Markets Slide on European Woes

Equity markets continued their up-and-down pattern, as the S&P 500 slipped 0.9% last week while the Dow fell 0.7%. Small cap stocks fared much worse, with the Russell 2000 plunging 4.0% in the period. Foreign stocks also suffered, as the MSCI EAFE declined 2.4%.

It was a very limited week of economic data, with reports such as the NFIB Small Business Optimism Index and Consumer Credit overshadowed by the release of Fed minutes on Wednesday. Despite the mostly positive nature of data last week – and a strong report by Alcoa to kick off second quarter earnings season – markets sank on news of renewed trouble in the European banking sector.

On Thursday, the parent company of Portugal's Banco Espirito Santo announced that it would be skipping bond payments. A dramatic selloff in the security led to regulators suspending further trading of the stock. The development caused many investors to fear another bout of contagion that gripped the European financial system in 2011 and 2012.

Most analysis of the default in subsequent days suggests it will not lead to a systematic crisis. Barclays Research, for example, notes that Portugal maintains sufficient capital to fund its operations through the year without significant additional bond issuance. After nearly two years of a much more benign trading environment in the region, however, Banco Espirito is a stark reminder that many structural issues remain yet unsolved in Europe’s financial system.

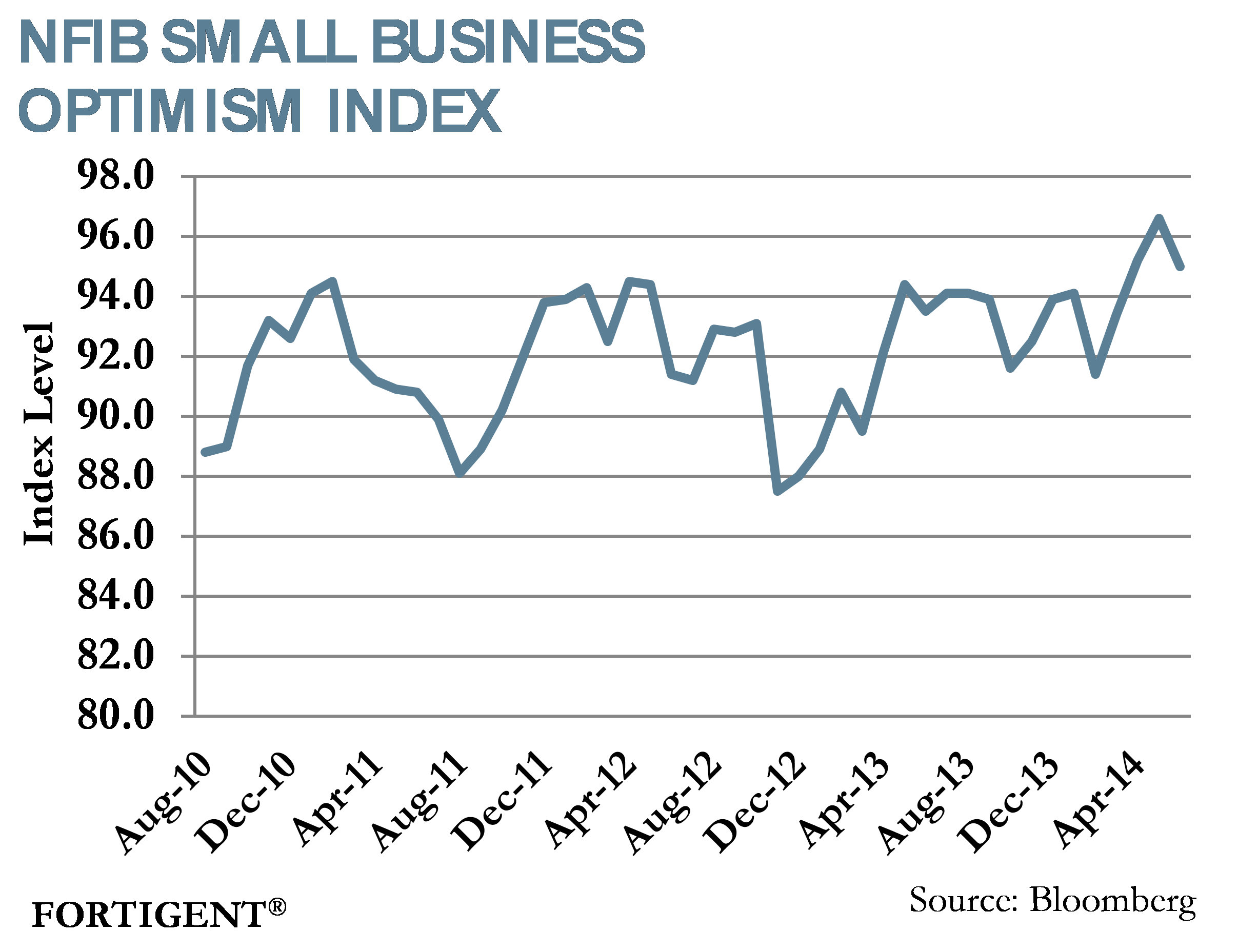

Back in the US, economic data was generally positive, with the exception of the NFIB report.

The National Federation of Independent Businesses (NFIB) Small Business Optimism Index slipped 1.6 points in June, a reversal after a solid three-month run. Only two of the index’s 10 components increased, though both were encouragingly tied to labor markets: businesses with current job openings and those planning to increase employment in the future. As noted by the NFIB, the job component measures improved to levels seen only in “strong private sector economic times.”

Source: NFIB

On the negative side, there was weakness in capital outlays and planned spending. Expectations for improving business conditions also fell sharply. The NFIB noted the index did remain above 95.0, which had been a ceiling for the measure in the early part of the recovery.

