In previous commentaries we have discussed the benefits of using a diversified financing currency approach for investing in gold by which we mean using two or more currencies (rather than just the US dollar) to make gold purchases. The example we have used to demonstrate the approach was to construct a time series of the price of gold purchased with an equal weighted basket of dollars, euro, yen and pound. Our analysis showed that the primary effect of taking this approach was to allow an investor to diversify away some of the idiosyncratic risks associated with the financing currency (for example, the dollar) used to make the gold purchases. When an investor buys gold they are explicitly expressing a long gold, short dollar view i.e. they expect the price of gold to increase relative to the dollar. The implication of this for investors is that the price of gold in dollars is impacted not just by gold supply and demand factors but also supply and demand factors that impact the value of the dollar. By increasing diversity in funding currencies an investor is able to reduce exposure to the risk factors that drive individual currencies and “accentuate” the risk factors that drive gold. Ultimately we believe this is of critical importance for medium to long-term gold investors especially for those that may not have a strong view on the future direction of the financing currency and as such may not want or desire concentrated investment exposure to the dollar.

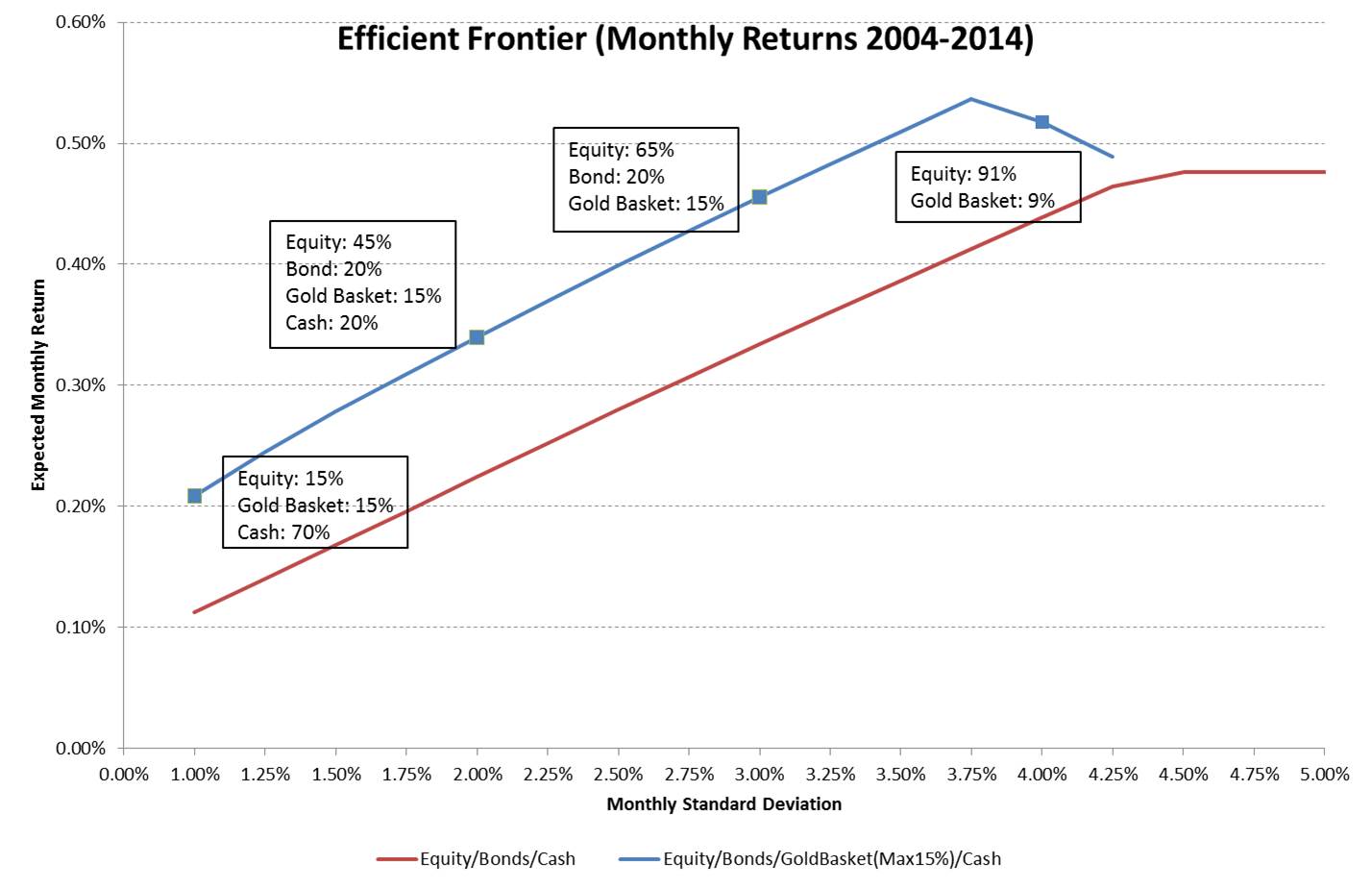

We now extend this discussion on financing currency diversification with an illustrative analysis of the impact on portfolio efficiency of adding a ‘diversified’ gold position to a traditional stocks and bonds portfolio. Adopting a mean/variance optimization process, efficient frontiers have been constructed for a stocks and bonds portfolio and a stocks, bonds and gold portfolio. The CRSP US Total Market Index is used as an equity market proxy and the Barclays US Aggregate Bond Index as a proxy for the bond market. A ‘diversified gold’ strategy (Gold Basket) is defined as gold purchases financed with an equally weighted basket of the euro, yen, pound and dollar with daily rebalancing. A covariance matrix for the three assets is constructed using ten years of monthly returns data with the expected return for each asset being defined as the geometric mean of monthly returns. Note also that two constraints are applied during the optimization process i) no leverage is allowed i.e. portfolio weights must be between 0% and 100% and ii) in the spirit of more closely reflecting real world outcomes the maximum holding of gold in any portfolio is limited to 15%.

