Accuvest Global Advisors, a California-based RIA and sub-advisor of the AdvisorShares Accuvest Global Opportunities ETF (ACCU) and the AdvisorShares Accuvest Global Long Short ETF (AGLS), share their analysis on the global marketplace.

A Powerful Relative Monetary Policy Advantage with Attractive Valuations, Fundamentals and Momentum

What Happened in H1 2014?

One of the most popular investment themes coming into 2014 was Hedged Japanese Equity (owning Japanese equities while simultaneously hedging out the risk of the Japanese Yen weakening against the US Dollar). At its core, this theme leaves investors long Japanese equities in US Dollar terms, not Japanese Yen terms. This investment turned in very poor performance for the first half of 2014. By the end of Q1 2014, Japanese equities had sold off rather sharply and the US Dollar had weakened 2.01% versus the Yen. An investor in the Hedged Japan Equity theme would have felt the 2% currency loss as well as the 8.24% loss seen in the MSCI Japan Index during Q1 2014. This 10.25% loss over 3 months helped to “reset” the trade and allowed for a more attractive entry point for the thematic investment.

The underperformance in early 2014 can be attributed to a few factors. The theme was crowded by the end of 2013, and after strong 2013 performance the trade was meaningfully overbought, setting the stage for mean reversion and profit taking. More so, the loss of 2013 momentum coincided with fears of an Emerging Market (“Fragile Five”) currency crisis that escalated in January. These concerns led to broad selling of emerging market investments, strengthening the Japanese Yen as the global carry trade unwound. Furthermore, a 3% sales tax increase in Japan went into effect in April. This led to noise in economic data and uncertainty regarding the medium-term trajectory of the Japanese economy and monetary policy.

We are attracted to the Hedge Japan Equity theme for three primary reasons. First, the explicit policy of the Bank of Japan and Government of Japan is to weaken the Yen, create asset price inflation, and support economic growth. Importantly, the policies had a positive impact during 2013, and more accommodative initiatives are expected in 2014 and beyond. Second, valuations are attractive while fundamentals are strong. Third, near-term equity price momentum is positive and accelerating.

Abenomics

Japan’s monetary accommodation, fiscal policy, and structural reforms have been coined “Abenomics” after Japan’s Prime Minister Shinzo Abe. Abenomics is a three arrowed multi-front attack on the deflation and slow growth that has mired Japan for more than 15 years. The first arrow is monetary accommodation (creating negative real interest rates, expanding the central bank’s balance sheet, and weakening the Yen), the second arrow is fiscal policy (tax cuts), and the third arrow is structural reform (industry de-regulation, increasing women in the workplace and incentivizing investment). Importantly, the Bank of Japan and the Government of Japan are coordinating their attack, a stark contrast to the level of US Congress and Federal Reserve cooperation during the implementation of “Quantitative Easing” in the United States. This “unified front” is crucial, as the BoJ and the Japanese Government need to establish creditability for Abenomics and the associated inflation target of 2%. Japan has an aging and traditionally risk-averse population, so Abenomics needs to be aggressive and persistent to overcome demographic pressures and break long standing expectations for deflation.

Monetary Policy

The primary objective of Japan’s monetary policy is inflation. Deflation can lead to liquidity traps where cash is horded and growth disappears. Japan’s “lost decade” (or more) is an example of the risks associated with a deflationary spiral. Although short lived (so far), the Bank of Japan has delivered price inflation. In April, prices for all items soared 3.4% from a year earlier, while prices excluding food and energy rose 2.4%. The challenge now is to maintain inflation long enough to change long term inflation expectations.

Inflation, and Yen weakness, allows the Bank of Japan to engineer negative real interest rates (nominal interest rate minus inflation). Negative real interest rates make it expensive to hold cash and low yielding fixed income (like JGBs). This condition creates an incentive for investors and Japanese household to allocate to riskier assets, like equities and real estate. Furthermore, negative real interest rates benefit any business, households, or government institutions that carry a debt as inflation can cover interest expense and even some principal.

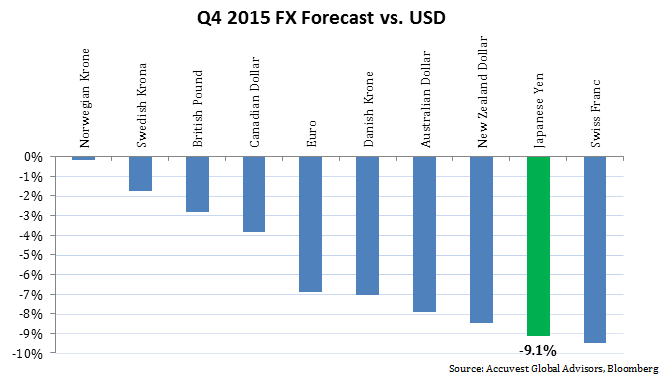

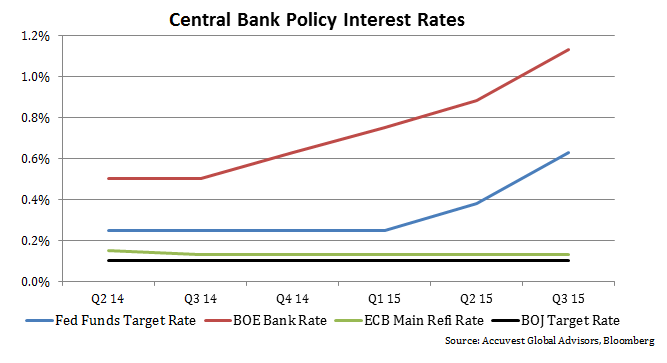

Relative to the other central banks, Japan has a more accommodative interest rate policy. Not only is the Bank of Japan’s interest rate lower than other central banks, the rate is expected to stay lower for longer. This relative monetary policy, and interest rate differential between the U.S. and Japan, should drive U.S. Dollar strength versus the Yen.

