Economic Signals Are Improving, Which Should Help Equity Prices

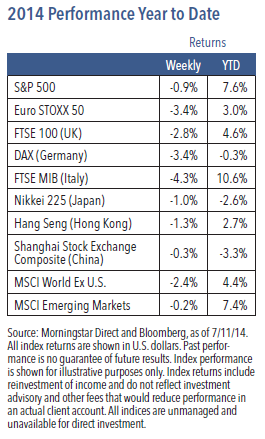

U.S. equities lost ground last week, with the S&P 500 Index dropping just under 1%, its largest weekly loss since early April.1 Cyclical sectors lagged, while defensive areas (chiefly utilities and telecommunications) led the way. A number of factors could be blamed for the decline, including signs of slowing European growth and lingering debt problems, as well as some downward revisions in corporate earnings guidance. In our view, however, the most reasonable explanation for the pullback may simply be fatigue and consolidation following the multi-week price advance. In any case, this sort of pullback is a normal part of a bull market. Overall, our observations point to stronger economic growth and higher equity prices, and we offer seven reasons why we remain constructive:

Seven Reasons to Remain Positive

1. Leading indicators are pointing to an economic acceleration. The Purchasing Managers Index readings have been moving higher,2 payrolls are increasing,3 inflation expectations are rising, bank lending levels have accelerated and earnings estimates are generally improving.

2. The U.S. manufacturing and energy renaissance is continuing to unfold, with manufacturing employment increasing at its fastest pace in over 30 years,4 and U.S. oil production surging as imports from OPEC decline.5

3. It has become increasingly difficult for those with bearish views to find indicators that don’t show accelerating growth. We expect yields to rise as bond markets begin to realize that the recovery is more certain.

4. The current recovery is the slowest in the post World War II period.6 As a result, the economy still has excess capacity, which should allow growth to continue.

5. Monetary policy should remain accommodative for a protracted period, although the Federal Reserve will increase the fed funds rate at some point.

6. Historically, bull markets falter when recessions ensue, not when valuations become more expensive. And we believe recession risks are very low.

7. In our view, the main driver of the bull market has shifted from supportive Fed policy to fundamental factors. A continued focus on earnings growth, dividend increases, valuations and other fundamentals should keep the market grounded and prevent it from getting ahead of itself. Although some investors believe the market has already gone too far and is overvalued, we find this sort of controversy reassuring. It is when investors start ignoring fundamentals altogether that markets tend to enter into bubble territory.

An Overweight to Equities Still Makes Sense, but Watch for a Market Correction

Investor anxiety appears to be high, but the bottom line is the economic backdrop and market fundamentals sill warrant overweight positions in equities. As the global economy slowly improves, U.S. corporations become more healthy, consumers reduce debt levels and monetary policy stays supportive, we believe equity markets look attractive. Additionally, “risk free” Treasury bonds and cash are overvalued or are producing extremely low returns. Finally, we would point out that many investors are still cautiously positioned and ample cash is sitting on the sidelines, indicating equities should have further room to run.

This is not to say that risks have vanished, however. Given the fact that markets appear fatigued and that it has been nearly three years since we have seen a 10% correction,1 we could see a pullback occur at any time. We are often asked what could cause such a correction. A few likely culprits could be a jump in bond yields, a spike in oil prices or heightened concerns about Fed tightening. When and if a correction does happen, we would expect it to be a temporary occurrence as long as the economy remains on track. For now, and over the next six to twelve months, we expect economic growth to improve, providing a tailwind for corporate earnings. With such a backdrop, we expect stock prices to rise and bond yields to move higher.

1 Source: Morningstar Direct, as of 7/11/14. 2 Source: Institute of Supply Management. 3 Source: Bureau of Labor Statistics. 4 Source: Cornerstone Macro Research. 5 Source: U.S. Energy Information Administration. 6 Source: Bureau of Economic Analysis.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment- grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results. Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2014 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM1-0714P 1970-INV-W07/15