Schroders Monthly Markets Review: Overview of Markets in April 2014

Highlights:

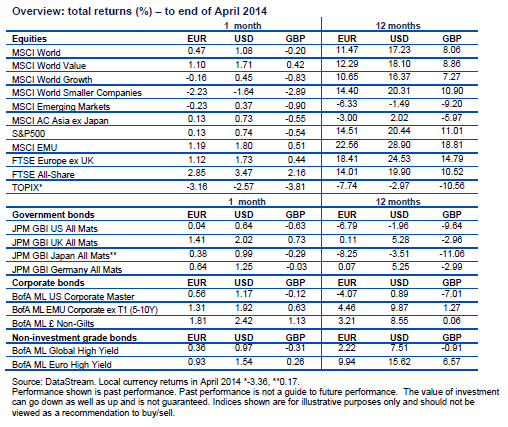

– Global equities edged higher in April. Some stronger macroeconomic data from developed economies helped to support returns but the ongoing crisis in Ukraine remained a headwind for equities. Developed markets outperformed emerging markets.

– In the US, a generally firmer tone to macroeconomic data and a broadly encouraging corporate earnings season supported sentiment. Investors were also reassured by comments from Federal Reserve (Fed) Chair Janet Yellen about maintaining low interest rates.

– Eurozone stocks were boosted by further positive macroeconomic data and signs that the European Central Bank (ECB) could consider further monetary policy easing. UK stocks rose, helped in part by merger & acquisition activity.

– Japanese equities posted negative returns after the sales tax increase came into effect and consumer confidence data was weak.

– The crisis in Ukraine remained a key focus for emerging markets. Chinese GDP growth for the first quarter was better than expected but other economic data was weaker and weighed on returns.

US

The S&P 500 rose 0.7% overall in April. Large stocks outperformed mid and small caps, with the latter providing the weakest return of the three. While economic data continues to support signs of a US recovery, the crisis in Ukraine remained a key risk factor for equity markets. By the end of April the US imposed further sanctions on seven government officials and 17 companies linked to President Putin.

Meanwhile US economic data remained largely positive. The US economy added 192,000 new jobs in March while the unemployment rate remained stable at 6.7%. Initial US jobless claims dropped towards 300,000, the lowest level since May 2007. US March retail sales jumped by 1.1% on the previous month, the largest rise in one and a half years. Investors were reassured by comments from Fed Chair, Janet Yellen, about maintaining low interest rates. The Fed continued to taper its quantitative easing program by a further $10 billion a month in April.

First quarter GDP figures showed the economy grew by a mere 0.1% which – as the number is annualized - means virtually no growth at all. However, a weak figure was not unexpected given the severe cold and snow during the quarter which meant that many were unable to work or shop. In terms of the components of GDP the weather weighed on residential investment, sales of motor vehicles and exports. Each of these is expected to rebound in the current quarter and lift real GDP back to a 3% pace. The bright spot was consumer spending, which was mainly due to a sharp rise in healthcare spending following the Patient Protection and Affordable Care Act (PPACA) signed by Barack Obama in March 2010. The Act expands the affordability and availability of private and public health insurance to Americans. Its effect is expected to continue into the second quarter and beyond.

Eurozone

Eurozone equities delivered positive returns in April. Despite inflation dipping to just 0.5% in March, the ECB elected to keep monetary policy unchanged. However, ECB president Mario Draghi said that quantitative easing was discussed at the meeting and that the bank will act if low inflation becomes prolonged. Preliminary figures for April showed inflation rose to 0.7%. Other macroeconomic data continued to be encouraging. The flash eurozone purchasing managers’ index (PMI) for April came in at 54.0, a 35-month high and up from 53.1 in March. The German Ifo business confidence survey rose to 111.2 in April from 110.7 in March. The ECB’s lending survey showed that net demand for household and corporate loans turned positive in the first quarter of 2014 for the first time since the second quarter of 2011.

There was good news from some of Europe’s troubled peripheral economies. Spanish GDP grew by 0.4% in the first quarter compared to 0.2% in the fourth quarter of 2013. Portugal held its first regular debt auction since its bailout in April 2011, selling €750 million of 10 year bonds amid strong demand. The successful auction put Lisbon on course to make a ‘clean’ exit from its bailout program, i.e. without a precautionary credit line from the EU. S&P raised Cyprus’s credit rating by one notch to B citing reduced risk to debt repayments.

By country, France was amongst the strongest markets while Ireland underperformed. By sector, energy registered the strongest returns for the month, boosted by a higher oil price as the Ukraine crisis intensified. Utilities lagged behind after strong performance in the first quarter. Merger & acquisition activity was a feature of the month, with cement groups Holcim and Lafarge announcing a tie-up and industrial firm Alstom drawing interest from GE and Siemens.

