TEMPORARY STRUGGLES IN THE HOUSING MARKET?

Equity markets were flat to negative last week with the S&P 500 roughly flat and small cap stocks, as represented by the Russell 2000, down approximately 0.3%. Technology stocks were hurt last week as the NASDAQ Composite declined more than 1%.

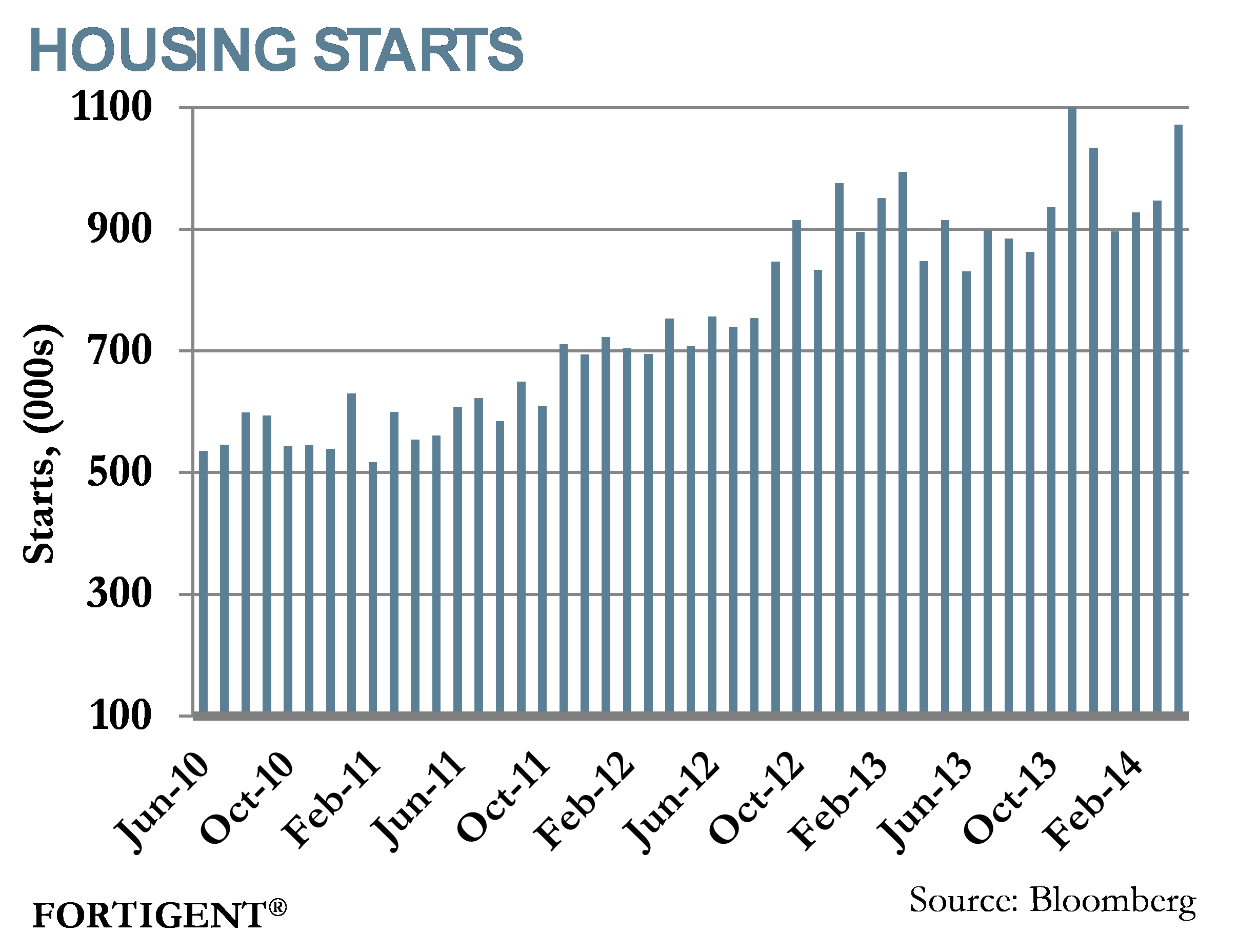

Last week brought about important pieces of economic data with housing market data at the forefront. Housing starts increased from a 947,000 annualized pace in March to 1.07 million in April. The 13.2% increase was almost all due to an increase in multifamily construction as condominiums and apartment building starts jumped to 423,000 in April from 303,000 in March. Single-family construction continues to be held back as housing prices remain elevated.

