EQUITIES RALLY ON SURPRISE-FREE FED

Equity markets climbed to record highs last week amid an “as expected” FOMC meeting. The S&P 500 rose 1.4% and the Dow Jones Industrial Average gained 1.0%.

The Federal Reserve held its regularly scheduled meeting last week, and equity markets raced to their strongest daily gain of the week after the announcement was released. There were few surprises, as the Fed chose to maintain its course, while painting a cautious economic picture.

At a high level, the Fed chose to reduce its asset purchases by an additional $10 billion, cutting monthly purchases to $35 billion, and maintaining the Fed Funds target at 0 to 0.25%.

Despite moving on an expected course, Fed officials offered somewhat cautious guidance, reducing expectations of GDP, and increasing inflation projections slightly.

Officials also inched up expectations of the Fed Funds Rate. Whereas previous expectations were for a 1.0% Fed Funds Rate in 2015 and 2.25% in 2016, that has now increased to 1.13% and 2.5%, respectively.

Source: Econoday

There continues to be a great deal of uncertainty around the timing of the first interest rate hike, but it appears more likely than not that rates will begin moving up in the next two years. Rising inflation pressure could become a concern for the Fed despite ongoing slack in labor markets. A growing number of economists are suggesting that slack in labor markets is less than believed, and inflationary pressure could quickly transition towards faster wage growth.

Market participants might disagree with the Fed, however, as bond markets rallied, stocks moved higher and the dollar weakened. Markets were likely expecting the Fed to express greater concern about pricing pressure, and were somewhat surprised about the lack of concern.

It was a mixed week of economic data, but by most accounts the US economy does seem to be shaking off the winter months’ sluggishness.

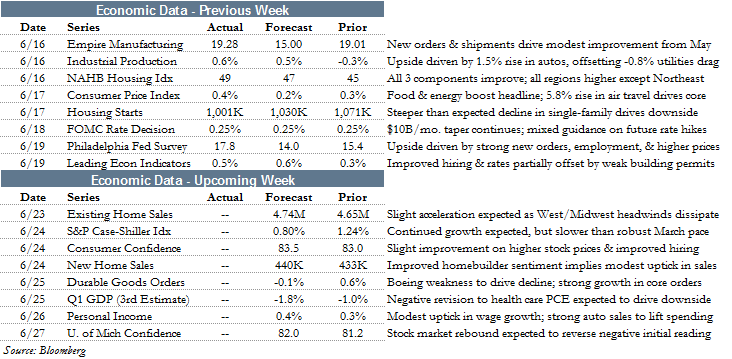

Industrial production rebounded from an April decline to expand 0.6% in May. This gain was aided by a revised April decline of just 0.3%, relative to the initially reported 0.6% contraction. Manufacturing helped fuel the increase, also up 0.6% in the month, while the mining component rose 1.3%. Utilities fell for the second straight month, shrinking 0.8%. Overall, this was a positive report for the US manufacturing sector and boosts hopes for a rebound in second quarter GDP.

The manufacturing sector received further good news in the form of the Empire State Manufacturing and Philadelphia Fed Business Outlook surveys, which both posted surprise gains for June. The Empire State report edged up slightly to 19.28, despite expectations for a four-point decline. The Philly Fed measure likewise rose from 15.4 to 17.8. Encouragingly, both reports were boosted by very strong new orders data, which generally is a better sign of sustainable growth.

Consumer inflation also signaled that growth is accelerating, as the measure came in unexpectedly high in May. Month-over-month, headline CPI rose 0.4% - twice the consensus forecast. On a year-over-year basis, consumer inflation increased 2.1%, the highest level since 2012.

Food and energy helped lift the headline measure, but core inflation was also higher than expected. As noted by Econoday, May’s core CPI month-over-month increase of 0.3% was the highest since August 2011.

The primary source of negative news last week was in the housing sector, as housing starts posted a deeper than expected decline in May. The Census Bureau reported that starts slowed to a seasonally adjusted annual rate (SAAR) of 1.001 million. That is 70,000 lower than the prior month and 35,000 below expectations. It does follow a 12.7% jump, however, so some give back was expected. Building permits were similarly weak, though, causing some concern about future months.

THE WEEK AHEAD

This week includes a spate of important economic news releases, highlighted by the final estimate for first quarter GDP. Subsequent data has caused most analysts to expect a downward revision of the second estimate to a 1.8% decline.

Also on the docket this week is existing homes sales, new home sales, Case-Shiller Home Price Index, durables goods, and personal income & outlays.

Abroad, important data releases are scheduled in Japan, including retail sales, inflation, and unemployment, as well as Europe: PMI composite, economic sentiment, and GDP figures for France and the UK.

Central bank policy announcements are due this week from Turkey, Hungary, Taiwan, and Czech Republic.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value