UK

The FTSE All-Share index outshone the majority of other developed markets in April. It gained 2.2%, led higher by larger companies (the FTSE100 was up 3.1%). The healthcare sector had the largest positive effect on overall index performance thanks in no small part to index heavyweight AstraZeneca, which saw its share price jump as US rival Pfizer made an offer to buy the company.

The latest preliminary estimate of UK GDP shows economic growth accelerated from 0.7% in the last three months of 2013 to 0.8% in the first quarter – a strong and promising start to 2014, but the estimate fell short of the City’s consensus estimate of 0.9%. Poor weather conditions at the start of the year have been blamed, as industries such as agriculture saw a sharp contraction. The UK purchasing managers’ index also pointed to expansion as it rose from 55.8 to 57.3 in April.

According to the Halifax house price index, average UK house prices rose by 8.7% in the first quarter of this year – their fastest pace of annual growth since the third quarter of 2007. This has fuelled speculation that measures will be introduced to cool rising prices, although the market does not expect interest rates to rise in the near future.

Japan

Japanese equities fell over the month of April, ending 3.4% down in local terms, as the country’s increase in sales tax from 5% to 8% was implemented on 1 April. Heavy losses early in the period were later partly recouped as investors adjusted expectations following the tax increase. Transportation equipment and electric appliances were the weakest-performing sectors over the month. Information & communication and pharmaceutical companies also posted losses. Food and mining were among the strongest sectors.

Investor sentiment in April was again directed by a number of external factors, including the continuing crisis in Ukraine. Traditionally viewed as a safe haven asset, the yen’s rise in times of uncertainty has come to be viewed as a negative for Japanese equities in recent years. This remained true over the month and the focus now moves to any potential additional easing measures by the Bank of Japan, in light of recent disappointing economic data.

The widely-watched Tankan manufacturers’ survey showed a marginal increase in March although large manufacturers and non-manufacturers expect conditions for the current quarter to be challenging following the sales tax hike. March’s consumer confidence reading came in at its lowest level since 2011 and currently wages are not rising in tandem with inflation, which combined with the sales tax increase, could start to depress real incomes. The earnings season for Japanese corporates began at the end of April and is likely to show strong profit growth but relatively conservative forecasts for the coming year.

On the political front, President Obama paid a visit to Tokyo as part of his Asian tour and, despite security pledges from the US, no bilateral trade agreement could be forged. However, some progress has been made and there is still political commitment to the current negotiations over the 12-nation Trans-Pacific Partnership (TPP) trade pact.

Asia (ex Japan)

Asia ex Japan equities delivered marginally positive returns in April as better-than-expected first quarter GDP growth in China and a continuing US economic recovery boosted sentiment for stocks. Despite first quarter growth coming in at 7.4% year-on-year, Chinese equities fell over the month with other data negatively impacting the market. The widely-watched HSBC manufacturing PMI saw its March reading hit an eight-month low of 48 while the country’s M2 money supply – a key leading indicator for activity growth – expanded by just 12.1% year-on-year in March, its slowest pace since 2001. Worries also swirled around a slowdown in property prices as March saw fewer cities recording month-on-month increases, with scarce credit for both developers and buyers affecting short-term sentiment. In contrast, Hong Kong equities delivered gains over the month as it shrugged off China concerns amidst a solid earnings season for the city’s blue chips. A cross-border stock trading pilot scheme, in co-operation with Shanghai, also spurred further gains.

Meanwhile, Taiwan was also up as its export-dependent economy expanded at 3% year-on-year in the first quarter – its fastest pace since the last quarter of 2012 – driven by strong exports and the improving outlook for the global technology sector. Fellow exporter Korea also notched up gains on the back of strong March exports, a solid current account surplus and recovering home sales. Lower unemployment and stable inflation in Australia saw its market finish up. In ASEAN, all the major markets posted positive gains. Indonesia, although up, saw more muted gains as legislative

elections delivered a result that suggests a likely coalition government after presidential elections are held in July. The Philippines gained on continued robust economic data. In Thailand, murmurings of a possible settlement to the current political impasse boosted investor sentiment. Market optimism surrounding BJP candidate Narendra Modi initially saw India’s market gain before profit-taking in large blue chips ensued, seeing it finish the month in negative territory.

