Second Quarter Finishes Higher

Equity markets rebounded in last week’s holiday shortened period, with the Dow Jones Industrial Average and the S&P 500 each climbing 1.3% (and the Dow crossing 17,000 for the first time). The second quarter also closed on Monday, with the S&P posting a robust 5.2% gain. It was the sixth straight quarterly increase for the index, the longest such streak since the late 1990s.

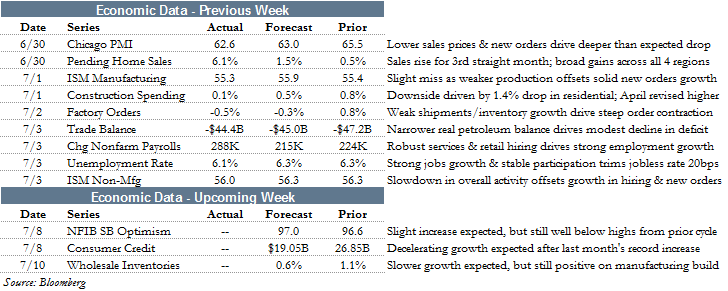

It was a strong week for economic data, punctuated by an upside surprise in Friday’s government jobs report. We discuss those results further in the topical section.

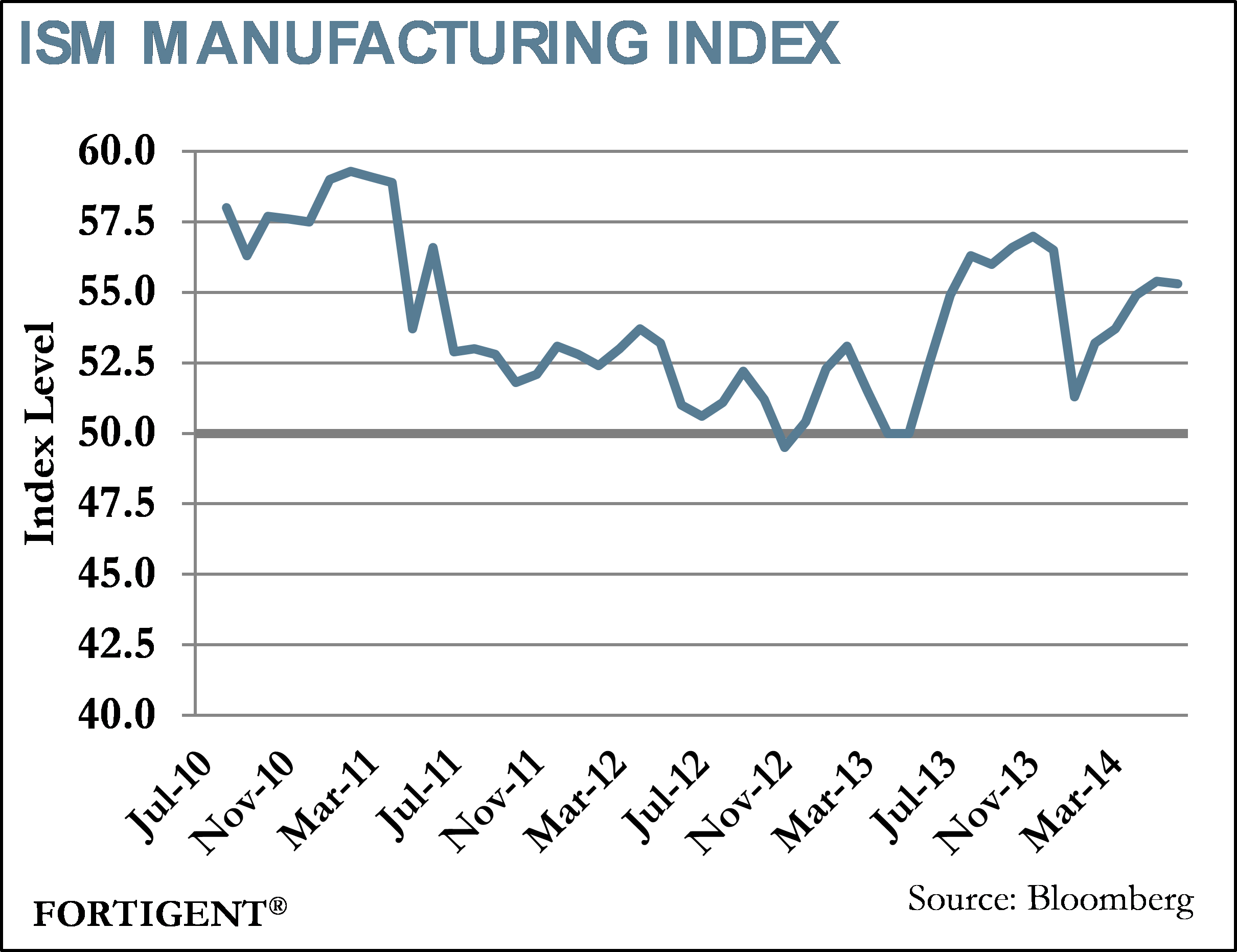

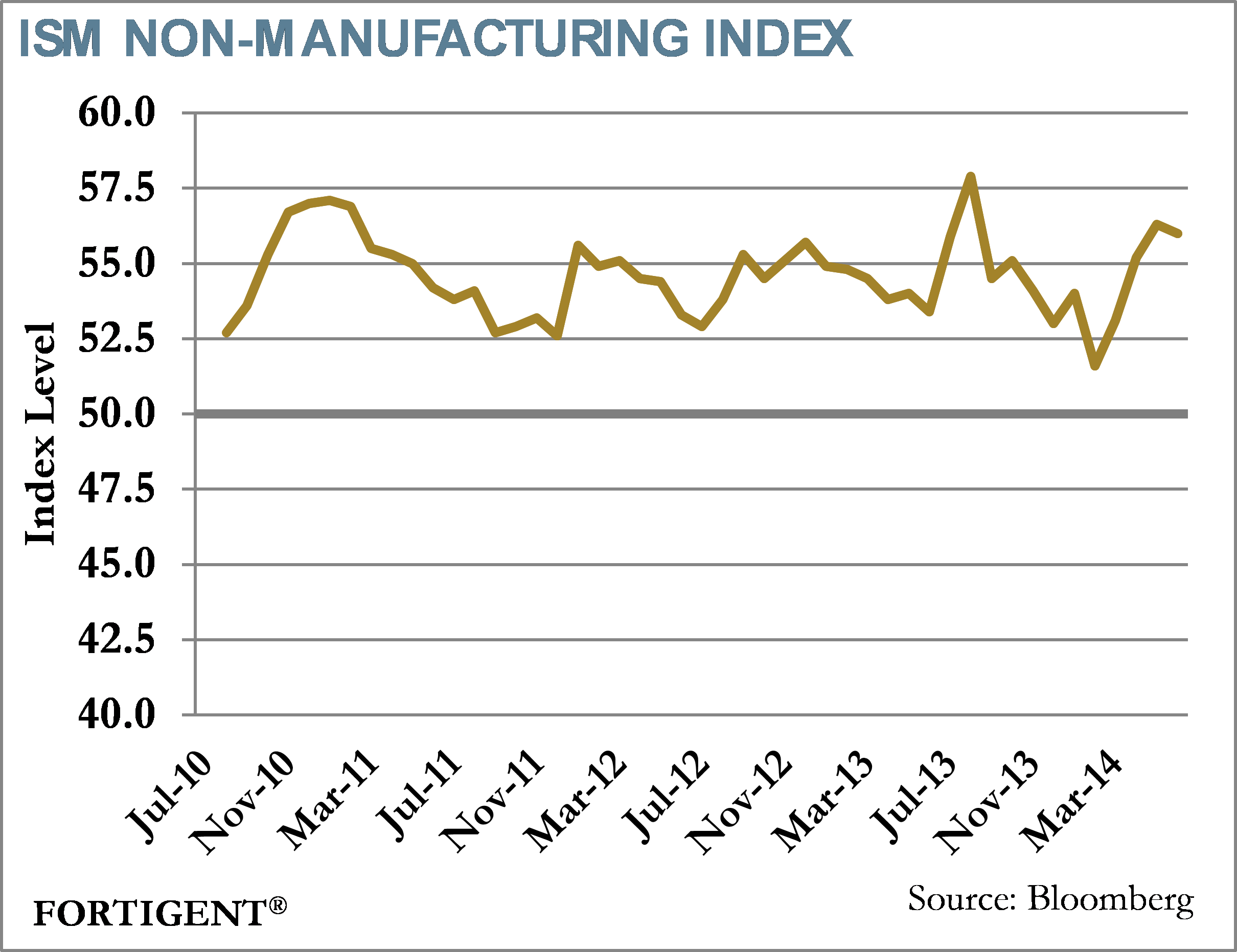

On the domestic front, the Institute for Supply Management (ISM) released its twin surveys on the health of the US economy.

The ISM Manufacturing Index remained in robust territory, coming in at 55.3, albeit slightly below expectations. Beneath the headline figure was encouraging news that new orders improved by two points to 58.9. Moreover, a sample of survey participants’ comments indicated a near-universal uptick in confidence, with the consensus suggesting improved business conditions relative to last year.

