying long-dated assets. Amusingly, QE is to stand for “qualitative easing” in this case where previously it stood for “quantitative easing”...perhaps this is to increase the appeal of the program to people who don’t like math.

Not to be outdone, another impossibly indebted issuer, Puerto Rico, got in on the act by issuing bonds in March. Demand exceeded supply and the offering was five times oversubscribed. Again, perhaps it’s not so much the creditworthiness of the issuer that makes the bonds attractive but rather that they are senior to other Puerto Rican bonds. The issuance also produced one of our favorite headlines from the quarter: “Puerto Rico Wants to Incur More Debt to Regain Financial Footing” . Does this remind anyone of Greek debt problems being “solved” by receiving more loans from the IMF and Europe? Well, perhaps they weren’t solved but instead just papered over for a while...pun mostly intended.

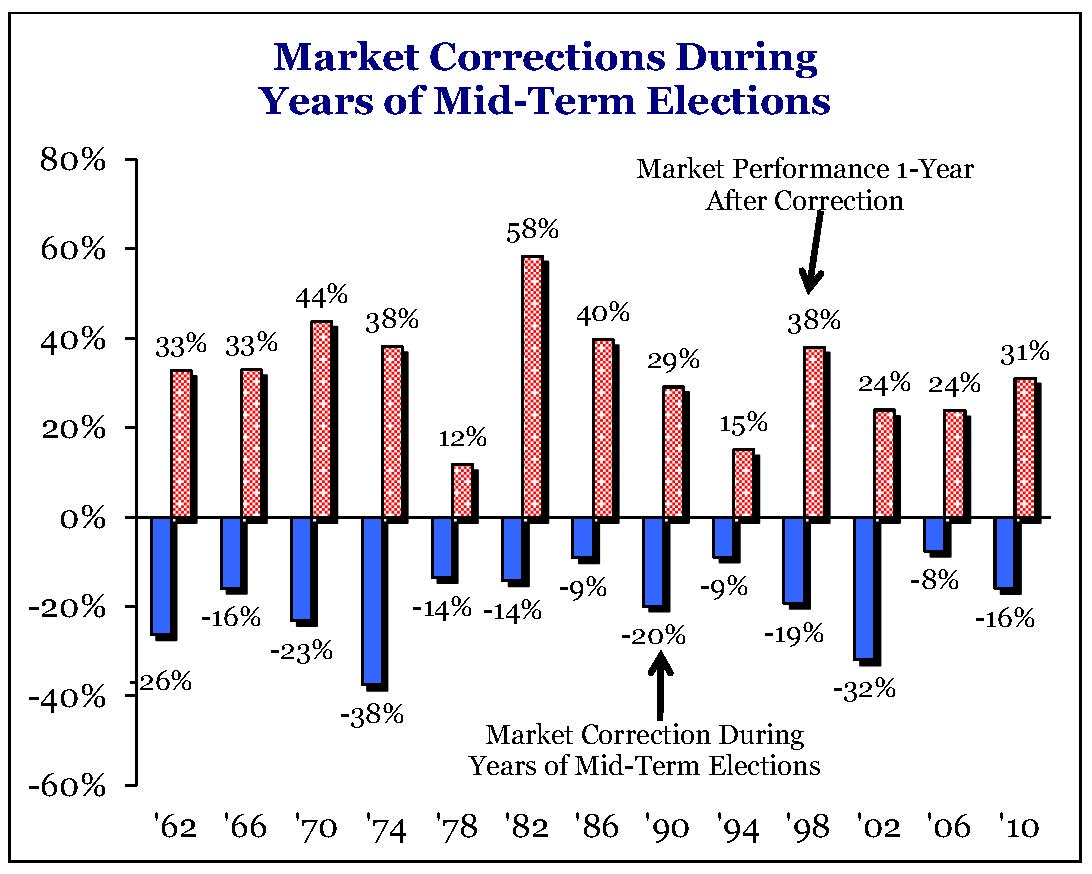

Turning to U.S. equities, the first quarter was a bit of a roller coaster. The S&P 500 Index dropped roughly six percent and then recovered, ending basically flat (actually Q1 finished with a small gain, and for what it’s worth, in every mid-term election year since 1950 in which the S&P 500’s Q1 was positive, the full calendar year return was as well). After new all-time highs in early April, fresh declines ensued and by mid-month the average stock in the S&P 1500 (which includes large, mid and small sized companies) was off over 14% from its 52-week high. As the above chart illustrates, it is common to experience tough market conditions leading into mid-term elections. Fortunately, such conditions have consistently given way to sizable one-year recoveries (albeit with hindsight of correction end-point), as the red bars evidence.

Last year’s stock market was an aberration, both in terms of the high returns and low volatility. In contrast, this year winning stocks have been few and far between as the top ten performers in the S&P 500 Index produced 170% of the total index gains through Q1 (meaning the other 490 stocks, 98% of the index, underperformed as a group). This situation, when a small number of high flyers power the index, has a perplexing result: the “average” stock underperforms the average.

