STOCKS MIXED AMID LIGHT DATA

Equity markets were mixed last week with the Dow moving higher, the S&P 500 flat, and technology stocks as represented by the NASDAQ Composite moving sharply lower. Small cap stocks suffered even deeper losses, losing nearly 2% in the week.

The week was fairly light on economic data, with Janet Yellen’s testimonies before the Joint Economic Committee and Senate Budget Committee in Washington, DC perhaps taking top billing. Chairwoman Yellen mostly reiterated her points from last week’s FOMC meeting: the group would maintain its low interest rate policy for the foreseeable future (and that it would be tied to overall economic conditions), and that its bond purchases would likely end in the fall. She noted the economy generally appeared healthier following the winter weather disruption from a few months ago, absent a stalling housing market that is causing some concern among FOMC members.

The highest profile economic indicator of the week occurred on Monday with the ISM Non-Manufacturing Index release. The measure beat expectations, coming in at 55.2, which was the highest reading in eight months. Gains were broad based, with seven of the 10 underlying components improving in April. However, among the contractions was employment, which fell 2.3 points to 51.3. This measure just recently moved into expansionary territory, and now stands slightly above zero growth levels.

On the positive side, both business activity and new orders – two of the most important components of the index – experienced robust gains of 7.5 and 4.8 points, respectively. This suggested broader economic improvement, as was further emphasized by the report’s qualitative assessment: “[t]he majority of survey respondents’ comments indicate that both business conditions and the economy are improving.”

On Tuesday, the Census Bureau released its monthly international trade report. Market participants were encouraged to see the trade deficit narrow to 40.1 billion from 41.9 billion in March as exports bounced back from a February decline. Imports increased slightly, but less than exports’ 2.1% uptick. Much of March’s narrowing of the trade deficit occurred as a result of a smaller oil gap; the latter decreased from a deficit of $20 billion to $18.4 billion. Despite the overall improvement, analysts noted that the Commerce Department projected a slightly smaller trade gap in its initial estimate of first quarter GDP; thus, this latest data is likely to have a small negative effect on the next growth estimate.

While data was limited in the U.S. last week, one major global report capturing traders’ attention was the HSBC China PMI Index for April. That measure came in at 48.1, the fourth straight month in contractionary territory. While a bit at odds with the official government manufacturing index, which recently suggested a figure of 50.4, HSBC’s report is considered more dependable. Nevertheless, continued softness in the country’s manufacturing sector is contributing to concern about the country’s impact on global growth. As noted by HSBC Chief Economist Qu Hongbin in the Wall Street Journal, “Both the new export orders and employment subindexes contracted, and were revised down from the earlier flash readings. These indicate that the manufacturing sector, and the broader economy as a whole, continues to lose momentum.”

DOLLAR BULLS DROP THEIR HEADS IN FRUSTRATION

For some time, strategists have been bullishly positioned on the U.S. Dollar, anticipating a rally that failed to materialize. The arguments were straightforward – the Federal Reserve is exiting its easing cycle, Europe is facing deflationary pressure and likely to ease further, and the economy in the U.S. is on improving footing. Those expectations, while true to some extent, are not translating into gains for the Dollar, leaving many frustrated. The Dollar is suffering from a bad case of dejection and could struggle to see a sustained breakout for some time.

Throughout the second half of 2013 and the early part of 2014, the Dollar has steadily lost value, dropping from a high near 85 last summer to a touch below 80 more recently.

Source: TradingEconomics.com

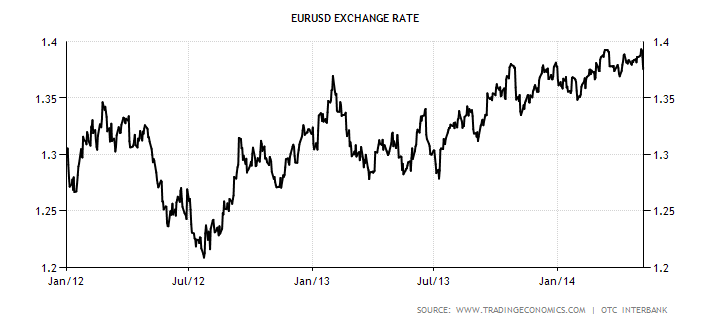

A major culprit of the weakness is trading in the Euro. Since the time European Central Bank President Mario Draghi offered to do “whatever it takes” to save the Eurozone, the

Euro itself has been on a veritable tear. The Euro dropped to $1.23 around the time of the speech, and rose at a nearly straight line since, reaching $1.37 recently.

Source: TradingEconomics.com

Despite the ongoing concern about sinking inflation trends, and expectations that the ECB could start an easing program of its own, the Euro has accelerated its rally in 2014. The latest week offered a glimpse into the possibility that the trend may finally break down, though.

During the second half of last week, the Euro lost more than 1% after Draghi stated that the ECB would be ready to act if inflation continued to fall. There has long been a belief that as the Fed moved away from its asset purchases, the ECB would be moving towards increasing its easing efforts. Such a development could have a dramatic impact on the pricing of the Dollar/Euro exchange rate.

The other trend taking place is a strong correlation between the Dollar and Treasury yields. YTD, with Treasury yields in steady decline, the Dollar has followed suit. The decline in yields was initially attributed to weaker economic data resulting from the winter weather period. We are finding, however, that a number of large pension plans did quite well in 2013, reducing their funding pressures, and causing them to rebalance portfolios towards fixed income exposure.

Source: Federal Reserve Bank of St. Louis

The Dollar received a technical reprieve last week, owing to Mario Draghi and the Euro. Over the intermediate-term, though, further action from the ECB, or clear signs that the U.S. economy is gaining steam will be required to accelerate the short rally. There is a small possibility the ECB will announce new policy measures at its June meeting, but as we have seen with the ECB in the past, nothing is guaranteed.

THE WEEK AHEAD

Economic news flow picks back up on the data side this week, with a range of reports spanning retail, inflation, manufacturing, and housing. Retail sales are released Tuesday, while industrial production is on tap for Wednesday. GDP figures for the Eurozone and Japan should also be monitored.

Central bank activity is limited this week with just Chile scheduled to release updated policy guidance. Janet Yellen continues her speaking tour of Washington with a Thursday address before the Chamber of Commerce and Small Business Administration.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

(c) Fortigent