The TCW Advantage: Analysis with Consumer Credit

5 years removed from the depths of the crisis and behind the tailwinds of an incredibly accommodative Federal Reserve, asset prices and of course Non Agency RMBS prices have improved dramatically. When double-digit loss adjusted yields were available most participants in the market did very well if they were able to simply overcome the fear of buying an asset class that was seemingly in freefall. At current prices and significantly lower loss adjusted yields today, however, the margin for error is far lower and many managers without the expertise, infrastructure and experience will underperform going forward. In our second segment of the TCW Advantage series, we discuss our access to consumer credit information. This information not only gives us additional insight into general borrower characteristics but we strongly believe that we are able to gather critical pieces of information to help us properly forecast default rates and prepayment rates. Most market participants simply do not have this type of data due to the high hurdles that exist to purchase and employ it properly. Simply having the data can be misleading if not properly analyzed. Our MBS team at TCW is dedicated to analyzing all the relevant pieces of information and we believe our ability to dive deeper into the borrower credit profiles gives us a distinct advantage versus our peers.

Understanding the borrower is key to forecasting voluntary prepayments and defaults. At TCW we’ve developed tools using updated consumer credit data to help us understand the current credit profile of the borrower. This updated credit profile gives us additional insight to more accurately predict voluntary prepayment rates and default rates. We will review six examples of consumer credit metrics that can lead to alpha generating insights.

Mortgage Inquiry

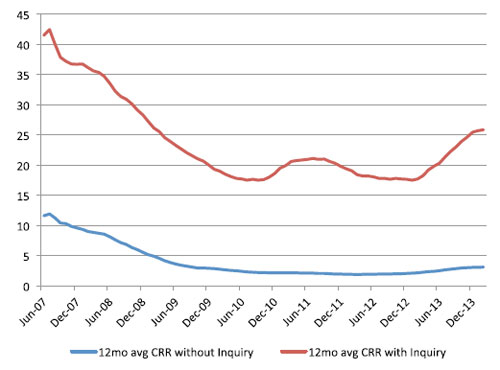

The mortgage origination process is fairly standardized. It typically initiates with the borrower contacting a lender and inquiring about mortgage terms. A lender can give an estimate based upon the information the borrower provides. However, in order to “lock in a rate” the lender must first verify the profile the borrower has presented and gather additional credit information. The lender contacts one or more of three consumer credit companies (Equifax, Transunion and Experian), presents the borrower’s social security number and pays a fee to obtain the information required. This event generates a note that the consumer credit company attaches to the borrower’s credit profile. We call it a “mortgage inquiry.” That note is passed on to TCW’s analytical database and attached to any non-agency residential mortgages that the borrower might have outstanding. As one might imagine, mortgage inquiries are strongly correlated with short-term voluntary prepayments. Figure 1 shows the voluntary prepayment rates of subprime mortgage borrowers that have had recent mortgage inquiries compared to the voluntary prepayment rates of subprime mortgage borrowers that have not had any recent mortgage inquiries.

Figure 1: Voluntary Prepayment Trends Among Subprime Borrowers With/Without Mortgage Inquiry

Sources: Equifax, Corelogic, TCW

TCW portfolio managers use our mortgage inquiry metric to identify pools that will have above average voluntary prepayments and thereby generate higher than anticipated cashflows for investors.

Number of Mortgages

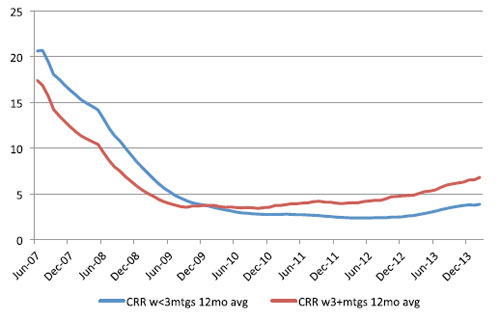

Our consumer credit data provider aggregates the total number of first mortgages a borrower has and reports the number to us for each borrower in the non-agency mortgage universe. Most borrowers have one first mortgage but there are many borrowers with more than one first mortgage. We asked, if borrowers with three or more mortgages prepay and default at different rates than borrowers with one or two mortgages. In some ways the answers surprised us. Figure 2 shows that if you were a subprime borrower with three or more mortgages trying to weather a tremendous drop in home prices then you prepay slower than those with fewer mortgages. However, since home prices began to find a bottom, the reverse is true. Subprime borrowers with three or more mortgages now prepay at a faster rate than borrowers with one or two mortgages.

