Helping Clients Hedge Market Risk: Four Important Considerations

The S&P 500 was up 32% last year and recently reached a new all-time high. Since the March 2009 lows, the market is up 180%. Despite this impressive rally, both institutional and retail advisors must contemplate how to protect client portfolio wealth as many sources of uncertainty remain. The risk environment has changed over the past several years. Banks can create instability, government debt is no longer seen as risk free, the China growth miracle is in question, and Central Banks are actively influencing the prices of assets. This is not your father’s market.

Because of these risks, hedging remains important. History has proven that once a market has experienced a significant decline, hedging strategies can become prohibitively expensive. But even stable, upward trending markets can present challenges to investors looking to hedge. While insurance is typically not expensive in bull markets, the opportunity cost of hedging can be high. When markets experience few down turns (as in 2012 and 2013), spending money on hedging can add up, creating performance drag.

Together, the environment for global market risk and the costs to hedging pose challenges for advisors seeking to preserve wealth for their clients. Fortunately, there are now many alternatives available to protect equity portfolios. Among these new products, the biggest advancements have come through the huge growth in the market for exchange traded funds. Launched as vehicles to trade an equity portfolio as a liquid basket, ETFs now cover the gamut of asset classes (credit, FX, rates, commodities) and geographies (Mexico, Europe, Japan, Brazil, etc.). In addition, theme based strategies (water, social media, infrastructure, and clean energy) are now common. There are even ETFs based on the level of market volatility.

Overall, the growth in the ETF market presents advisors with a broader menu of hedging products. This is good news, yet, this innovation poses challenges. All too often, products are employed without sufficient understanding of the costs and risks that they carry. Hedging is important and advisors must be well educated on the products they may need to utilize to protect wealth. In this short note, we highlight some of the common pitfalls we observe in order to better equip advisors during the next downturn. While hedging can be complicated, we offer the following 4 guidelines.

1. Know the Product

2. Know the Payoff Profile

3. Be Wary of Back tests

4. Hedge When you can, Not When You Have to

KNOW THE PRODUCT

What if we told you, there was an ETF that had this statement in its disclaimer:

“The long term expected value of your ETNs is zero. If you hold your ETNs as a long term investment, it is likely that you will lose all or a substantial portion of your investment.”

What if we next told you that this ETF traded on average 10mln shares per day? Meet the TVIX, an ETF created in 2012 to deliver 2x the daily performance of the VXX, itself an ETF based on market volatility. We are skeptical that investors using the TVIX and products like it are sufficiently well versed in the factors that drive its performance.

Over the past few years, a litany of products has emerged: Inverse funds, double inverse ETF’s, funds that track volatility, funds that seek to provide overwriting strategies, etc. These products, often with hidden fees, obscure costs, and complex risks can have adverse and unpredictable impact on a portfolio.

Perhaps no product is more misunderstood than the ETF on volatility. Launched in 2009, the VXX was the first ETF based on a mechanical strategy utilizing VIX futures. Investors flocked to the VXX as a means of gaining long exposure to market volatility during a period when the VIX was quite elevated. Eventually, however, VXX holders noticed that during certain periods in 2009 and 2010, while the VIX spot price remained unchanged, the VXX position deteriorated by ~10-20% per month. This disconnect, implied in the foreboding TVIX prospectus, is the result of the high "roll cost" associated with the strategy employed by the VXX and other ETFs. These vehicles pursue a strategy that requires futures contracts to be rolled each month that they expire. This strategy is costly when the “term structure” of implied volatility is upward sloping (meaning longer term VIX futures are higher than the VIX itself). This cost does not imply that the VXX is a bad product, but it does illustrate that multiple factors must be considered before utilizing a product.

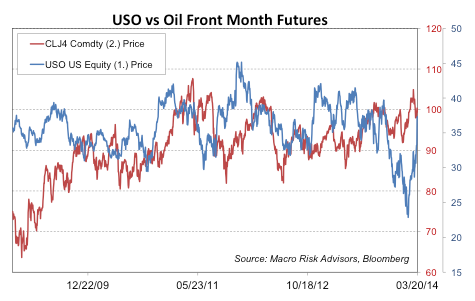

In the commodity space, ETFs seeking to provide exposure to a specific underlying have also run into similar costs associated with rolling futures. For example, the USO seeks to track the daily movement of the price of oil through the futures market. By doing so, the USO avoids delivery of the physical commodity. Critically, a price discrepancy exists between the first and second month futures contract that will cause the price of the USO to track lower (contango) or higher (backwardation) relative to the underlying commodity. The point, again, is that the USO is not a pure play on the spot price of oil. Its performance is also impacted by the shape of the oil futures curve. Below we show a graph of the relative performance of the USO and oil front month futures contract:

(Image shows USO compared to the nearest future contract…correlation varies between 80-95% over a two year period)

UNDERSTAND THE PAYOFF PROFILE

The payoff profile of cash equities is simple. If you buy X for $50, you have $50 at risk and an unlimited reward. Investing using cash equities is straightforward. Confusion sets in when advisors employ options to enhance their clients’ risk/return profile.

