The massive post-GFC Quantitative Easing (QE) in the USA, EU, and now in Japan has repaired the global banking system’s balance sheet. Debt of various qualities, worth trillions of dollars, was moved from struggling banks to the central banks at book value where it is likely to run out to maturity or rollover.

The new cash injected into the banks has not yet been fully multiplied by the fractional-reserve banking system because consumers need to first work out their overleveraged household balance sheets before they borrow again.

So banks returned most of the QE cash to the central banks as reserves but some of it found its way to the market to underwrite various forms of foreign investment and carry trade destined for attractive yields in Emerging Markets (EM).

QE tapering is reversing the flows exposing the EM’s inherent problems. The countries most at risk are: China, India, Turkey, Thailand, Brazil, and Ukraine.

The search for yield added to funds flow from developed markets to emerging economies in recent years. According to Bank of America Merrill Lynch, external bond issuance from emerging markets more than doubled to $2 trillion in the five years to end-September 2013. Including bank loans, EM had attracted investment from abroad totalling $5 trillion by autumn 2013, nearly $2 trillion more than five years ago.

The carry trade was once described in Robin Hood terms as “borrowing from the rich to lend to the poor.” A carry trade is a strategy in which the trader invests in a high yielding instrument financed by borrowing in a low yielding instrument.

Popular carry trades include investments in low grade bonds financed by borrowings in high grade bonds, investments in long maturity bonds financed by borrowings in short maturity bonds, and options strategies in which the investor is long theta (receiving time premium).

Historically, one of the most popular carry trades has been in the foreign exchange markets where carry traders invested in high yielding currencies using funds provided by borrowing in low yielding currencies.

The classic examples of these trades were Australian dollar investments financed by Japanese yen borrowings, and Mexican peso investments financed by U.S. dollar borrowings. And more recently, borrowing at rock bottom rates in the USA to invest in China.

The round trip FX carry trade is a free lunch as long as the target currency does not weaken which usually requires intervention by the target’s central bank to maintain FX stability. This has been the case in highly regulated China although more recently the Chinese currency was allowed to fluctuate for a while in a wider range scaring off the modern Robin Hoods.

An estimated US$2 trillion dollars is involved in the global carry trade - approximately half of it in China - the largest of the EMs.

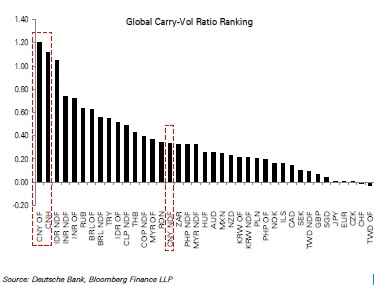

Here are examples of the most popular carry trades - chart.

Source: http://www.euromoney.com/Article/3217737/Chinas-FX-carry-trade-the-next-shoe-to-drop.html

Bilal Hafeez, global head of FX strategy at Deutsche pointed out that volatility in USD/CNY is very low, meaning the renminbi delivers the highest volatility-adjusted carry in the world.

QE Tapering will reduce Emerging Markets Carry Trade

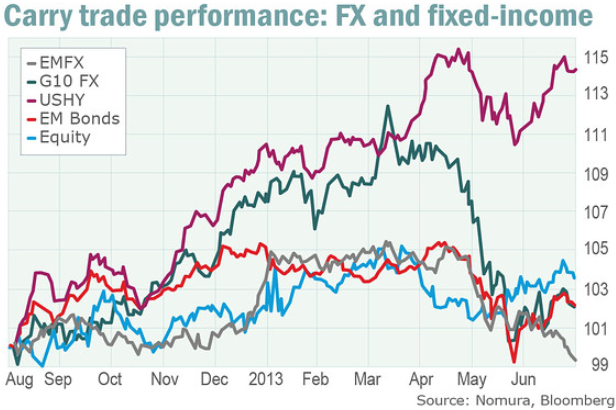

Saumya Vaishampayan of WSJ noted in August 2013 that some investors have gotten past the market turmoil that erupted when Ben Bernanke first hinted that the Federal Reserve might scale back its bond buying later this year. Not those who play the carry trade in the currency market.

When concerns that the USA Fed would slow its monthly asset purchases of $85 billion started surfacing in May 2013, the trade fell apart as the chart shows. Note the gap between the performance of carry trades with emerging-market currencies (gray line) and U.S. high-yield bonds (magenta line):

Source: http://blogs.marketwatch.com/thetell/2013/08/05/why-fx-carry-trades-arent-performing/

The funds from developed countries that chased higher yields in the EM are now returning home. The trend should continue throughout 2014.

The funds outflow is also weakening Emerging Markets’ equities and pushing up their interest rates.

Which Emerging Markets are most at risk?

The reversal of easy money flow will expose many of the weaker EMs - especially those with balance of payments problems, high current account deficits and where credit grew faster than GDP for an extended period.

