US Regional Banks’ Attractiveness Jumps in June1

Market Sector Overview

Data as of June 2, 2014

|

Sector2 |

Aggregate Market Cap3 |

No. of Companies |

No. of VS10 Companies4 |

No. of VS1 Companies |

Bull/Bear Score5 |

|

Utilities |

748,104 |

94 |

27 |

2 |

27% |

|

Financial Services |

5,311,530 |

588 |

141 |

5 |

23% |

|

Real Estate |

803,004 |

198 |

28 |

3 |

13% |

|

Energy |

4,134,646 |

240 |

40 |

10 |

13% |

|

Communication Services |

1,579,906 |

76 |

13 |

7 |

8% |

|

Consumer Defensive |

2,474,421 |

159 |

5 |

3 |

1% |

|

Basic Materials |

1,230,396 |

195 |

11 |

12 |

-1% |

|

Industrials |

3,070,745 |

480 |

14 |

19 |

-1% |

|

Consumer Cyclical |

3,187,658 |

461 |

13 |

30 |

-4% |

|

Technology |

4,564,801 |

521 |

5 |

110 |

-20% |

|

Healthcare |

3,524,317 |

347 |

2 |

147 |

-42% |

|

Total |

30,629,529 |

3,359 |

299 |

348 |

-1% |

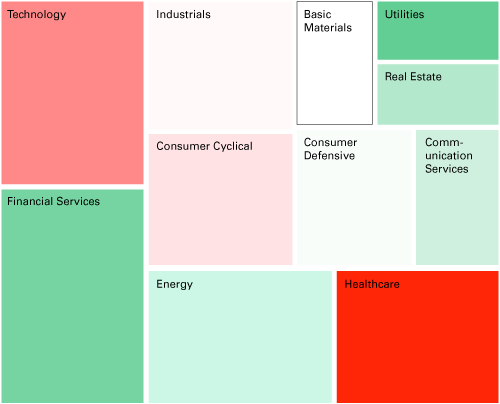

Our Sector-level heat map looks much the same as it did last month, save for the fact that the shade of green has deepened for the Utilities and Financial Services sectors—indicating a larger number of companies screening undervalued according to YCharts Value Score.

We will take a closer look at Financial Services for our bullish sector overview this month, since the data has an interesting story to tell there. In short, it looks to us as though positive quarterly results for regional banks have not yet been fully priced into the market. See the next section for more details.

The Healthcare Sector continues to be the most overvalued in the N. American market—thanks to the ongoing saga of overvalued biotech firms—but statistically it has not changed a great deal from last month to this. The picture is more interesting in the Technology sector because of a large drop in the number of companies screening as overvalued. Could it be that momentum has begun to shift in Tech? We turn to that sector in the last section of this article.

Top Bullish Opportunities: Financial Services

|

Industry |

Aggregate Market Cap |

No. of Companies |

No. of VS10 Companies |

No. of VS1 Companies |

Bull/Bear Score |

|

Banks - Global |

1,917,873 |

19 |

10 |

- |

53% |

|

Banks - Regional - Latin America |

234,314 |

13 |

6 |

- |

46% |

|

Asset Management |

400,759 |

74 |

29 |

1 |

38% |

|

Insurance - Reinsurance |

40,735 |

10 |

3 |

- |

30% |

|

Specialty Finance |

42,268 |

21 |

7 |

1 |

29% |

|

Insurance - Property & Casualty |

248,238 |

47 |

13 |

- |

28% |

|

Insurance - Diversified |

517,020 |

15 |

4 |

- |

27% |

|

Credit Services |

456,466 |

33 |

8 |

- |

24% |

|

Banks - Regional - US |

453,480 |

230 |

49 |

- |

21% |

|

Insurance - Specialty |

28,147 |

10 |

2 |

- |

20% |

|

Savings & Cooperative Banks |

39,839 |

46 |

9 |

1 |

17% |

|

Insurance - Life |

296,170 |

22 |

1 |

- |

5% |

|

Banks - Regional - Asia |

107,867 |

5 |

- |

- |

0% |

|

Banks - Regional - Europe |

135,162 |

2 |

- |

- |

0% |

|

Capital Markets |

254,995 |

25 |

- |

- |

0% |

|

Financial Exchanges |

58,202 |

5 |

- |

- |

0% |

|

Insurance Brokers |

79,995 |

11 |

- |

2 |

-18% |

|

Total |

5,311,530 |

588 |

141 |

5 |

23% |

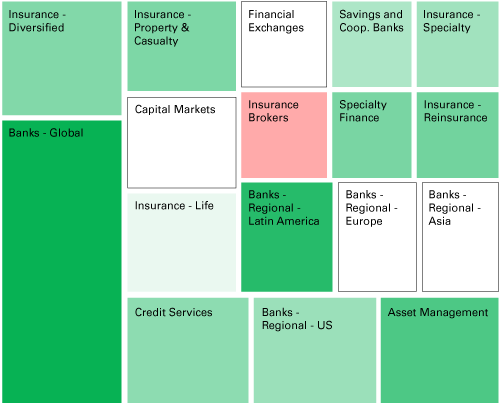

The first thing to catch our attention when we crunched the numbers this month was the large increase in the number of Financial Services companies screening as undervalued compared to last month. At the start of May, 102 Financial Services firms screened as VS10; at the start of May, this figure increased to 141 firms—a material increase of nearly 40%.

Looking closer, we noticed that the biggest month-over-month winner for VS10 count was the US Regional Bank industry. 49 regional banks are now screening as attractive, whereas only 17 did last month—by far the biggest single industry change.

The price of the SPDR S&P Regional Banking ETF KRE was flat for the month of May, implying that the greater number of VS10s this month from last are likely due mainly to operational improvements (e.g., better TTM earnings and cash flow). Our hypothesis is that better quarterly earnings at regional banks have not been fully priced into the market yet, leading to what may be an attractive investment opportunity.

