Executive Summary

- Macro conditions are lukewarm but positive and largely absent any systemic risk.

- Momentum stocks have fallen out of favor as the market rotates into names with more attractive valuations.

- Europe and especially the U.K. have been showing signs of strength despite geopolitical risk with its energy supplier, Russia.

- The “safety” of sidelined cash exposes investors to what we view as the greatest current risk in the market — upside risk.

The Goldilocks economy is making a comeback. After concerns about overheating in the fourth quarter gave way to a first quarter economy that was way too cold, we find ourselves in a place that feels just about right. U.S. corporate profits will likely — and unexpectedly — finish the latest reporting season with another quarter of positive year-over-year growth, while reports on manufacturing, consumers and housing have been fair to good. Bond yields among Europe’s periphery are at record lows, though this has more to do with the looming threat of deflation — and the associated possibility that the ECB will introduce quantitative easing — than a robust economic renaissance on the Continent. The contribution of emerging markets to global growth trumps that of the U.S. despite ongoing structural concerns about the developing economies. As we said, pretty lukewarm overall. But lukewarm seems just about enough to move this market forward, absent any systemic crisis.

Rotation Away from Momentum

It certainly hasn’t been all good for the equity markets as the days of easy money wind down; after the Fed’s latest cut to its asset-purchase program, the central bank’s bond buys now stand at $45 billion per month, the same level before Operation Twist was instituted in December 2012. The full carnage from the stimulus taper is being obscured, however, as it hasn’t resulted in an exodus from equities but rather a generally positive rotation from momentum stocks to value names. While broad market fundamentals are still intact, the air is being let out of those stocks with extreme valuations. For example, the highest-price momentum stocks were the worst performers in April after being the best performers in the first quarter. And the heretofore high-flying U.S. small-cap equities are the only asset class that is negative year to date; they’re even being beat by the long-unloved emerging markets.

Positive performance continues to be widespread though, as nine of the ten asset classes in a broadly diversified portfolio are positive or flat year to date. While a broad market offers well-diversified investors boundless opportunity, those with narrow, U.S.-centric portfolios will miss out.

U.S. Fundamentals Show Steady Improvement

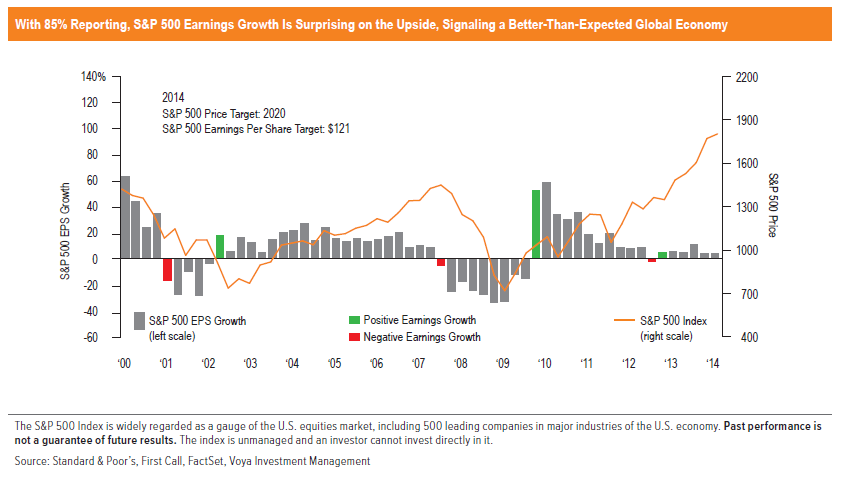

There is always noise around the trend, but the domestic trend is positive and getting better — still lukewarm, but definitely warmer. U.S. corporate profits are the fundamental driver of markets; with 85% of the S&P 500 having reported first quarter results, the numbers are better than anticipated. Year-over-year earnings growth is about 2%, as 74% of the companies beat Wall Street’s expectations. Top-line revenue growth is also looking stronger and, at 2.8%, outpaced earnings growth in the first quarter.

Corporate earnings are reliant on the consumer and manufacturing, and here too the trend is positive. U.S. retail sales jumped to their highest level ever — $433.9 billion — in March, a 1.1% increase over an upwardly revised February and the biggest gain since September 2012. Consumer spending jumped 0.9%, and consumer incomes were up 0.5%; this reflected the largest increase in real consumption since August 2009 and the biggest gain for real disposable income since last September. On the manufacturing side, the resurgence of energy production in the U.S. and the wave of cheap natural gas continue to provide a tailwind in this sector. The ISM Manufacturing Index climbed to 54.9% in April — the highest level since December — from 53.7% in March.

So while the initial estimate of first quarter U.S. GDP growth came in at a concerning 0.1%, it’s important to note that this backward-looking report will not be final until we are well into what should be a much better quarter for economic growth.

International Highlights

The world’s stage is always rife with the good, the bad and the ugly. Here are but a few examples.

