Ade Odunsi is the Managing Director for Treesdale Partners and portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE).

With recent sharp falls in the price volatility of a wide range of assets including gold and the markets’ apparent insensitivity to macroeconomic news, many gold investors have shifted focus to some of the more widely watched gold technical indicators to see if they provide insight into the future direction of the gold price. In this week’s short discussion piece we look at the Gold Forward Offered Rate (GOFO), the US inflation adjusted (real) interest rate and the Gold/S&P500 ratio.

1. GOFO has turned positive again after spending much of April and May in negative territory.

GOFO (Gold Forward Offered Rate) is an actively traded rate in gold markets being the rate at which a participant can borrow gold in exchange for posting US dollar collateral. GOFO in essence reflects the total cost of carry of gold (technically it is the USD Funding Rate less the Gold Lease Rate) and given that it’s components are generally ‘non-negative’, it is uncommon for GOFO to turn negative. In a prior commentary we discussed a potential explanation for negative GOFO rates whereby there is a rise in demand for physical gold related to settling gold futures contracts and this is coupled with an environment where the supply of physical gold has dropped. When this imbalance has arisen in the past GOFO has occasionally become negative with an investor being able to earn carry to own gold and this has generally been supportive for the spot price of gold. After spending much of April and May in negative territory, GOFO has turned positive again indicating that spot gold prices are lower than the price of gold for future delivery. The absolute level of GOFO remains extremely low at 0.05% per annum but the switch in direction from negative to positive is perhaps indicative of the so-called ‘convenience yield’ for gold where investors have a preference for physical over future delivery, moving back towards a neutral level.

Source: Bloomberg LP; Treesdale Partners calculations

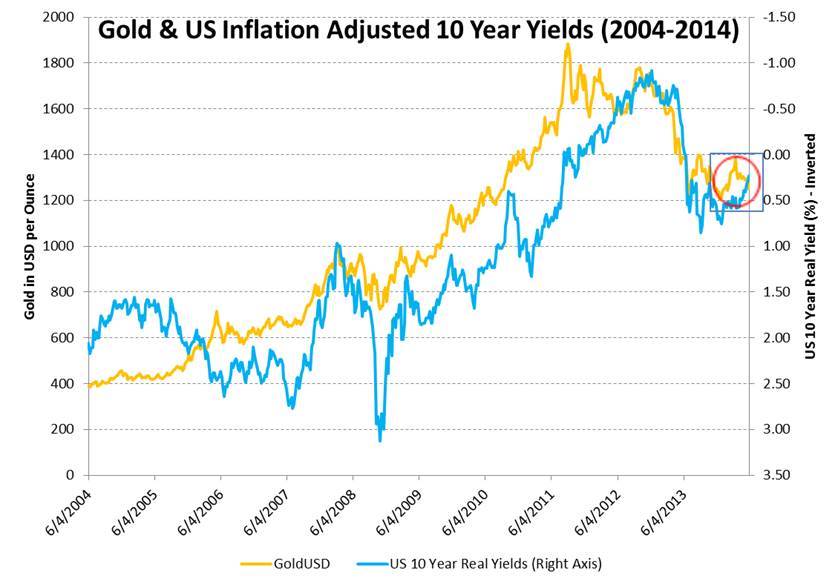

2. Very recent divergence between gold and the ten year US real yield.

Source: Bloomberg LP; Treesdale Partners calculations

Past performance is not indicative of future results.

Perhaps one of the strongest gold indicators to watch has been the US real interest rate (the US interest rate less inflation rate). The chart above shows the relationship between gold and the 10 year real interest rate over the last ten years. Note that the interest rate axis has been inverted to reflect that lower US real yields are generally associated with high gold prices. Over the last month there has been a discernible divergence between the gold price and the real interest rate (the chart below shows the divergence more clearly) with gold prices moving lower despite much lower real interest rates. For the relationship to move back into line either the real interest rate will need to rise (become more positive) or the gold price should stabilize and move higher. Should the recent drop in US real interest rates be sustained we would expect the price of gold to find support at current levels.