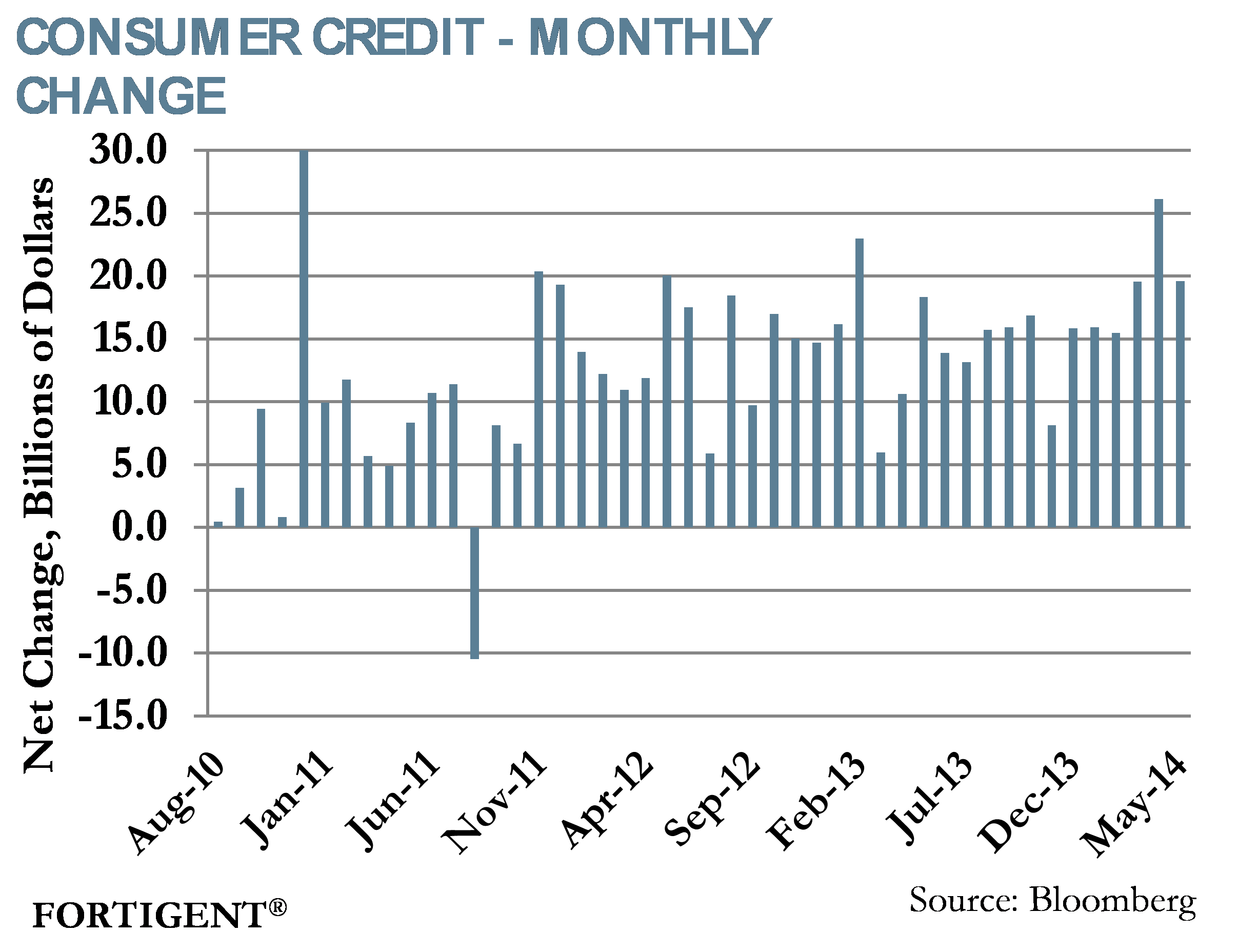

Consumer credit increased by $19.6 billion in May, which came in more than $2 billion above expectations. Moreover, the revolving credit component, which better represents credit card use by consumers, managed another increase following a sharp $8.8 billion gain in the prior month. Although a somewhat delayed measure compared to sentiment surveys, healthy credit card usage may serve as a better indication of consumer confidence.

More positive news on the labor front came via weekly jobless claims data that suggested the jobs market continues to improve. In the week ending July 5, initial jobless claims sank well below consensus estimates to 304,000. This represented a drop of 11,000 claims and pushed the four-week moving average to 311,500 – near recovery lows.

The Fed Announces Its Intentions

Minutes from the mid-June FOMC meeting were released last week, offering keen insight to the Federal Reserve’s current thinking on the economy. While the Fed suggests that the economic outlook is benign, the minutes offered guidance on the Fed’s exit path, which is expected to arrive by the end of the year.

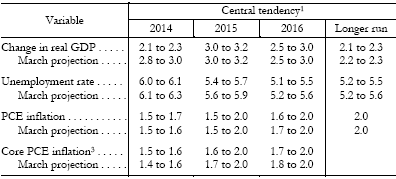

Within the minutes, the FOMC noted “improvement” in labor market conditions, “subdued” activity in housing markets, and “modest” increases to measures of labor compensation. At the aggregate level, FOMC members reduced projections of economic growth for this year, and made a slight adjustment higher to projections for inflation.

Source: Board of Governors of the Federal Reserve

The more important part of the minutes came on page 10, where the FOMC reported that its final month of asset purchases would occur in October. It was not a particularly surprising revelation given the recent trajectory of asset purchases, but there was some debate about extending purchases to year-end.

Source: Econoday

Bringing about a conclusion to asset purchases is only part one of the Fed’s path towards interest rate normalization. A number of other policies were put in place after the crisis, and unwinding those numerous policies is not expected to be easy.

