The FIFA World Cup and market predictions have in common that we are tempted to create a world of make-believe when it comes to predicting outcomes. While others ponder about the meaning of a round ball, we’ll focus on the implications of a make-believe world comprised of ever-higher asset prices. Our caution: look out below!

Investors have a tendency to ignore the hidden risks in their investments, even if those risks may be hiding in plain sight. You may recall the references to a “goldilocks” economy in the run-up to the 2008 credit crisis. Similarly, in the 1990s, what could possibly go wrong investing in tech stocks? What these episodes have in common is that the downside volatility of asset prices was unusually low. The pessimists warn of pending collapse, yet are ignored.

As an optimist, I agree with the pessimists. Not because I think the world will come to an end, but because the path from euphoric to normal is a rough one. When low asset price volatility lulls investors into believing the markets have become safer than they really are, folks take risks that they are bound to regret. Those that pile into the equity markets on the backdrop of ever shorter corrections, of ever higher asset prices, of historically low volatility, may be running for the exit fast when they realize they had no business being over-exposed to the equity markets in the first place.

Some laugh at gold investors that saw the price of gold drop sharply in 2013. What many fail to realize is that the very same can happen in the equity markets just as easily. When an asset (gold in this case) rises for 12 years in a row, there will be those taking out a loan to invest in the yellow metal. Similarly, investors have taken out ever more debt to buy stocks. For such euphoria to end, we don’t need a crisis, all we need is fear levels to return to “normal.”

Liquidity is dead

The low volatility environment has been accompanied by what is historically low volume. When liquidity in the market is low, it provides fertile ground for more abrupt price moves. One reason why liquidity may be low is due to the Dodd–Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”). Dodd-Frank, with its good intentions, has banished a lot of risk taking by financial institutions. That may be a good thing in some ways, but it has also curtailed major liquidity providers. The next sharp correction in the markets may well be an indication of whether the dearth of market participants is a problem.

Other markets infected

The above symptoms don’t just affect the equity markets. In the fixed-income markets, our analysis shows:

- Volatility has been rather low of late;

- Liquidity is sharply reduced as banks have sharply reduced their trading activities (due to Dodd-Frank);

- Investors chase yield (mostly by chasing “credit”, i.e. lower quality debt instruments; but some also take on more interest rate risk by investing in longer-dated debt securities).

- Investors increasingly embrace what we call creative bond funds that brag about holdings in Master-Limited Partnerships (“MLPs”) and ultimately have big exposure to dividend paying emerging market equity securities.

Currency markets have also experienced extraordinarily low volatility of late. Having said that, we have not seen leverage increase much in this market, as folks abstain rather than take huge positions.

Policy makers concerned

Folks at the Fed have started to talk about complacency, with New York Fed President Dudley saying, “Volatility in the markets is unusually low.” At a dinner of the Hoover Institution I attended, Kansas City Fed President George mentioned in a speech: “The incentives to reach for yield extend to smaller financial institutions as well… If longer-term interest rates were to suddenly move higher, these institutions could face heavy losses.”

Should you be concerned?

If you are not concerned, you are not paying attention. The reason I say this is because when the masses are complacent, it is my assessment that it is prudent to be fearful. The time to prepare for the next correction is now. And you don’t need to think a crash is imminent to endorse the idea that it might be a good idea to rebalance a portfolio when equity securities have taken on a greater portion of one’s portfolio.

Do I think a crash may be coming our way soon? Yes. What can trigger such a crash? Nothing in particular, yet anything can, given the high degree of complacency we see in the markets. Could I be wrong? Certainly.

What can you do about it?

First, if the equity exposure in your portfolio has grown, consider rebalancing in the context of your longer-term goals. This is a prudent exercise no matter what your long-term outlook is. Beyond that, to the extent you want to be invested in equities:

- Consider an enhanced, hedged or market neutral strategy. There are many flavors out there of equity strategies, each of them have their own set of risks and opportunities. You’ll have to do your homework to be comfortable with them.

- There will always be some sector in the market outperforming. Rather than chasing the winners, consider looking at areas that have underperformed.

Even these types of strategies may experience negative returns in a down market, but you may consider yourself a winner with many of these strategies if you lose less than the market.