Figure 2: Subprime Voluntary Prepayments Among Borrowers With/Without Three or More Mortgages

Sources: Equifax, Corelogic, TCW

Figure 3 shows that prime borrowers with three or more mortgages have consistently prepaid at a slower rate among both falling and rising home prices.

Figure 3: Prime Voluntary Prepayments Among Borrowers With/Without Three or More Mortgages

Sources: Equifax, Corelogic, TCW

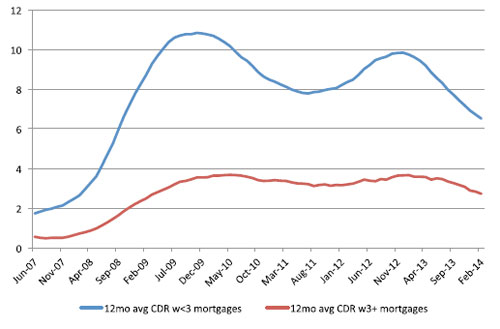

Subprime borrowers with three or more mortgages default at a lower rate than borrowers with one or two mortgages as seen in Figure 4. These borrowers likely benefited from rental income which helped them weather the loss of equity during the housing crisis.

Figure 4: Subprime Default Trends Comparing Borrowers With/Without Three or More Mortgages

Sources: Equifax, Corelogic, TCW

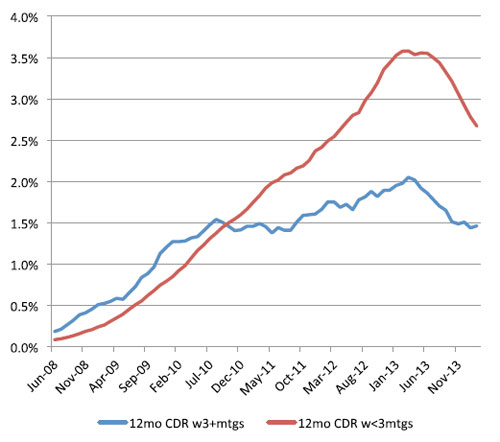

Figure 5 shows that prime borrowers with three or more mortgages are also stronger borrowers when it comes to defaults. However, during the most difficult part of the housing crisis, more mortgages meant higher default rates for prime borrowers.

Knowing how many mortgages a borrower has helps portfolio managers identify pools with stronger borrowers who are less likely to default thereby generating higher cashflows for investors.

Figure 5: Prime Default Trends Comparing Borrowers With/Without Three or More Mortgages

Sources: Equifax, Corelogic, TCW

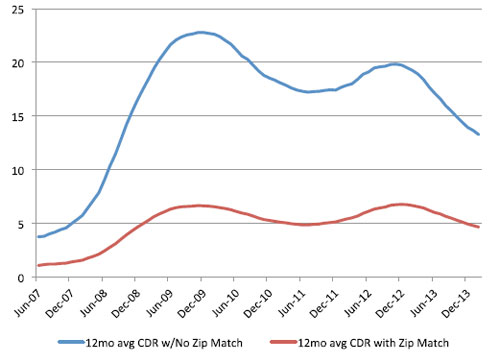

Owner Occupancy

Loans backed by second homes and investor properties historically have had higher default rates compared to owner occupied properties. A difficulty arose during the housing bubble when borrowers began reporting investor properties as owner occupied properties to obtain better loan terms. The result of this trend created noise in the data. Specifically, the percentage of investor properties in a pool of mortgages was understated. To reduce the noise we use the “home” zip code provided by the credit data company and match it with the zip code of the property backed by the loan in the mortgage pool. If there is a match, then there’s a good chance that the borrower lives in the home. If the two zip codes do not match then there’s a good chance the borrower does not live in the home and receive mail there. Figure 6 shows the default rates of the two sets of borrowers. It is clear that when the zip code of the property matches the zip code that the credit company has on file as the “home” zip code of the borrower the default rate drops dramatically. This trend, while shown for Subprime in Figure 6, is consistent across all sectors. At TCW we use these results to find pools with a higher percentage of true owner occupied loans in pools to generate higher cashflows for investors.

