I spent last week in China, meeting with corporate management teams, government officials and investors in the Chinese markets. One of my motivations for making the trip was to get a better sense of the speed and scope of government reforms. It was a fascinating week, but I can’t say that I came away with sweeping, definitive clarity. While there is growing optimism from local observers about government intent and will, much uncertainty remains. Important tangible steps have actually been taken already and a path to economic sustainability will require significantly more actions. However, a strong desire to maintain high near-term growth levels seems likely to lead to a measured pace of implementation. If there is one simplifying theme, it’s that reforms involving the imposition of power/control (environmental reform and anti-corruption, for example) come more naturally to the government than the relinquishment of control (opening of capital markets and state-owned enterprise (SOE) reform as examples). The most common refrain from all parties to inquiries regarding any challenges in the country is that “the government is well aware of the problem.” However, I remain somewhat skeptical regarding the pace of change dealing with the excesses of China’s credit system, particularly in the face of some weakening in the key real estate markets. There, it seems to me, the hope is to change the slope of the marginal behaviors and to guide a very gradual rebalancing, minimizing any shocks to the already slowing economy.

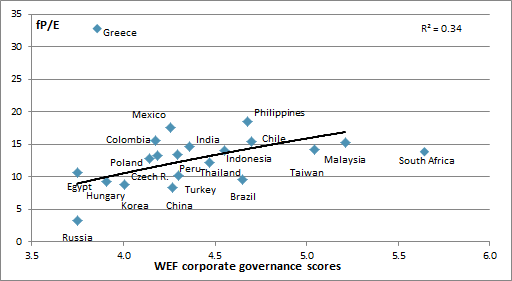

While there may not be complete clarity about the exact shape of reforms, it appears that the market will reward countries which are undertaking positive reforms in governance with higher equity valuations. A UBS study published last week confirmed quantitatively what we have been observing: the value ascribed to positive governance has been rising and stands at eight-year highs. In India, for example, growing excitement regarding the reform agenda of Prime Minister Modi has driven a dramatic revaluation of share prices. Given the number of important elections and proposed reform agendas in play across the emerging world this year and the high stakes of those issues in a low growth world, we continue to be excited about the opportunities to position ahead of positive change where market uncertainty still exists. Indonesia is one such market where we feel like the likelihood of a positive reform cycle is potentially underestimated by the markets.

Exhibit 1: Forward P/E and corporate governance scores in emerging markets

Sources: WEF, Thomson Datastream, MSCI, UBS

That said, as with many issues, the most exciting, under-discovered investment opportunities are often found at a more granular level. I came away from the week in China thinking that corporate level governance reforms may be where many of those undiscovered situations exist. An immersive series of company meetings in the emerging world always serve to remind one of the wide range of corporate governance disciplines there. Convoluted ownership structures and management incentives only vaguely aligned with underlying shareholders are still all too prevalent. These are clear reasons why the aggregate earnings growth and equity market performance in China have not been consistent with the spectacular gross domestic product (GDP) growth figures. However, there are increasing forces that may drive changes at some companies. There are a growing number of firms with thoughtful, world-class governance and significant inside ownership in the emerging markets. Equally important, those companies have clearly delivered strong earnings and garnered significant valuation premiums to their less-well-managed peers. When one considers the increasing need to attract global capital sources, the pressure and incentive to follow their best practices is growing at the margin. Rising cross-border M&A into as well as from the emerging world should also play into this trend. IPOs of new businesses seem to be embracing higher governance standards, raising the national averages. Identifying situations where governance improvements are unappreciated can provide a powerful return tailwind. A company that can take robust aggregate growth in the country and drop it to the bottom line with any degree of operating leverage can generate robust earnings. Doing so in an increasingly shareholder-friendly and transparent manner should result in a growing multiple accorded to those earnings (a potentially powerful combination).

Even in a slowing China, the level of change is amazing, presenting both opportunity and potential disruption. One area where reform is clearly taking shape is the environment. China will continue to burn large quantities of coal for years to come, but significant action is occurring to diversify into natural gas, alternatives, and to burn coal in less polluting/more efficient ways. Interestingly, one of the barriers to really exploiting China’s shale potential is water scarcity. Managing water resources in China will be a massive challenge and spending opportunity in the years to come. In some cases, China has an opportunity to leapfrog the rest of the world on the environment. On electric vehicles, for example, China seems likely to be a global leader in absorption and implementation. It is a high priority for China’s leadership, which is rapidly moving to build the necessary infrastructure and to support the industry with steps such as moving municipal buses to electric. Regarding commodities, there has been a great deal of focus on slowing Chinese demand, but underappreciated may be the ripple effects of closing unprofitable and highly polluting plants producing energy-intensive products such as steel and aluminum. The Chinese consumer’s tastes are also changing at a very rapid pace. Pure materialist consumption is losing share of spend, but cash-rich Chinese families are shifting significant resources into areas such as health (healthier food and beverage, exercise and preventative medicine), travel and private education resources. It is worth remembering that second homes in China are largely forbidden and the vast majority of families have only one child. That leaves wealthier families with a lot of disposable income to direct towards these more experiential purchases. China’s embrace of mobile computing and e-commerce is advancing at a phenomenal pace and some extraordinary local businesses are arising to serve their unique needs.

In the end, I was struck by what a vast landscape the Chinese economy is. The scope and pace of China’s reform will have significant influence on the global economy and should be monitored closely. However, uncertainty about the complete reform picture at a national level should not preclude delving deeper into the potential opportunities at an industry and company level. Many parts of the Chinese economy will continue to grow rapidly. The intersection of that growth with hard-working local talent wrapped in corporate structures that are increasingly aligned with their equity shareholders is well worth pursuing.

Disclosure

The views expressed are as of 6/16/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

International investing involves increased risk and volatility due to potential political and economic instability, currency fluctuations, and differences in financial reporting and accounting standards and oversight. Risks are particularly significant in emerging markets.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

948669