Emerging Markets

Geopolitical tension in Ukraine remained the central concern for investors over the month. Heightened conflict in the eastern part of the country prompted concerns about the possibility of Russian military action and resulted in increased diplomatic sanctions from the West. Investors also focused on disappointing Chinese economic data. As a result of poor performance from some of its Asian and emerging European constituents, the MSCI Emerging Markets (EM) Index underperformed its developed world counterpart.

Latin America was the best performing region in April, led by gains in Peru as index heavyweight Creditcorp performed particularly well. In Brazil, ongoing political optimism about a potential change in government ahead of October’s presidential elections continued to drive market gains. The local currency strengthened against the dollar over the month and an expected end to the recent rate tightening cycle was also positive for the market.

The emerging Asian markets marginally underperformed. China and India were the region’s biggest underperformers. Despite China’s better-than-expected first quarter growth of 7.4%, other economic data weighed on the market. These included a poor PMI reading and a slowdown in M2 money supply. In India, higher-than-expected inflation dampened market sentiment and investors took profits following previously strong market performance.

Emerging EMEA underperformed the MSCI EM index, led lower by market falls in Greece and Russia. In Greece, National Bank of Greece and Piraeus Bank performed particularly poorly while in Russia, escalating conflict in eastern Ukraine and increased diplomatic sanctions by the West weighed on investor sentiment.

Global Bonds

The economic picture became more muddied in April, with mixed data releases, persistent geopolitical concerns and central banks doing their level best to avoid revealing their next move. With so little to go on, investors sought to buy into certainty, and fixed income markets enjoyed a further month of gains.

Many investors interpreted Fed Chair Janet Yellen’s comments in March as a precursor to an earlier rate hike. Yet since those comments were made, the Fed has gone to great pains to assure markets that the eventual removal of monetary accommodation will be much more gradual. Markets have had to digest similar vagueness from the European Central Bank and the Bank of England.

Government bonds across the US, the UK and the eurozone fell in the month. The US 10 year Treasury yield fell to 2.65% from 2.72%, mirrored by the UK 10 year gilt yield, which moved from 2.74% to 2.66%. Both core and peripheral European yields also retreated. The German 10 year bund yield ended the month down 10 bps at 1.47%. The Italian 10 year government yield fell from 3.29% to 3.07% and the Spanish equivalent fell to 3.02% from 3.23%.

The investment grade BoA Merrill Lynch Global Corporate Bond Index outperformed the equivalent high yield index by 22 bps to generate 1.02% in April. Sterling corporate bonds outperformed both US dollar and euro names in a month which was positive for all three. Given the stronger growth of the UK economy, and sterling gains against both the dollar and the euro during April, this was perhaps to be expected. UK investment grade names gained 1.29% against US investment grade credit gains of 1.13%, and euro gains of 0.86%. In high yield, euro credits in fact progressed more than US and UK high yield bonds by 16 and 12 bps respectively.

Important Information:

The views and opinions contained herein are those of Keith Wade, Chief Economist and Strategist, Azad Zangana, European Economist and Craig Botham, Emerging Markets Economist, and do not necessarily represent Schroder Investment Management North America Inc.’s house view.

This newsletter is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument mentioned in this commentary. The material is not intended to provide, and should not be relied on for accounting, legal or tax advice, or investment recommendations. Information herein has been obtained from sources we believe to be reliable but Schroder Investment Management North America Inc. (SIMNA) does not warrant its completeness or accuracy. No responsibility can be accepted for errors of facts obtained from third parties. Reliance should not be placed on the views and information in the document when taking individual investment and / or strategic decisions.

The opinions stated in this presentation include some forecasted views. We believe that we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee that any forecasts or opinions will be realized. The opinions stated in this presentation include some forward-looking statements. We believe that we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. There can be no assurance, however, that events will occur as we expect or believe.

Securities mentioned are for illustrative purposes only and should not be viewed as a recommendation to buy/sell. Past performance is no guarantee of future results.

Schroder Investment Management North America Inc. ("SIMNA Inc.") is an investment advisor registered with the U.S. SEC. It provides asset management products and services to clients in the U.S. and Canada including Schroder Capital Funds (Delaware), Schroder Series Trust and Schroder Global Series Trust, investment companies registered with the SEC (the "Schroder Funds".) Shares of the Schroder Funds are distributed by Schroder Fund Advisors LLC, a member of FINRA. SIMNA Inc. and Schroder Fund Advisors LLC are indirect, wholly-owned subsidiaries of Schroders plc, a UK public company with shares listed on the London Stock Exchange. Schroder Investment Management Ltd. is the UK based investment subsidiary of Schroders plc.

Schroder Fund Advisors LLC, Member FINRA, SIPC

875 Third Avenue, New York, NY 10022-6225

(c) Schroder Investment Management