India. India is nearing a pivotal parliamentary election, and the likely winner is Narendra Modi of the right-wing Bharatiya Janta Party (BJP), who bills himself as pro-growth and business friendly. India has been floundering of late and any hint of improved growth for its one billion people could have a significant impact on global growth.

Europe/U.K. Europe has recently emerged from recession, and the bond yields offered by its most troubled members have receded sharply in recent months, further facilitating growth for the currency bloc. But the real story is the United Kingdom.

Unemployment in the U.K. is at a five-year low of 6.9%, while wages have increased at a pace in excess of inflation and housing prices spiked nearly 11% in 2014; this helped British retail sales post their best quarter in nearly eight years during the first quarter. The first quarter also saw GDP grow at a pace of 3.1% year-over-year and 0.8% quarter-over-quarter, while manufacturing and services PMIs rose to 57.3 and 58.7, respectively, in their latest readings. Britain was the only developed country to implement austerity that is reining in government spending and reducing the need for higher taxes; the U.S., on the other hand, having implemented considerable fiscal stimulus to soothe the impact of the credit crisis, subsequently raised taxes and is caught in a slower-growth economy despite a host of natural advantages.

Emerging markets. According to a survey by the United Nations Conference on Trade and Development, the total value of cross-border M&A activity climbed 5.2% in 2013 to $349 billion, with emerging market-based organizations accounting for 56.5% of this figure. Deals included:

- Chinese company Shuanghui’s acquisition of U.S. pork producer Smithfield Foods

- PetroChina’s purchase of part of Italian oil group ENI’s Mozambique business

- Indonesian oil company Pertamina’s purchase of ConocoPhillips’ Algerian oil field stakes

- CNOOC of China’s $19 billion purchase of Canada oil and gas company Nexen

- Kuwaiti foreign direct investment in other countries soaring 159%

Meanwhile, global M&A volume has already topped $1 trillion for 2014, and the emerging markets have continued to make their presence felt.

Russia. Russia continues to flex its power on the Ukraine border, hoping that U.S. and German governments will succumb to pressure by domestic corporations doing business in Russia and go soft on sanctions. But Russia, with more than $50 billion in fund outflows already and an economy on the precipice of recession, has significantly more to lose than either the U.S. or Germany.

Tectonic Shifts Are Positive Catalysts for Growth

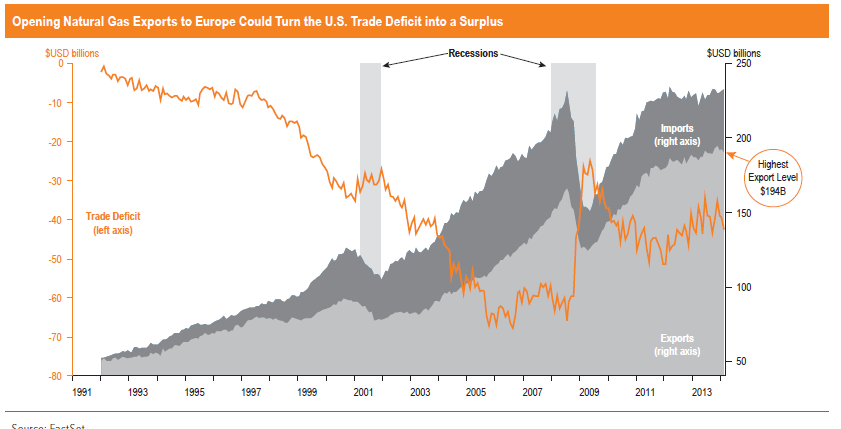

Tectonic shifts in energy and global trade were front and center last month as Germany and the U.S. met for further negotiations around the Transatlantic Trade and Investment Partnership. A deal here could boost annual economic output by more than $100 billion each for the EU and U.S. and make it easier for the U.S. to export natural gas to Europe. The Ukraine crisis has highlighted European vulnerability in its reliance on Russia for oil and gas, and the U.S. is pushing the EU to diversify its energy supplies as a result. The current U.S. net import-export position of about $415 billion a year is roughly 2.6% of its $16 trillion economy. Opening natural gas exports potentially could turn the trade deficit into a trade surplus, effectively doubling the pace of GDP growth.

Neither too Hot nor too Cold Is Just Right

Given the pessimistic attitude that continues to dominate investor psyches and asset allocations, there is a lot of fallow cash on the sidelines; the re-emergent Goldilocks economic scenario could spark this dry tinder and propel the market higher, or it could just fizzle out. While the consensus seems to be excessively positioned for the latter, we recommend a normal allocation for investors that are geared toward building wealth while maintaining prudent risk control, as fundamentals suggest that the biggest risks to the current market are to the upside.

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

©2014 Voya Investments Distributor, LLC • 230 Park Ave, New York, NY 10169

CID 9686