YCharts Pro subscribers can click this link for a list of all US regional banks trading in VS10 territory at present. Non-subscribers who would like this list are encouraged to contact the report’s author.

Top Bearish Opportunities: Technology

|

Industry |

Aggregate Market Cap |

No. of Companies |

No. of VS10 Companies |

No. of VS1 Companies |

Bull/Bear Score |

|

Software - Application |

409,079 |

116 |

- |

44 |

-38% |

|

Semiconductor Memory |

33,129 |

3 |

- |

1 |

-33% |

|

Internet Content & Information |

755,137 |

40 |

- |

12 |

-30% |

|

Software - Infrastructure |

634,342 |

23 |

- |

6 |

-26% |

|

Computer Systems |

87,348 |

16 |

1 |

5 |

-25% |

|

Communication Equipment |

431,104 |

50 |

- |

12 |

-24% |

|

Semiconductor Equipment & Mat’ls |

123,308 |

34 |

- |

7 |

-21% |

|

Semiconductors |

568,156 |

75 |

1 |

13 |

-16% |

|

Solar |

18,829 |

7 |

- |

1 |

-14% |

|

Health Information Services |

31,830 |

9 |

- |

1 |

-11% |

|

Data Storage |

139,689 |

11 |

- |

1 |

-9% |

|

Electronic Components |

93,539 |

30 |

1 |

3 |

-7% |

|

Information Technology Services |

459,877 |

36 |

1 |

3 |

-6% |

|

Computer Distribution |

9,757 |

5 |

- |

- |

0% |

|

Consumer Electronics |

638,281 |

12 |

- |

- |

0% |

|

Contract Manufacturers |

16,358 |

9 |

- |

- |

0% |

|

Electronic Gaming & Multimedia |

39,028 |

11 |

1 |

1 |

0% |

|

Electronics Distribution |

17,661 |

6 |

- |

- |

0% |

|

Scientific & Technical Instruments |

58,350 |

28 |

- |

- |

0% |

|

Total |

4,564,801 |

521 |

5 |

110 |

-20% |

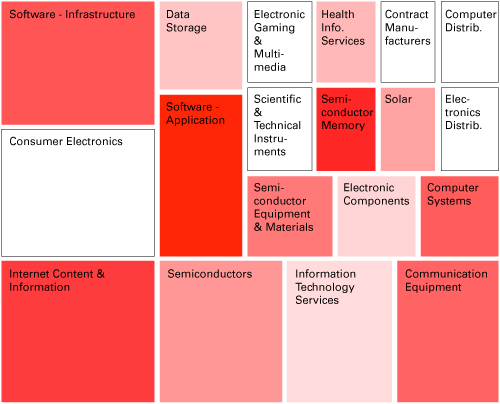

The second thing to catch our attention while perusing the data was the fact that the Bull/Bear Score for the Technology sector had improved by a material amount—eight percentage points—in the space of just one month. Having seen Groupon GRPN loose a fifth of its value in a single day, and knowing that other momentum stocks had also been hit hard, we assumed that the tide was finally turning for the frothy Tech sector. However, as we dug deeper, we realized that the story was more complex.

For example, the application software industry was a group in particular to show a significant change in stocks screening as VS1 from May to June. No less than 21 application software stocks that had been in May’s VS1 list dropped out when we screened this month. However, just over one-third of these stocks left the VS1 group due to improvements in operational performance reported in May rather than to stock price drops.

What’s more, the stocks that moved out of VS1 territory due operational improvements tended to be the most important, largest capitalization ones such as Adobe ADBE (VS2) and Autodesk ADSK (VS2). The stocks that suffered the largest drops were less important companies such as Interactive Intelligence ININ (-20.3% during May) and NQ Mobile NQ (-38.3% during May).

Investors looking for bearish Tech exposure still have plenty from which to choose. LinkedIn LNKD, Workday WDAY, and Electronic Arts EA are all well-known Tech firms trading in VS1 territory again this month. And Groupon? Even after losing a fifth of its value, its poor operational performance means that it is still screening as a VS1 stock at the start of June.

_____________________

NOTES:

1. The YCharts 10% Sector Report is designed to do three things:

a. Show the relative valuation of all U.S. market sectors at the start of each month,

b. Highlight the most and least attractive industries in the most over- and under-valued sectors,

c. Provide a summary of notable stocks in both the VS10 and VS1 deciles (see Note 4 for an explanation of the deciles)

2. We use Morningstar sector classifications.

3. Our market cap figure includes the companies of large capitalization foreign stocks that are listed on U.S. Exchanges. These companies are excluded from the S&P 500, the U.S. Russell Indices, and the Wilshire Index, so the aggregate market capitalizations for these indices are materially less than the total listed here.

4. The Value Score is a quantitative six-factor model designed to separate companies according to their relative (rather than absolute) valuation; companies with a Value Score of 10 (“VS10”—the most undervalued decile) have historically performed much better than the S&P 500 index, and those with a Value Score of 1 (“VS1”) have historically performed worse. YCharts Value Scores are calculated for all stocks within the YCharts data universe that have a market cap above 100M and share price greater than $5. We further limit the universe for the purposes of this report. As such, even though the Value Score framework is based on equally-sized deciles, the total number of VS10 stocks may not equal the total number of VS1 stocks.

5. The formula we use is:

|

Bull/Bear Score |

= |

No. of VS10 Companies in a group – No. of VS1 Companies in a group |

|

Total Number of Companies in a group |

This is meant to identify groups (i.e., sectors or industries) that have a large absolute difference between overvalued and undervalued firms regardless of the component firms’ market capitalization weighting.