For example, securities the Fed purchased have gradually been maturing and, rather than holding cash, the Fed chose to reinvest those proceeds. The proper time to end that practice is up for debate. Some members of the FOMC believe it is best to end reinvestment prior to hiking interest rates, but others believe the right course of action is increasing interest rates first, then bringing a conclusion to the reinvestment program.

Determining the right time to begin rate hikes is also going to be a tough subject. One member of the FOMC believes interest rates should increase by the end of this year, but the majority believes that 2015 is more fitting. However, another three members do not believe rates should rise before 2016. Even within the majority, expectations are varied. Of the individuals believing that 2015 is the right time to raise rates, one person feels that rates should rise quickly and reach 3% by the end of the year. A number of people are suggesting a target of 1.5%-2% and another group fall in the camp of slow, gradually spaced increases.

It finally appears that after many years, the Federal Reserve is making its way towards a “normal” interest rate environment. The exit path will be fraught with potholes and potential pitfalls as members of the FOMC bring varied opinions. So far, the start of the exit has gone smoothly and we can only hope that the Fed continues to move in such a deft manner.

The Week Ahead

Economic data picks back up this week with a number of marquee reports. Those include retail sales, industrial production, and housing starts. Additional reports such as the Empire State Manufacturing and Philadelphia Fed Surveys are also on tap.

Earnings season heats up this week with reports from blue chip stalwarts such as Citigroup, J.P. Morgan, Johnson & Johnson, Intel, Bank of America, Schlumberger, Google, IBM, and General Electric.

Central bank policy announcements are due from Chile, Brazil, Canada, Turkey, and South Africa.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value