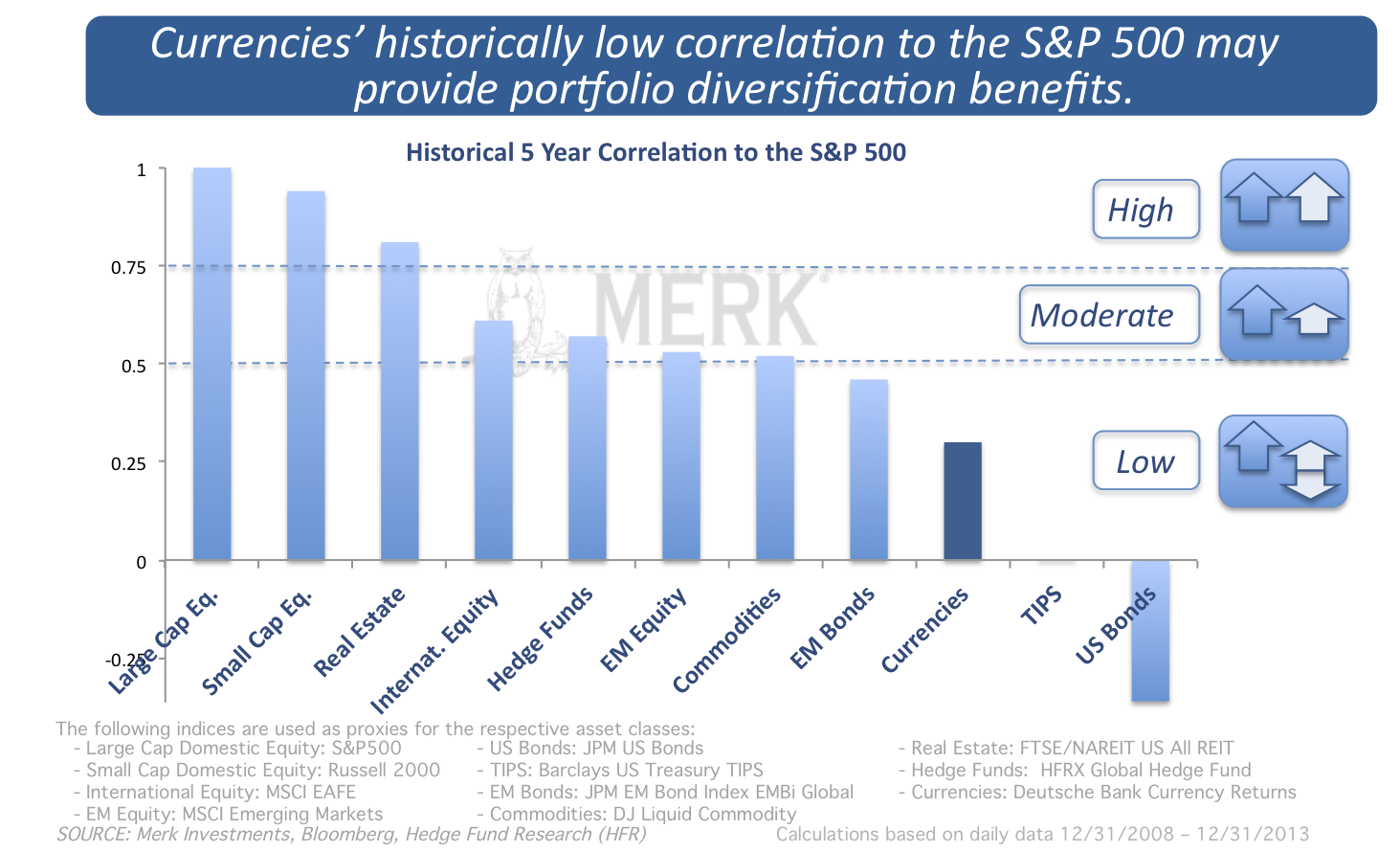

Second, diversify. As already eluded to with the reference to different types of equity strategies, key to thriving when equity returns sour is to have assets that produce a return stream with low or even negative correlation to the equity markets:

As one can see from the illustration, bonds have historically been powerful diversifiers for equity portfolios. Trouble is that investors not only want low correlation, but they also like positive performance. And while bonds have historically done just fine with regard to performance, many investors, including yours truly, aren’t so sure that this will be the case going forward. However, rather than finding an incarnation of a “new generation” fixed income fund that engages in what may be unnecessarily risky bets or masks an emerging market equity strategy as a fixed income play (because those stocks pay a dividend), we prefer to look elsewhere.

As many of our readers know, we have increasingly been looking at gold as a long-term diversifier as we think real interest rates, i.e. interest rates after inflation, may be negative for a long time. Today, we take it a step further, focusing on our currency outlook for the second half of the year. We like the currency market for a couple of reasons, including:

- Historically, exchange rates exhibit low correlation to equity markets; in fact, if one employs an absolute return (long/short) currency strategy, one can design a portfolio that should exhibit low correlation to equities over time. An example I like to cite is that taking a position in the New Zealand Dollar versus the Australian dollar will almost certainly generate returns that are not correlated to how equity prices behave.

- If deployed without leverage, a long/short currency strategy has a risk profile that – in our assessment – makes it a good candidate to be used instead of a bond allocation. While there are bond strategies that have historically had an even lower risk profile, few alternatives offer as compelling a risk profile as currencies.

- The currency market provides unique profit opportunities as many market participants are not seeking to maximize their profits: from corporate hedgers to central banks, even tourists spending money abroad.

U.S.

The U.S. dollar has not been acting as a safe haven currency. Part of it may be because of a lack of leadership. We are not referring to Mr. Obama, but Ms. Yellen. And it’s not personal. The Fed has, in our interpretation, communicated that monetary policy shall be increasingly ad hoc. In fact, the best indicator of where rates will go may be whether the convicted felons that the head of the Federal Reserve profiled in her first public speech have a job by now. I wish this were a joke, but I’m rather serious about it: Yellen has indicated she wants to keep rates low as long as necessary to boost employment as long as inflation does not cause too much of a problem.