Recently a member of the Knightsbridge research team had the pleasure of sitting at a poker table with a hedge fund analyst. Said analyst quoted his boss as recently saying, “Lever up baby, we’re headed to the moon!” Perhaps it should be no surprise then that hedge funds produced their worst Q1 return since the 2008 financial crisis. Many of these funds had crowded into momentum names that had experienced great advances recently (internet and biotech stocks, etc.) but subsequently proceeded to get crushed in late March and early April. The NASDAQ biotechnology group plunged a quick 20% from its peak and NASDAQ internet stocks dropped 11.9% from their peak. We would say these declines were deserved given (still) nosebleed valuations.

The chart to the below shows just how high the valuation of certain favored groups was, and still is, as measured by stock price compared to revenue. Note the upward trend...until recent events, that is. In a world of widespread slow growth, investors are paying huge premiums for the few issues that they believe offer certain growth. Empirical Research Partners screened for the 75 companies possessing “secular growth” potential, as measured by expected revenue growth and stability as well as quality of earnings. These 75 stocks trade at about nine times revenue (blue line on the chart). Growth is certainly a good thing, but at what price? Five or ten times current revenue for said potential growth is in our mind way too steep a price to pay for an only-promised future.

The IPO market is a great barometer of investment enthusiasm. After all, hope is a necessary ingredient for trusting in something not yet in existence...like Twitter’s profits. Filings to go public have been coming fast and furious this year, more so than at any point since the year 2000 internet bubble. During the last six months, three quarters of new issues lacked any profits, again the highest proportion since 2000, with most of this year’s numerous tech and biotech IPOs lacking profits. IPO buyers have been paying an extraordinary 14.5 times annual sales on average this year (for perspective, Knightsbridge holdings trade at an average 1.5 times sales, just less than the S&P 500 Index at 1.6). Given the recent plunge in high-flying “hope” stocks, some are beginning to wonder whether the doors to the IPO carnival are shutting. If this happens, we wonder if the decline in sentiment will extend to the entire stock market.

Another sign of the Tech Bubble II is the recent slate of acquisitions, capped of course by Facebook’s $19 billion dollar acquisition of WhatsApp. WhatsApp, an electronic messaging service (think text messages without the phone bill), is better than many tech companies in that it actually has revenues and profits. However, if one values it on current revenues or profits, one sees an absurd picture. Well Facebook wasn’t buying revenue or profits, they were buying...users! So Facebook’s apologists have been explaining the WhatsApp’s valuation on users. Sounds great...except doesn’t this remind everyone of valuation on “eyeballs” seen in the first Tech Bubble ? I suspect even wunderkind Mark Zuckerberg “knows” the value of a WhatsApp user about as well as the old-time Time Warner board “knew” the value of an AOL user before the merger (we might add that AOL at the time had the dominant messaging application). Some are quick to point out that Facebook paid for this merger in stock, and therefore perhaps didn’t overpay because Facebook’s own stock might be overvalued. While this may be true, it certainly doesn’t help Facebook’s stockholders any, because either the company overpaid for WhatsApp, or if not, the original Facebook stock is heavily overvalued.

Astronomical mergers aside, the rush to go public is a warning sign and we are on alert given the length of the current bull market. Of the 23 bull markets (defined as a rise of more than 20% after a fall of equal magnitude) since 1928, the current bull market, which began in March of 2009, is the sixth longest, producing the fifth greatest total gain. The probabilities of market cycles, based on historical patterns, suggest a downturn could appear at any time and we endeavor to be prepared.