Figure 6: Subprime Borrowers With/Without a Zip Code Match to Credit File

Sources: Equifax, Corelogic, TCW

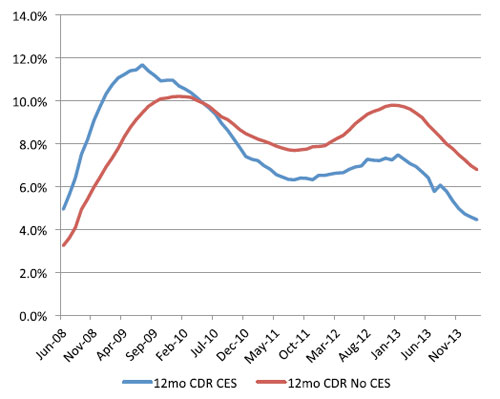

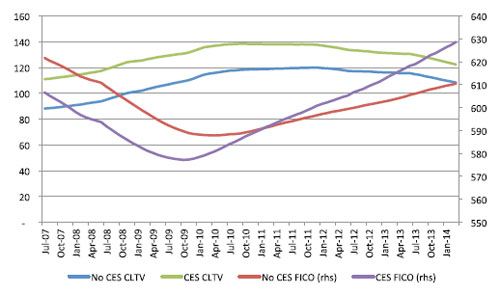

Closed End Seconds

During the housing bubble secondary financing was often used to reduce barriers to entry in the housing market. A large volume of no down-payment, 80/20 loans were originated. This Closed End Second (CES) lien product was most often employed in the Subprime market. When the bubble burst and home prices fell dramatically, these noequity borrowers defaulted quickly and at a faster pace than borrowers without closed end second lien loans. This dynamic jibes with intuition. What is often overlooked, however, is that after the initial large wave of defaults passed through the liquidation pipeline, borrowers with CES loans began to default at a lower rate than their less levered peers. The remaining CES borrowers’ FICO scores cured at a faster pace as the housing market began to recover. Figures 7 and 8 illustrate this fascinating dynamic.

Figure 7: Subprime Borrowers With/Without Closed End Seconds Default Trends

Sources: Equifax, Corelogic, TCW

Figure 8: Subprime Borrowers With/Without Closed End Seconds FICO and CLTV Trends

Sources: Equifax, Corelogic, TCW

Investors who are unaware of this important shift are likely to sell bonds with high percentage of CES at a discount to the market when they should be demanding a premium.

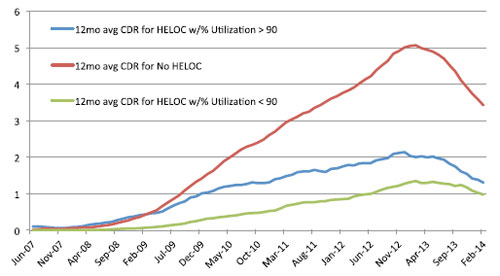

HELOCs

In addition to Closed End Seconds, borrowers have had access to Home Equity Lines of Credit (HELOCs) to tap equity in their homes. Unlike CES borrowers, HELOC borrowers do not have to draw the entire loan amount at origination. Typically there is a draw period (usually 10 years) during which the borrower can use the HELOC as they would a credit card. After the draw period ends, the borrower must pay back the loan during the repayment period and may not make additional draws. HELOCs are typically second liens and can give us insight into default trends. This type of financing was more typical among Prime borrowers. Intuition might persuade investors to believe that a borrower with a second lien HELOC has a higher risk of default. The opposite is true, however. Figures 9-11 show that borrowers who do not max out their HELOCs typically have higher FICOs and are a lower default risk. Surprisingly, even if the HELOC is near capacity default rates are still lower for borrowers with HELOCs. All things being equal, the additional leverage has proven to be a strong indicator of better underwriting at origination.