Ray Dalio of Bridgewater sounded a cautious note about investing in emerging markets, especially in equities, which have plunged in value this year. Emerging markets will not be an "an attractive place" to invest in the near future "given flows and pricing."

He said emerging markets face "a major balance of payments problem" that will eventually lead to significant problems.

We are "going to have the emerging market crisis," Dalio said during a question and answer period.

India should "prepare for the worst" since it has been one of the biggest beneficiaries of foreign capital flows that are already bypassing emerging market equities, he added.

Source: http://www.reuters.com/article/2013/09/06/hedgefunds-dalio-japan-idUSL2N0H21LH20130906

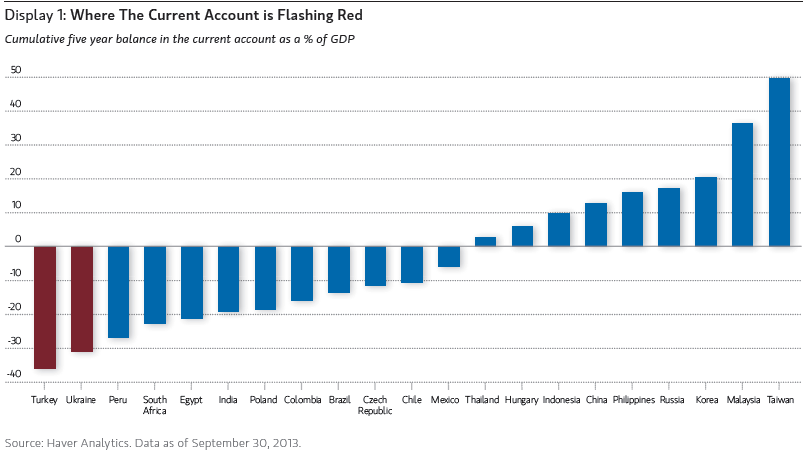

Morgan Stanly identified Turkey and Ukraine with the highest Current Account Deficits.

Chart Source:

Fast credit growth indicates future crisis

After failing to spot the global crisis back in 2008, many of the world’s leading financial authorities began studying how to spot the next crisis. By 2009, the BIS, the ECB, and the NBER had all released papers, followed in 2011 by the IMF.

Though arrived at separately, the conclusions are strikingly similar. Surprisingly, many of the most oft-cited indicators, such as rising current account or government deficits, were not consistently clear predictors of crisis.

The most telling indicator is when credit, particularly private credit, grows faster than GDP for an extended period.

Where is this signal flashing red today? The IMF was most specific in defining the warning sign. It said that if the ratio of credit to GDP rises by at least 5 percentage points in any given year, this threshold “works reasonably well in signaling a crisis.”

Between 2008 and 2012, the ratio of credit to GDP rose by a simple average 2 of about 2.5 percentage points per year across emerging markets, and rose at or slightly above the IMF threshold - between 5 and 6 percentage points a year - in three of the main emerging markets: Thailand, Turkey and Brazil.

The nation that stands out, in a negative way, is China, where the ratio of credit to GDP grew 65 percentage points, or an average of 13 percentage points a year over the last five years.

Source: Morgan Stanley

More readings on Emerging Markets and Carry Trade

Adventures in the Carry Trade by John Bilson,

http://www.cmegroup.com/education/files/bilson-adventures-in-the-carry-trade.pdf

Emerging markets face painful carry trade pay-back by Natsuko Waki

http://www.reuters.com/article/2014/03/07/emerging-carry-idUSL6N0M32N520140307

2014: Another year of the dollar; Currency could shift into new bull market by Peter Garnham

Gundlach – Where to Expect the Next Crisis by Robert Huebscher

http://www.advisorperspectives.com/newsletters13/pdfs/Gundlach-Where_to_Expect_the_Next_Crisis.pdf

Russia, the Ukraine, and the Markets: Broken BRICs by Rana Foroohar

http://time.com/12221/emerging-markets/

China’s weakening currency: Risks in unwinding yuan carry trade by Craig Stephen

http://www.marketwatch.com/story/chinas-weakening-currency-2014-03-02?pagenumber=1

FX Theory: Carry Trade and Reverse Carry Trade

http://snbchf.com/fx-theory/interest-rate-and-carry-trade/

Emerging-Market Shakeout Putting Reserves Into Focus: Currencies by Ye Xie and John Detrixhe

China's yuan carry trade, an anchor and a risk for Asia by Vidya Ranganathan

http://www.reuters.com/article/2014/01/30/us-markets-asia-china-idUSBREA0T0N720140130

George Bijak, MBA, is an investment strategist and director of GB Capital Pty Ltd - a provider macroeconomic research for global macro and dynamic multi-asset allocation investment strategies. Their USA Profits and S&P 500 Outlook based on the Corporate Profits Growth Leading Indicator www.cpgli.com signalled major market turning points: 2007 top and 2009 market bottom.