Does Negative GOFO Signal Higher Prices for Gold Financed in Currencies?

In recent weeks a number of gold commentators have once again highlighted the strong inverse relationship over the last year between the price of gold in dollar terms and the London Bullion Market Association Gold Forward Offered Rate "GOFO". Since the first week of July 2013 when the price of gold bounced decisively, the GOFO rate has fairly reliably predicted the future direction of the gold price. When GOFO has turned negative the gold price has tended to rise and when GOFO has turned positive, the gold price has tended to fall. This relationship can be seen clearly in the chart below - when the light blue line flips from positive (+1) to negative(-1) (right hand axis - red circles) this has generally signaled a turn higher in the gold price. And with GOFO moving decisively below zero in the first week of April, the expectation from many strategists is that the price of gold is likely to rise over the coming weeks, having fallen sharply from the 1379 high on March 17 to a low of 1283.50 on April 24.

![]()

![]()

![]()

![]()

![]()

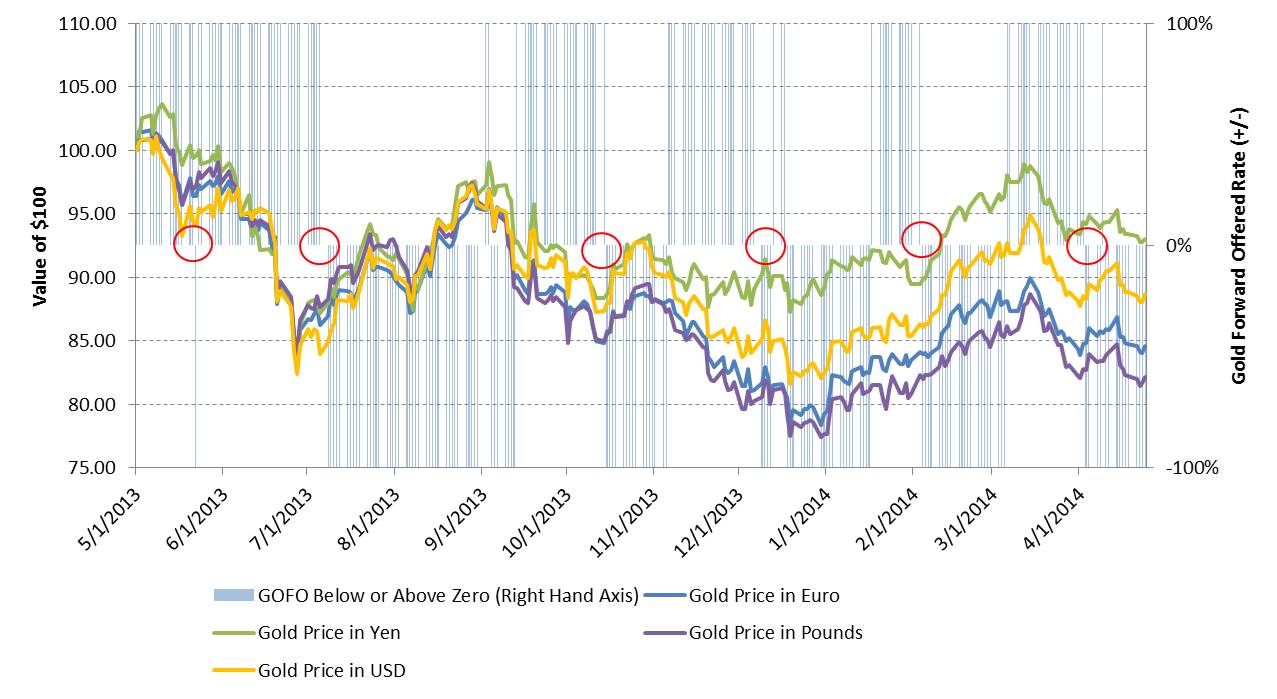

Source: Bloomberg LP; Treesdale Partners calculations. Past performance is not indicative of future performance

In this week's commentary while we give a short technical description of GOFO and discuss what may be driving this relationship, we also want to investigate whether this observed relationship between the gold price and GOFO also exists between GOFO and the price of gold expressed in foreign currency terms, in particular in euro, yen and pounds.

At its essence GOFO is a benchmark (published by the LBMA and quoted as an annualized interest rate) that reflects the cost of carry of gold - the cost to borrow physical gold for an agreed period of time versus depositing US dollar collateral - a positive GOFO indicating that a gold investor will incur a cost to swap gold for cash today and then receive the gold back and repay cash on an agreed future date. In an earlier commentary we discussed the following identity

GOLD COST OF CARRY = USD FUNDING INTEREST RATE + COST OF STORAGE - CONVENIENCE YIELD

Given that interest rates and cost of storage are generally ‘non-negative’, a negative cost of carry can only really occur when the convenience yield exceeds funding and storage costs – in practice when traders are willing to pay a premium to own physical gold today versus the right to own gold in the future (the convenience yield). Turning then to how cost of carry relates to GOFO:

GOFO = USD FUNDING INTEREST RATE – GOLD LEASE RATE

The gold lease rate (the interest rate on gold) is akin to the interest rate an investor would earn for cash and is primarily a function of the cost of storage and the unobservable convenience yield. Therefore, unsurprisingly, the gold cost of carry and GOFO are closely related concepts and would be expected to be closely track each other. A scenario that can occur and one which we believe largely explains the negative GOFO rates in recent months is where there is a rise in demand for physical gold related settling gold futures contracts and this is coupled with an environment where the supply of physical gold has dropped. Typically when this imbalance has arisen in the past the cost of carry/GOFO has occasionally become negative with an investor being able to earn to own gold.

A detailed examination of this relationship is beyond the scope of this discussion piece but we will suggest that certainly there is some evidence in recent months (for example negative GOFO has tended to be observed around COMEX gold delivery) to suggest that it has been this drop in supply in the physical market coupled with settlement demand in the futures market that has underpinned the gold price. And while it is certainly unclear as to whether this relationship will hold going forward, we nevertheless find it instructive to see if GOFO has shown a similar relationship with the price of gold when expressed in euro, yen and pounds.

We show in the chart below the price of gold expressed in each of dollar, euro, yen and pounds overlaid on the light blue bars indicating periods of positive or negative GOFO. Prices are normalized to show the change in value of $100 invested in each asset. Over the period May 2013 to April 2014 the gold price in euro and pounds has largely tracked the gold price in dollars. The same relationship between gold and GOFO is evident with a negative GOFO generally associated with a rising gold price and a positive GOFO associated with a falling gold price. The relative outperformance of gold in dollars versus gold in euro or in pounds reflects that the both the euro and pound strengthened versus the dollar by approximately 5% and 8% respectively over the period. Nevertheless even during the periods when gold in dollars outperformed on a relative basis all three prices generally exhibited the same relationship with GOFO. Similarly, gold in yen outperformed gold in dollar reflecting the yen weakening versus the dollar by approximately 5% and while showing less volatility overall compared to gold in euro or pound, the same directional relationship to GOFO was evident.

But bigger picture, a word of caution - despite gold in yen terms having had a consistently negative cost of carry (cost of carry + cost of currency funding) since May of last year its price has still fallen by over 7% - earning carry is no panacea for rising gold prices.

Source: Bloomberg LP; Treesdale Partners calculations. Past performance is not indicative of future performance

(c) AdvisorShares