Figure 9: Prime Default Trends for Borrowers With HELOCs

Sources: Equifax, Corelogic, TCW

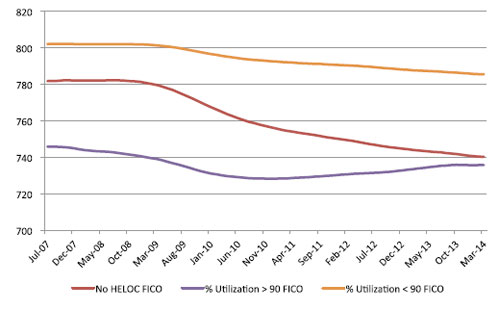

Figure 10: Prime HELOC FICO Trends

Sources: Equifax, Corelogic, TCW

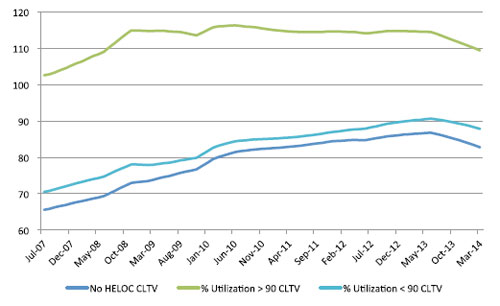

Figure 11: Prime HELOC CLTV Trends

Sources: Equifax, Corelogic, TCW

Current Credit Scores

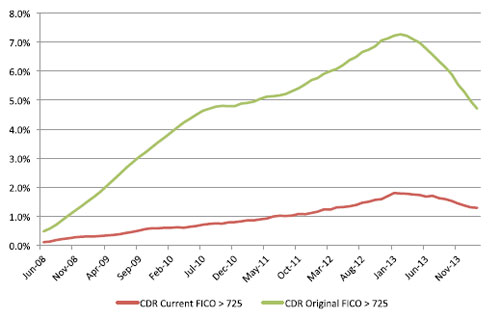

Finally, we have found that updated credit scores are essential to understanding the default risk of the remaining borrowers in the pool. Original credit scores are seven plus years old. Figure 12 shows that if investors rely upon stale credit scores their default expectations will be much different from reality.

Figure 12: Current FICO Versus Original FICO Default Trends

Sources: Equifax, Corelogic, TCW

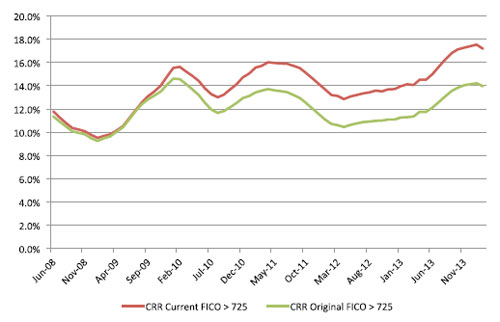

Moreover, these updated credit scores are also helpful when assessing future prepayment expectations as illustrated in Figure 13.

Figure 13: Current FICO Versus Original FICO Voluntary Prepayment Trends

Sources: Equifax, Corelogic, TCW

Conclusion

When it comes to understanding how to set expectations for future default and prepayment trends, TCW utilizes updated consumer credit data. As seen above, intuition is challenged by the results of sound quantitative analysis. ntuition would have us believe that subprime borrowers with more financial leverage would always default at a higher pace than their less levered peers. However, our willingness to constantly reevaluate fresh data, such as the consumer credit data trends, brings the insight that the non-intuitive truth can hold substantial value for the investor.

Investing in the Non-Agency RMBS asset class requires discipline to evaluate the ever changing fundamental and technical landscapes. We believe that the incorporation of consumer credit information into the analysis gives TCW a large competitive advantage to managing unforeseen risks as well as finding alpha generating opportunities.

This material is for general information purposes only and does not constitute an offer to sell, or a solicitation of an offer to buy, any security. TCW, its officers, directors, employees or clients may have positions in securities or investments mentioned in this publication, which positions may change at any time, without notice. While the information and statistical data contained herein are based on sources believed to be reliable, we do not represent that it is accurate and should not be relied on as such or be the basis for an investment decision. The information contained herein may include preliminary information and/or "forward-looking statements." Due to numerous factors, actual events may differ substantially from those presented. TCW assumes no duty to update any forward-looking statements or opinions in this document. Any opinions expressed herein are current only as of the time made and are subject to change without notice. Past performance is no guarantee of future results.

© 2014 TCW