We must stress that the intention of the analysis is not to recommend a specific portfolio allocation but rather to show the relative impact on portfolio efficiency of adding a diversified gold position to a traditional stocks and bonds portfolio. And it must be emphasized that all the usual concerns that pertain to mean-variance optimization also apply to this analysis: in particular the difficulty in estimating the co-variance matrix and the sensitivity of the analysis to forecasts of expected returns.

The chart below shows the shift in the efficient frontier from adding Gold Basket to a stocks and bonds portfolio with the maximum gold allocation capped at 15%. For fours points on the stocks/bonds/Gold Basket efficient frontier (the blue line) we also show the optimized portfolio allocations. For all but the highest risk portfolios which unsurprisingly are heavily skewed towards an equity allocation, the gold allocation results in a more efficient portfolio relative to the stocks and bonds portfolio with a shift higher in the efficient frontier for a given level of standard deviation.

Source: Bloomberg LP; Treesdale Partners calculations. Past performance is not indicative of future performance

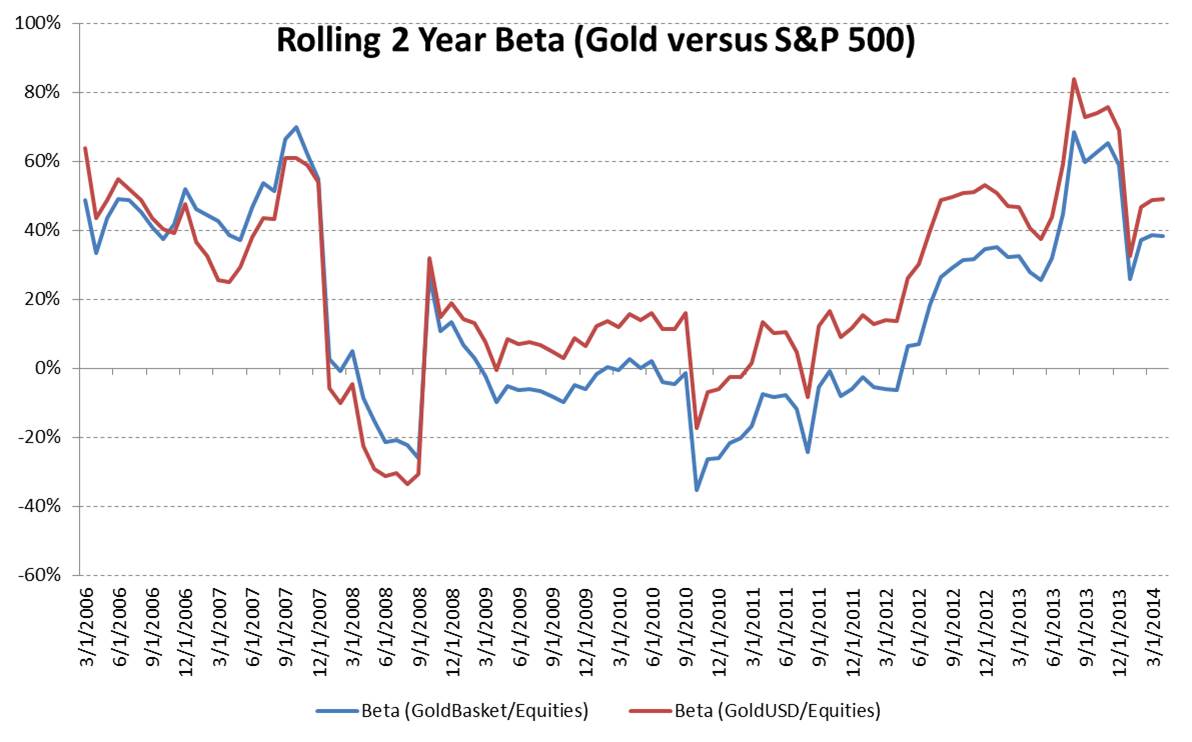

Another consideration for potential investors assessing the impact of gold on portfolio efficiency is the extent to which gold price variability is driven by broader market variability – in other words how much of the risk of investing in gold is driven by systematic risk. Beta is a measure of an asset’s systematic risk – in effect how much of an asset’s volatility can be ‘explained’ (is caused) by the volatility of the broad market. A beta of 1 indicates that the asset's price will move with the market. A beta of less than 1 indicates that the asset will be less volatile than the market. A beta of greater than 1 indicates that the asset's price will be more volatile than the market. In the chart below we plot the rolling two year beta of the Gold Basket versus VTI using the same monthly returns data as was used in the efficient frontier chart. For comparison we also plot the beta of gold priced in dollar terms versus stocks. The chart shows that while there has been variability in gold beta versus stocks it has consistently been below 1. Also of note the beta for Gold Basket has been below the beta for gold priced in dollars, over the reference period.

Using the ten year history of gold and equity prices as a guide we have constructed an illustrative efficient frontier for a stocks and bonds portfolio and a stocks, bonds and gold portfolio to show the relative impact on portfolio efficiency of adding gold. The data also show that over the same period the beta of Gold Basket versus stocks has been consistently below 1.

Source: Bloomberg LP; Treesdale Partners calculations. Past performance is not indicative of future performance

(c) AdvisorShares