Stocks Decline on Geopolitical Risk

Equity markets trended lower on the week, after geopolitical risks increased and economic data was mixed. The S&P 500 lost 0.7% and the Dow Jones Industrial Average fell 0.9%.

Tensions in the Middle East quickly rose to the top of the newswires last week, as the situation in Iraq turned markedly more volatile. From an investment perspective, tensions throughout the region are pushing oil prices higher, and leaving the cost for a barrel of oil at more than $113. At that cost, oil prices could begin to affect consumer psyche during the summer driving season, and we are already seeing some portions of the country reporting per gallon gas prices above $4.

Source: GasyBuddy.com

The good news so far is that higher oil prices have not had an impact on consumers. In May, retail spending was up 0.3%, while April was revised higher to 0.5%. Expectations were for a 0.6% gain in May, so the released figure was slightly disappointing, and much of the gain last month was the result of higher auto sales. When coupled with the upwardly revised numbers from April, though, the trend in consumer spending is more positive than not.

Source: Econoday

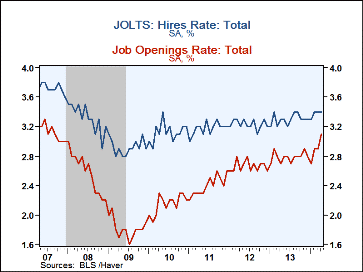

One reason behind the more optimistic behavior of consumers has been improvements in labor markets. The recently released Job Openings and Labor Turnover (JOLTS) report for April showed 4.455 million job openings in the month, up sharply from March. A measure of activity within

labor markets is the job separations rate, which occurs due to layoffs, resignations, or retirement. Job separations stayed static at 3.3%, indicating that activity was similar to prior months, but the actual number of separations increased more than 5% in the past year.

Source: Haver Analytics

Despite the stabilization in labor markets, consumers were slightly apprehensive based on a lower than anticipated reading in the consumer sentiment index. Slightly surprisingly, consumers revealed that they were more optimistic about the current economic conditions, but less so about the future outlook, and that was the reason for softening in the headline figure.

Oil Spikes on Iraqi Strife

Of the many global macroeconomic concerns of the past few years, oil has curiously fallen down the list in terms of major areas of investor focus. After recovering in the wake of the financial crisis, the commodity has generally been range bound between $100 and $120 a barrel. Newfound supply of natural gas in the United States has also eased concern about the domestic economy’s reliance on oil imports from the Middle East.

But with market stress at very benign levels (exemplified by the VIX falling below 11 for the first time since 2007), last week’s flare up in Iraq has brought oil back to the front pages. According to the Wall Street Journal, oil futures experienced their biggest weekly gain since December last week, with Brent crude for July delivery hitting $113.41 a barrel.

