By: Heather Rupp, CFA, Director of Research for Peritus Asset Management, the sub-advisor to the AdvisorShares Peritus High Yield ETF (HYLD)

A strategy that we have seen emerge over the past year within the high yield market has been “hedged high yield,” most recently with iShares rolling out an product last month that uses their passive, index-based HYG fund as the high yield component. The gist of the hedged high yield strategy is to go long high yield bonds and short Treasuries (or Treasury futures). The basic premise is that the strategy will hedge interest rate risk, with any bond pricing decline due to rising rates being offset with the short in Treasuries. At face value this makes sense, as the adage in fixed income is that prices and yields/rates move in opposite directions, so as interest rates increase, prices decline. However, the problem is that history shows this really isn’t true in the high yield space.

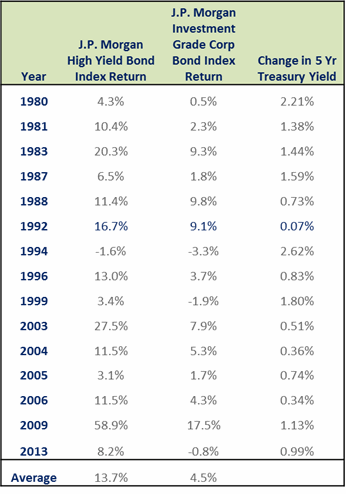

Looking at the historical data, high yield bonds have actually performed very well when interest rates increase. The long-term numbers show that in the 15 yearly periods since 1980 where we saw Treasury yield increases (i.e., interest rates rose), high yield bonds posted an average return of 13.7% (or 10.4% if you exclude the massive performance in 2009). This compares to only a 4.5% average return (or 3.6% excluding 2009) for investment grade bonds over the same period.1

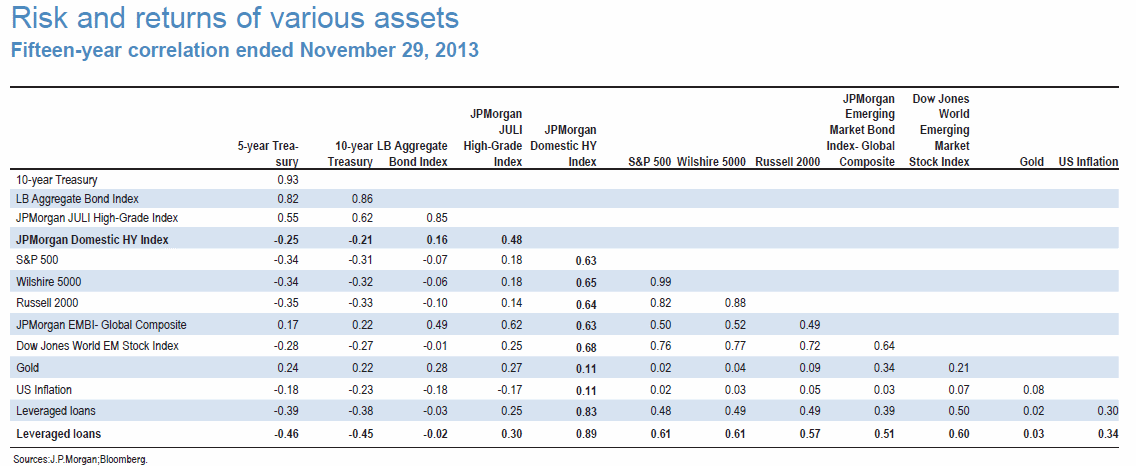

Additionally, Treasuries and high yield bonds actually have a negative correlation.2 This means that as Treasury prices go down due to yields (interest rates) increasing, high yield would theoretically experience the opposite change (increase) in pricing.

So while a short Treasury position may be appropriate to offset your interest rate risk in the investment grade world, where there is a positive correlation with Treasuries, it does not appear appropriate in the high yield space.

Further, we see another big problem with a combined portfolio of being long high yield bonds and short Treasuries: during times of systemic market disruptions we see a “flight to quality” trade, where investors abandon perceived “risky” assets such as high yield bonds and pile into “risk free” Treasuries. So in a situation like this, you would not only be hit on a decline in your high yield bonds as investors sell them, but you would be hit on your short Treasury position as investor flock to these assets and bid up the price of Treasuries. So at face value the “hedge” sounds appealing, but it very well may be far from a hedge depending on the market environment.

Not to mention the fact that so far this year, the short Treasury side has been a losing strategy. Going into 2014, the vast consensus was that rates would definitely be rising in 2014, but so far that certainly has not been the case, meaning in this sort of strategy investors would be taking losses on the short side. Our ultimate belief is that various economic and demographic factors will constrain rates going forward. As we sit here today, we believe that a pure long allocation to high yield is more appropriate.

1 7 Data sourced from: Acciavatti, Peter Tony Linares, Nelson R. Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “2008 High Yield-Annual Review,” J.P. Morgan North American High Yield Research, December 2008, p. 113. “High-Yield Market Monitor,” J.P. Morgan, January 5, 2009, January 5, 2010, January 3, 2011, January 3, 2012, January 2, 2013, and January 2, 2014. 2008-2012 Treasury data sourced from Bloomberg (US Generic Govt 5 Yr), 2013 data from the Federal Reserve website. The J.P. Morgan High Yield bond index is designed to mirror the investible universe of US dollar high-yield corporate debt market, including domestic and international issues. The J.P. Morgan Investment Grade Corporate bond index represents the investment grade US dollar denominated corporate bond market, focusing on bullet maturities paying a non-zero coupon.

2 Acciavatti, Peter, Tony Linares, Nelson R. Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “2013 High Yield-Annual Review,” J.P. Morgan North American High Yield Research, December 23, 2013, p. 296.