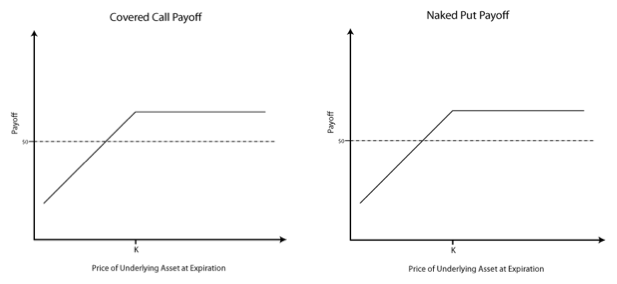

One example of this confusion is a covered call position, where you take 100 shares of a stock and sell a call option against it. The call option provides the seller with instant income (the option premium), while the stock’s returns are capped at whatever strike the call is sold at. At the same time, losses on the downside in the equity are slightly cushioned from the option premium received. As a result, covered call writing is typically characterized as a more defensive strategy for owning equities.

A second strategy is selling a naked put. Typically characterized as “picking up nickels in front of a steamroller”, the naked put generates option premium but is vulnerable to a big sell-off in the stock. Many investors simply say, “I would never sell a naked put”. The aversion to the risk often appears dogmatic, implying that the strategy is simply an accident waiting to happen. It turns out, however, that the naked put seller and call overwriter have a great deal in common. In fact, they share the same risk profile: capped upside, unlimited downside, as we show below in the payoff of the two strategies.

Given the identical charts above, it is unfortunate and confusing that the two strategies are characterized very differently. Despite being considered a “safe” position, the call overwrite has the exact same payout profile of the “risky” naked put sale.

We often see strategies being marketed that appear far better than they actually are. Classic examples are the “reverse convertible bond”. Hardly a bond at all, the reverse convertible is simply the combination of a long position in stock with a short call option. The premium for the call option is recast as coupon income, enticing to investors in today’s low yield environment. Here is a story published on Bloomberg that details losses investors suffered in 2012 as the price of AAPL sold off. There is no free money in the market, and advisors must approach strategies like reverse convertibles which appear to provide excess yield with a great deal of caution. Understanding payoff profiles is critical.

BE WARY OF BACK TESTS!

Mark Twain said there are “Lies, damned lies, and statistics.” Perhaps he was referring to the Wall Street back test. A common method used to test an investment product or idea, back testing can help advisors understand how a strategy performed over various market conditions. Yet, back tests, like statistics, can be shown to prove almost anything. They are teased, massaged, and retrofitted to demonstrate a degree of alpha in a strategy that simply does not exist. In the words of Josh Diedesch of CALSTRS, “You never see a bad back-test. Ever. In any strategy.” A back test will only show you what the results were for that market, but will very rarely carry enough weight to put the results to use in current market conditions.

The overpromise that comes via back testing is nicely captured in Barron’s in a chart displaying ETF performance pre and post creation. Many ETF creators have been back-fitting strategies that have worked well in the past, but once a new ETF is launched, only 51% outperform the broad US market. Incredibly, Barron’s calculates that the average annualized excess return for this series of ETFs is 10.3% in the 5 years before inception, but actually -1% in the 5 years afterward! This chart should make us all skeptical about the value of back tests.

EMBRACE THE NFL

NFL means “no free lunch.” A saying we all know in finance that means you get what you pay for. There is far too much over-promising in our industry, as evidenced by how every advisor has one client who wants the impossible— “I want leveraged upside, hedged downside, and I don’t want to pay for it!” Beyond this farfetched, albeit hypothetical example, advisors find themselves at a difficult crossroad—remain fixated on a return target, or risk underperforming the benchmark and losing money on hedging. This is especially true in the low interest rate environment of the past several years.

There is no easy solution here and advisors must embrace hedging with intellectual honesty. Hedging is costly and a portfolio that is more hedged will underperform in rising market conditions as in 2012 and 2013. From the advisor’s perspective, the key is clear communication with clients around financial objectives and the risk/reward characteristics of portfolios. Once this dialogue is established, we believe the advisor is in a substantially better position to educate clients around the costs and benefits of hedging.

At Macro Risk Advisors, we encourage investors to “hedge when you can, not when you have to.” By this we mean that the when markets are quiet, hedging is like “buying flood insurance in a drought”. But when markets suddenly become uncertain, the cost can become prohibitive when you need it most. And counter intuitively, it is often most profitable to sell options when there is time of great fear. Today’s quiet markets argue for advisors working with clients to develop a preparedness plan for the next financial storm.