Curiously, when inflation numbers come out higher than expected, a currency often appreciates versus its peers, as investors anticipate the central bank will do “the right thing” and raise rates. It’s then, over time, that the currency reflects whether the central bank walks the talk. In the case of the Fed, we don’t think the Fed is likely to walk the talk. As such, we continue our overall negative view with regard to the dollar.

Eurozone

Mr. Draghi, the head of the European Central Bank (ECB) has thrown in all but the kitchen sink in an effort to weaken the euro. It's not working very well. It’s not working very well because negative rates on the deposits at the ECB don’t matter much when there are few deposits. The new initiative, the TLRTO (targeted long-term refinancing operation), while creative and well intended, is unlikely to weaken the euro. What weighs on the euro is that rates are expected to be lower for longer. However, what ultimately matters are real interest rates, not nominal interest rates. And there, we think the U.S. will have lower real interest rates even with the latest efforts of the ECB.

U.K.

The UK has had numerous tailwinds in its economy. Recently, Bank of England (BoE) head Mark Carney told us he was just kidding with his forward guidance that rates will stay low for a long time. He didn’t use exactly these words, but made it clear that a rate hike might come sooner than the market anticipates. One of Carney’s concerns is rising home prices; monetary policy can’t do much there, though, as it is cash payers, including Russian oligarchs, looking for safe haven assets – many of these investors are not particularly sensitive to rise in interest rates.

The main thing going against the sterling is that it has already appreciated quite a bit. Still, in our assessment, Carney is likely to walk the talk, providing support to the sterling in the coming months.

New Zealand & Australia

Talk about walking the talk. Rates are on the rise in New Zealand. Again the only negative is that the New Zealand dollar isn’t cheap. Of late, we had gotten a bit cautious about valuations, especially versus the Australian dollar. However, New Zealand has continued to march ahead, bolstered by a hawkish central bank; in contrast, Australia has continued to lag further behind.

We still think that the Australian dollar will ultimately play catch up (at least a little bit) to the New Zealand dollar.

Talking about Australia, the Australian dollar is “proof” that China is not falling apart. We think positive surprises for the Australian dollar may be triggered by good news out of China.

China

China is one of the most misunderstood places. The volatility in the yuan earlier this year was intentionally introduced by policy makers to put an end to highly levered arbitrage games between the onshore and offshore versions of China’s currency. The unwinding has been the cause for many headlines, including the fallout in the copper market (copper was used as collateral for speculators; except that some of the collateral appears to have been pledged multiple times); another fallout was that economic indicators were useless, as many financial transactions were disguised as real trade to circumvent capital controls.

As the dust settles, higher volatility will teach businesses to put proper hedging techniques in place, forming the basis for a further liberalization of the market.

We are less concerned about the housing bubble in China, notably because consumers rarely take out a loan; and while banks, municipalities and developers may face challenges, the fallout from a housing crash may be more similar to a stock market crash rather than what we experienced in the US as our housing market crashed.

Finally, China has made it a priority to provide small and medium sized enterprises (SMEs) access to credit. A major entrepreneurial boom could be unleashed as the allocation of credit matures.

Japan

While we have a long-term price target of infinity for the Japanese yen, i.e. we don't think the currency will survive, in the short-term, Abenomics has taken a breather. In recent months, we interpreted pricing action in the yen to suggest a failing reform agenda. Of late, however, the yen is failing to rally on occasions where historically it would have.

As such, we think the trend of a weaker yen is likely to resume.

Emerging Markets

Emerging markets in general have had reprieve from quiet global markets. Don’t count on that to continue. India is a bright star in the space, as capital is likely to flow back into India with the new government and a strong central bank in place. Some of that has already happened, but we think the Indian rupee may continue to outperform.

Norway, Sweden, Canada

Norway should raise rates, but will be reluctant. Sweden should lower rates, but will be reluctant. Canada has reached new records in being boring – the currency that is. Various models favor the loonie as a safe haven. Except that I don't trust the calm: if we get volatility emanating from the U.S., we don’t think the loonie can stay out of the fray.

For more, again, make sure to also register for our free Webinar on Tuesday, June 24, at 4:15pm ET. If you find value in our analyses please encourage your friends to sign up for this free newsletter, have them follow me on twitter, and/or post a link to this newsletter on your favorite social media site.

In the context of many disliking China these days, we are increasingly optimistic about the outlook of the renminbi.

Add to that the overall negative sentiment regarding the euro and we think the euro should appreciate versus the greenback for the remainder of the year.

Axel Merk

Axel Merk is President and Chief Investment Officer, Merk Investments,

Manager of the Merk Funds.

This report was prepared by Merk Investments LLC,and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Merk Investments LLC makes no representation regarding the advisability of investing in the products herein. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice and is not intended as an endorsement of any specific investment. The information contained herein is general in nature and is provided solely for educational and informational purposes. The information provided does not constitute legal, financial or tax advice. You should obtain advice specific to your circumstances from your own legal, financial and tax advisors. As with any investment, past performance is no guarantee of future performance.