The increase in multifamily construction highlights the post-crisis trend of construction aimed at meeting demand for rental housing. The trend away from homeownership has been a concern for some time. As a result, there has been a pickup in job and income growth while discussions of loosening credit for home purchases have come to the forefront of debate. This has also brought into question the roles of Fannie Mae and Freddie Mac in terms of the level of homeownership push they should be providing, not to mention their status as government sponsored enterprises.

Confidence among homebuilders fell in May as measured by the NAHB/Wells Fargo Housing Market index. The index fell to 45 from 46 in April while consensus forecasts were calling for an increase to 49. Homebuilder confidence is the weakest it has been since May 2013. NAHB Chief Economist David Crowe found consumer confidence to be the biggest drag on homebuilder confidence stating, “Builders are waiting for consumers to feel more secure about their financial situation.”

Industrial production declined 0.6% in April after a 0.9% increase in March. This came as a surprise as median forecasts were calling for an unchanged reading. The reading confirms the impact harsh weather played on economic data. Manufacturing output decreased 0.4% after back-to-back gains in the preceding months that followed January’s stretch of bitter cold weather. Coupled with the decline in manufacturing was a plunge in utilities as temperatures warmed entering the spring months.

Consumer prices increased 0.3% in April following a 0.2% increase in March. This marked the largest percentage increase since June 2013. Higher costs for gasoline, shelter, and food more than offset a decline in utilities. Also in focus were producer prices which jumped 0.6% in April, the largest gain since September 2012. It is worth noting that the Labor Department refurbished the PPI index at the beginning of the year to include services and construction. Subsequently, PPI readings have been more volatile due to big swings in prices for trade services.

The Thomas Reuters/University of Michigan’s Consumer Sentiment index came out Friday. The index unexpectedly fell from 84.1 in April to 81.8 in May. Rising food and gasoline prices coupled with weak wage growth are seen as the main culprits for the decline.

INFLATION BECOMES THE LATEST TOPIC DU JOUR

Long discussed pricing pressure is beginning to show up in various domestic indices, leading some to believe the Fed will pull its foot off the brakes sooner than anticipated. While inflation is stabilizing, there are few signs that it is accelerating materially, leaving plenty of room for the Fed to maneuver. It will be important to keep an eye on prices going forward, though, as any acceleration could alter the investment and economic landscape quickly.

Last week, we learned the consumer price index increased 0.3% in April, the highest monthly increase since last summer. Food and energy continue to be large culprits, with food prices up 0.4% and energy prices up 0.3%.

Source: Federal Reserve Bank of St. Louis

Underlying the headline numbers, the results did not seem so terrible. Core-CPI, excluding energy and food prices, was higher by 0.2% in April and only up 1.8% in the past year. However, important CPI components such as shelter are showing a very clear trend. Shelter is roughly 30% of CPI and in the past 12 months, it is up more than 2.5%. This is a stark contrast to the deflationary scenario seen in late 2010, and has gradually risen for the past several years. With home supply tight and rental markets heating up, shelter costs are expected to remain on an uptrend.

Source: Federal Reserve Bank of St. Louis

For individuals, the most important inflation may be wages and the good news is that wages are ticking higher. It has been some time since wages rose with any sustainability, and follow through on wages will naturally spill over into other areas of the economy as spending power reemerges. The Bureau of Labor Statistics indicated that weekly wages were up 3% over the past year during the first quarter. Between 2001 and 2014, that figure averaged just under 2.5%, and for many of the post-recession years, it was well below the average.

Source: BusinessWeek

Strategists are closely watching trends in inflation to see if policies from the Federal Reserve are finally beginning to filter through to the everyday economy. A great deal of concern resides around the possibility of inflation spiking in the years ahead, but until we see sustained growth in wages, broad based inflation is likely to be some time away. More likely is a gradual reacceleration of inflation that could pick up pace in one to two years, barring any unforeseen setbacks.

THE WEEK AHEAD

Further insight into the housing market will be provided this week with new and existing home sales data coming out. The Leading Economic Indicators index also comes out mid-week.

Central bank activity is limited this week with Japan, Turkey, and South Africa scheduled to release updated policy decisions. The Bank of Japan’s (BoJ) policy decision will be heavily watched as BoJ officials have voiced concern over El Nino’s potential impact on consumer sentiment and spending.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value