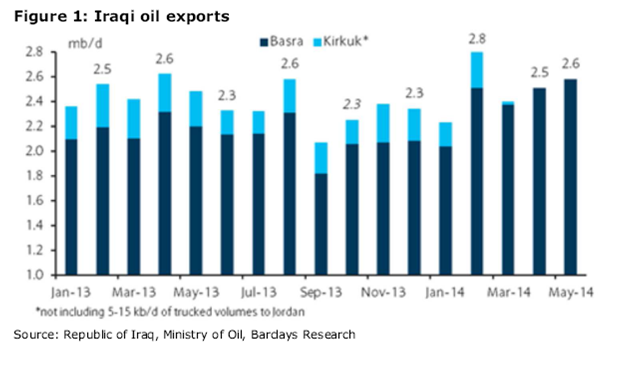

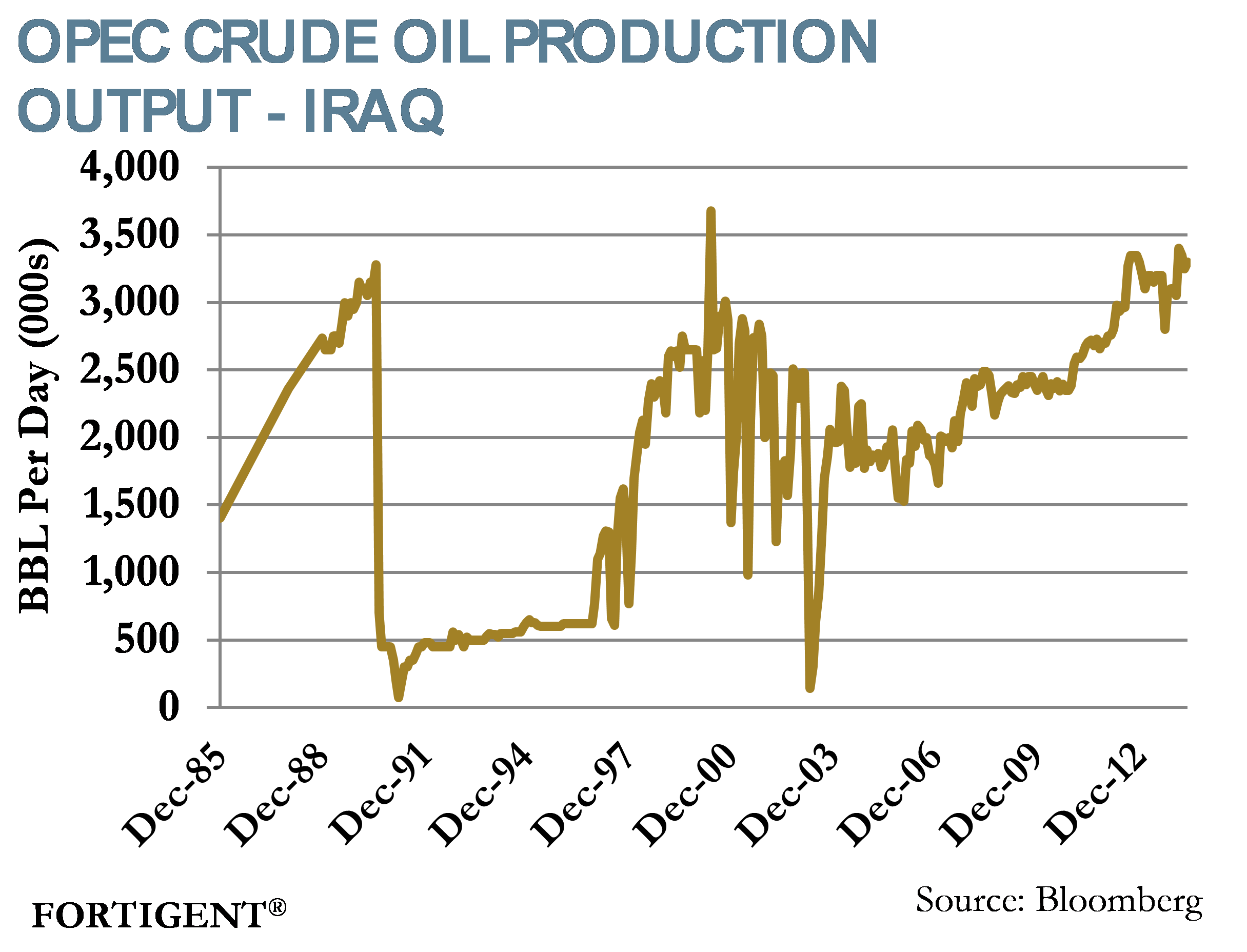

While oil prices still sit within the band of trading experienced over the past several years, there are fears that it could move sharply higher. To date, the areas seized by insurgent forces within Iraq do not represent the major hub of oil production in the country. Kurdish fighters took control of the northern oil city of Kirkuk on Thursday, which accounts for a small fraction of total Iraqi oil output. However, a successful push into the southern production center of Basra would create a far more significant disruption to global oil supplies.

Iraq had gradually been raising its production, recently reaching the highest output level since the Iraq War. A disruption of this expected supply would be particularly impactful given already limited production from Libya and Iran, the first due to strife and the latter due to US-imposed sanctions.

As noted by Barclays Research, a significant disruption to Iraq’s oil production would have particularly negative effects for China and India. While Iraq accounts for 3% of global oil supply currently, it makes up 8% of China’s crude imports and 13% of India’s. Those two countries import 60% and 75% of their oil, respectively. Barclays’ economists estimate that every $10 increase in crude cuts 0.2% from China’s GDP.

At this stage, booming US energy production will do little to alleviate the global price of oil, given the current US ban against oil exports. This dynamic may cause further economic divergence between the US and the rest of the world that has taken root over the past year. Despite the calm with which equity markets have absorbed macro event after event, investors would be wise to keep a close eye on how the global energy landscape evolves this year; it may just be the negative catalyst that causes a long-anticipated correction in risk assets.

The Week Ahead

Headlines will continue to be dominated by the situation in the Middle East, but several pieces of economic news will also garner attention.

In the US, the Federal Reserve holds its regularly scheduled policy meeting this week, with an expectation that asset purchases will be reduced by a further $10 billion per month.

Other data to watch in the US includes industrial production, consumer price index, homebuilder sentiment, and May housing starts.

Overseas markets will focus in on monetary policy decisions in Russia, Philippines, Colombia, and Thailand.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value