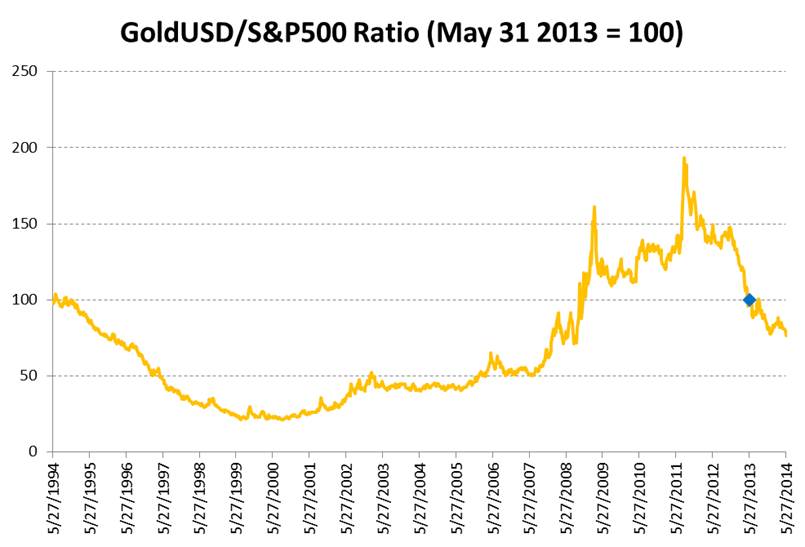

3. The Gold price in USD as a ratio of S&P500 has fallen dramatically over the last two years.

Source: Bloomberg LP; Treesdale Partners calculations

This indicator has met the perfect storm of lower gold prices and the S&P500 more than doubling since its trough in 2009. In essence it gives a measure of the value of the US stock market in gold terms and shows that gold has dropped in value precipitously relative to the stock market. We should note that the absolute level of the indicator has no meaning but rather the indicator should be looked at on a relative basis, to its history. While the recent moves have been large, looking back over a 20 year history does not suggest that the relative value of gold to the stock market has moved to either extreme.

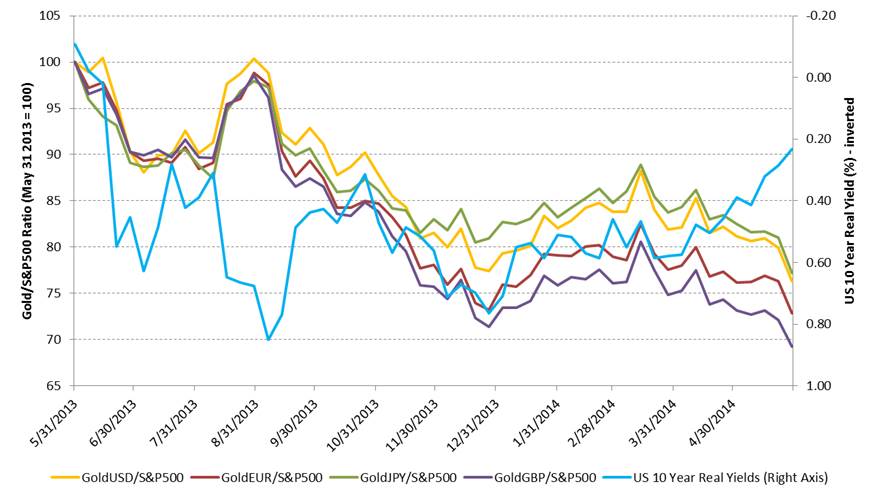

Finally In the chart below we also plot the value of gold in dollars, euro, yen and pounds relative to the S&P500. The chart covers a 1 year historical period and sets all the gold/equity ratios to 100 on May 31 2013 so that the two charts may be compared directly. As we stress above the absolute level of the indicators have no meaning but rather we wish to compare the relative change in each gold price versus the S&P 500 to get a comparative measure of how they have each performed relative to the equity market. Starting at an indicator value of 100 on May 31 2013 we see that gold in pounds and gold in euro have suffered the largest falls in value relative to the equity market but that the overall trend has been similar for gold priced in each of the four currencies. In the chart we have also shown the US 10 year real interest rate (inverted) which more clearly shows the very recent divergence between the gold price (in all currencies) and the real interest rate.

In summary, the move in GOFO back to positive territory is perhaps indicative of the upwards pressure on the ‘convenience yield’ for gold abating and therefore suggesting reduced support for spot gold. There has been a recent pronounced diversion between the price of gold and US real interest rates but it is unclear at this stage how this divergence might be resolved. Should recent the fall in US interest rates be sustained support for the gold price would be expected to emerge at current levels. On a relative value basis the price of gold relative to the S&P 500 has fallen dramatically over the last two years, most notably versus the gold price in euro and the gold price in pounds. We note however that on a longer term view the gold/equity ratio does not appear to be at extreme levels in either direction.

Value of gold in dollars, euro, yen & pounds

relative to the S&P500

Source: Bloomberg LP; Treesdale Partners calculations

Past performance is not indicative of future results.