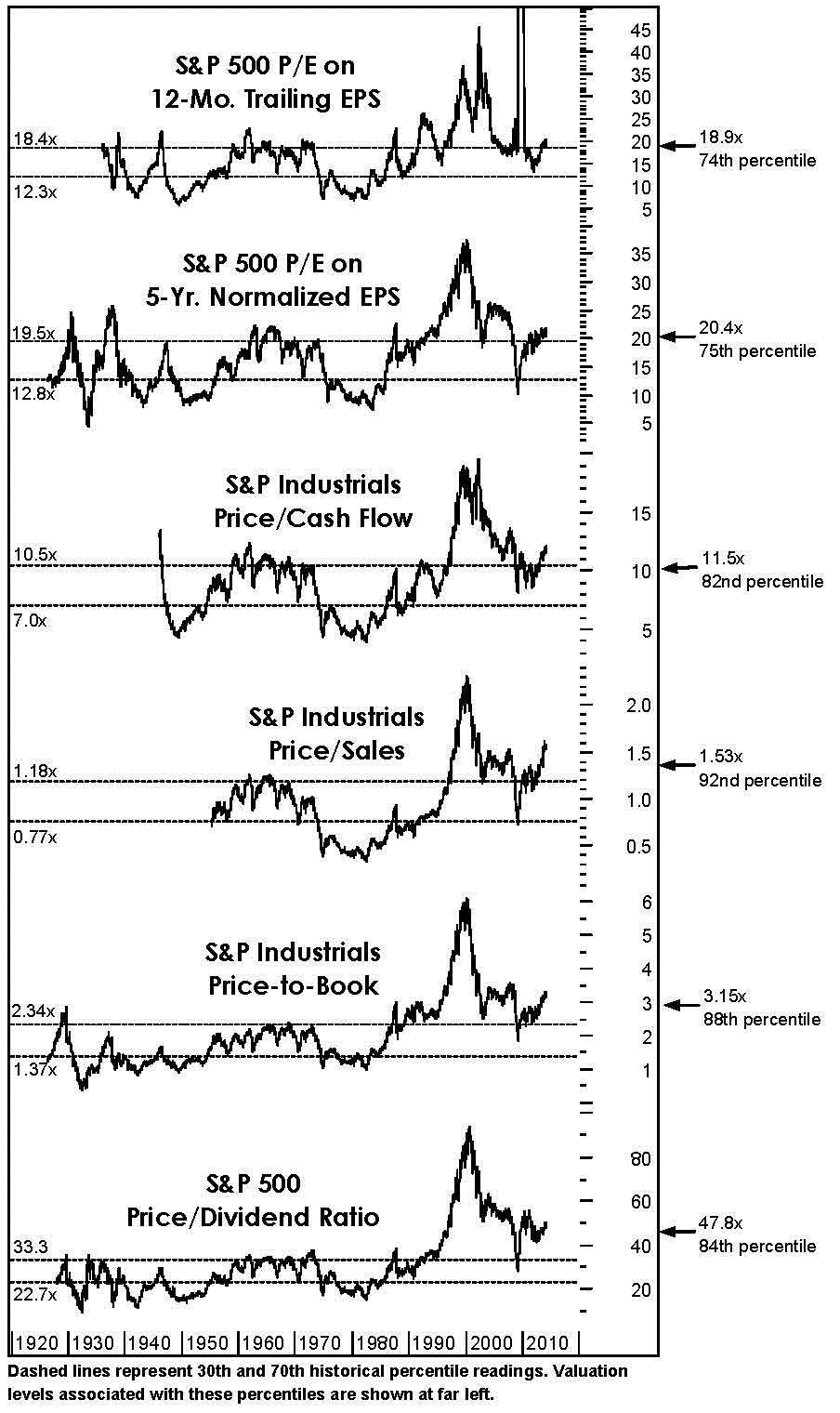

Equity valuation also warrants attention. As the chart at right illustrates, by a broad array of valuation measures stocks are trading at top-quartile most-expensive valuations. Given all this, we are keeping a close eye on the stock market. Our seatbelts are fastened, cash reserves in hand, for what we expect to be a more challenging, but potentially still rewarding, 2014.

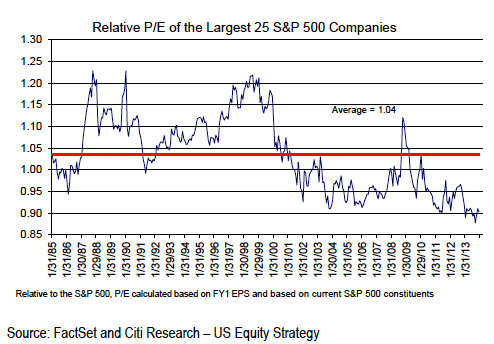

Fortunately there remain isolated pockets of value in this market and, by being opportunistic and willing to range broadly in the search for investments, we are set to take advantage. The largest U.S. companies offer good relative value (bottom left chart) as do emerging markets, which is why you see both types of stocks represented in your portfolio. Our most recent purchase, Turkcell (a major European telecommunications company and the only NYSE listed Turkish company, symbol TKC) represents exposure to a market trading at a steep discount to the S&P 500 Index. We expect Turkcell to deliver a large one-time special dividend during the next year or two following resolution of a shareholder dispute, as well as a return to regular dividend paying status. Both developments should be very favorable for valuation. We found this opportunity after observing massive outflows from emerging markets, including Turkey, early this year following a prolonged period of meaningful underperformance from which we expect to see a nice recovery. As the previous chart (prior page, bottom right) illustrates, emerging market (EM) equities have tended to sharply outperform developed markets (DM) following periods of larger relative fund outflows.

Also on the positive side, the “investment anomalies” in which we traffic, such as spin-off situations, are capable of delivering market-beating results in multiple types of environments. You now own shares of the recently spun-off Lands’ End and two other holdings, Chesapeake Energy and Exelis (itself a spin-off from our holding at the time, ITT), will likely execute spin-offs later this year. You own roughly 20 of our best ideas in which we see unique developments and potential for good returns, even if the overall market continues to deliver lackluster returns this year.

As Socrates so well understood, the future is always uncertain. We attempt to remain cognizant of this reality. What is more certain than yet-to-be-realized predictions, is that current earnings and values tend to extend into the future and many difficulties and troubles tend to fade with time. It is these principles which have guided us over our 20-year track record and will continue to guide us for the next 20 years as well. As always, we appreciate your continued support.

Very Truly Yours,

John G. Prichard, CFA

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

(c) Knightsbridge Asset Management