The ISM Non-Manufacturing index was faced with similar dynamics, coming in slightly below expectations but still in very strong territory at 56.0. Although business activity experienced a material downtick, new orders and employment both improved in June. As noted by ISM, “the majority [of survey respondents] indicate that steady economic growth is continuing.”

Investors received encouraging news on housing, as the pending home sales index increased 6.1% in data released for May. Improvement was broad based, and the headline increase was the largest such gain since 2010, according to Econoday. The report bodes well for future home sales data, which recently started rebounding from a slowdown in the back half of 2013.

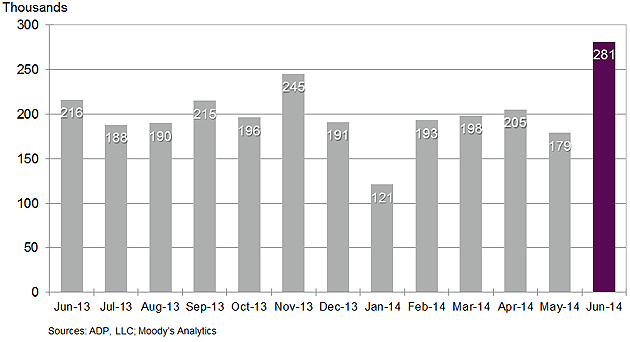

In the lead up to Friday’s government jobs data, ADP released its own estimate of private payroll growth. Like the official data, ADP employment surged past estimates to record a 281,000-job gain in June. According to ADP, gains in construction jobs were particularly impressive, “representing the highest total in that industry since February 2006.”

Change in Nonfarm Private Employment

Source: ADP

Abroad, a few important measures also made headlines.

In China, both official and private market estimates of the manufacturing sector improved in June. In fact, the HSBC/Markit Manufacturing PMI – which some regard as more reliable than government estimates – moved back into expansionary territory for the first time since January. The group’s composite PMI, which captures both manufacturing and the service sector, also was in positive territory for the second straight month and at its highest levels in more than a year.

In Europe, amid a European Central Bank meeting in which no new policies were announced, there were several reports to digest. Eurozone GDP was re-affirmed to have grown 0.9% year-over-year in the first quarter in the group’s second and final estimate. Data concerning more recent periods was underwhelming: unemployment remained unchanged at 11.6%, retail sales were flat (and below expectations), while manufacturing PMI softened to 51.8 from 52.2. Producer inflation also came in at negative levels, furthering fears that a deflationary cycle could grip this significant global economy.

Will Latest Jobs Report Force The Fed To Act?

After a reasonably bleak winter, labor markets are on the rebound, just in time for the Federal Reserve to decide when they should stop asset purchases. Recent figures suggest that labor markets are very near Fed targets, raising the possibility that interest rate hikes could begin sooner than expected.

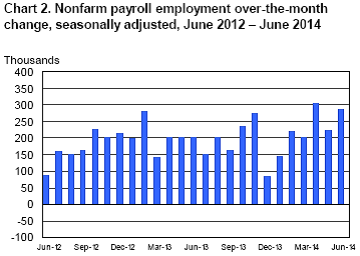

In June, payrolls expanded by 288,000 and the unemployment rate declined to 6.1% from 6.3% the month prior. June was viewed as a very positive report, particularly after May and April payrolls were revised higher to 224,000 and 304,000, respectively.

Source: Bureau of Labor Statistics

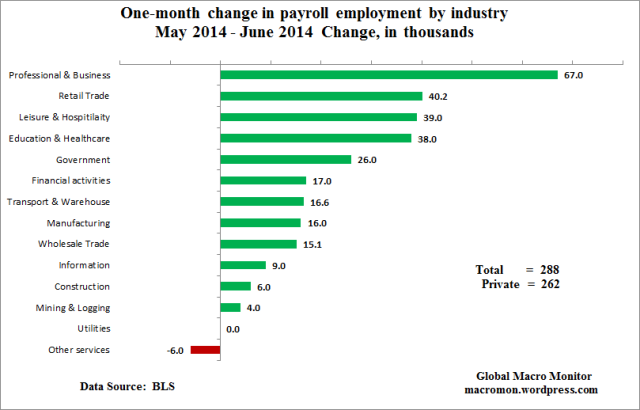

At the industry level, payroll gains came from a wide range of companies, led by professional & business services, retail, leisure & hospitality, and education & healthcare.

Source: Global Macro Monitor

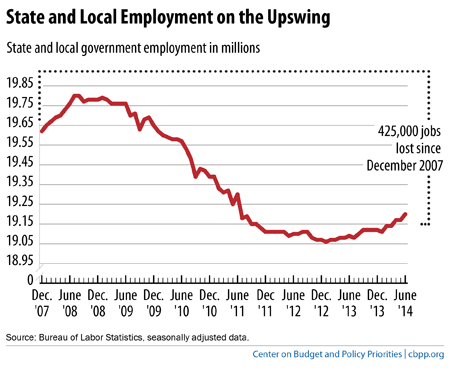

One area that experienced surprisingly strong growth last month was state and local governments, showing gains of 24,000. Since December 2007, state and local governments have shed more than 400,000 jobs, but there has been some improvement in recent months. Much of the gain in June came from school districts, according to CBPP, but the overall trend at the state and local level is becoming increasingly positive.

Source: Center on Budget and Policy Priorities

The biggest inhibitor to Fed action has been stagnant prices. Without wage growth, the ability to raise prices has been limited, but

there are signs pointing towards improving trends in wages. In June, average hourly earnings increased 0.2% for a 2.0% gain in the past year. Production workers experienced a 2.3% gain in average hourly earnings during the last year.

As labor markets enter a period of more sustainable growth, and wages begin to rise proportionately with historic norms, pressure on the Fed to act is also increasing. It was widely believed that the Fed would not raise the Fed Funds rate prior to 2016, but those expectations are shifting due to better

economic data. Over the weekend, Goldman

Sachs moved its target date for Fed Funds increases from 2016 to the third quarter of 2015.

The Fed has been inclined to hold the course for many quarters now as inflation was nonexistent and unemployment was stubbornly high, but those excuses are waning with unemployment falling quickly and inflation stabilizing. Investors and strategists have long struggled to predict the exit path for the Fed, but a strengthening economy is bringing the exit path closer to fruition.

The Week Ahead

It is a fairly quiet week for economic data, with the highest profile reports including the NFIB Small Business Optimism Survey and minutes from last month’s FOMC meeting. Select European country data will also be made available, including industrial production for Germany, France, Italy, and the UK. Chinese inflation data is also on tap.

In terms of global policy decisions, there are ECOFIN and Eurogroup meetings this week, as well as a Bank of England meeting on Thursday. Other central bank policy announcements are due from Indonesia, South Korea, Serbia, Malaysia, Peru, and Mexico.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value