A weaker Yen should benefit Japanese exporters. Japan’s primary exports have fairly inelastic demand, meaning export prices usually do not need to drop as much as the Yen depreciates, yielding higher profits for exporters.

Fiscal Policy

On June 25th, Japan’s Prime Minister, Shinzo Abe, announced that the government will aim to cut the corporate tax rate to below Germany’s levels. According to Japan’s Finance Ministry, Germany’s effective corporate tax rate was 29.55% as of Jan. 2013, and Abe projected that the final landing spot for the corporate tax rate would be between 20%-29%. The Cabinet approved a plan to start cutting corporate taxes from FY2015, with aim of lowering the level to under 30% in a few years. Japan’s corporate tax rate is currently around 35.6%, and it is estimated that a 5% tax cut will improve TOPIX equity index overall ROE by approximately 60bps.

Structural Reform

If structural reforms, the third arrow, are to have large effects, we would expect to see it first in rising forecasts of real future growth and lower long run inflation expectations. If inflation expectations fall at the same time as growth forecasts rise, it would suggest that forecasters expect positive future supply shocks.

Only the tip of the “third arrow” has been revealed, but these initial reforms could have a meaningful impact on growth and consumption. Agriculture reform, even given disappointments, should, on the margin, raise aggregate disposable personal income. This should happen through reducing subsides for inefficiency, and by increasing consolidation of farmland, allowing agricultural households easier access to accumulated illiquid wealth. Also, medical reforms should raise households’ purchasing power, another implicit rise in disposable income. In aggregate, the consumption effects of the announced reforms could be significant.

While monetary and fiscal policy initiatives have been broadly outlined, the structural reform arrow of Abenomics still remains largely undisclosed. It is important that Prime Minister Abe and the Japanese Government use this opportunity to strengthen the creditability of Japan’s inflation target. Prime Minister Abe’s is expected to continue rolling out revamped growth initiatives and reforms to generate new investor enthusiasm. New initiatives could include immigration reform and enticing women into the workforce, two moves that could help Japan overcome an aging population and shrinking workforce.

Enhancing the creditability of the BoJ and Government will help convince Japanese households and the Government Pension Investment Fund (GPIF) to re-allocate to risk assets and away from Japanese Government Bonds. Only 8% of aggregate Japanese household assets (roughly $15Tr) are invested in equities. The Japanese government hopes that the NISA accounts (Nippon Individual Savings Accounts) will draw approximately $250B into the Japanese equity markets, while Nomura Research Institute estimates that it could be as high as $690B. Furthermore, the GPIF raised their target equity allocation from 18% to 26% at the end of 2013, and it is expected that this equity allocation will continue to grow.

Abenomic’s – Green Shoots

In late June, Japanese Prime Minister Shinzo Abe told reporters, “A virtuous cycle is appearing in Japanese economy.” JP Morgan’s Head of Japan Equity Research agrees, recently stating, “The private sector getting its mojo back. Consumer spending led the economy last year, now business investment is beginning to pick up. Businesses are retooling their factories, and wage growth is beginning to pick up.” Adding that, “Part time workers represent 40% of all paychecks, and these part-time wages are growing at 6%” driving domestic demand.

Additionally, average land prices for Japan’s three largest cities rose last year, marking the first annual growth since 2008. Real estate transaction volume rose 70% from 2012 to 2013. The 3% sales tax hike in April has created noise in the Q1 and Q2 economic data, but it is important not to get caught in the noise as Japan appears to be exhibiting sustainable economic acceleration. Many economic indicators saw a spike before the April tax hike as demand was pulled forward from future months into March. This has resulted in a May and June drop in economic activity relative to March and April. The noise in economic data should level out going into Q3. Despite the noise, Japanese equities appear to be in an attractive position. Similar to the set up for U.S. Equities around the announcement of QE2, either the economy surges from here and equities rally, or the economy stalls and more aggressive Abenomics is applied, and equities rally.

Valuations & Fundamentals

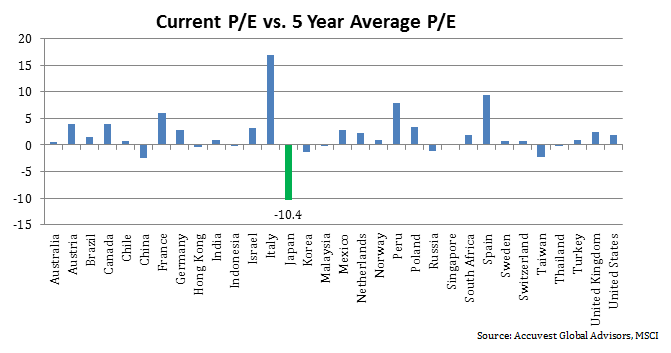

Japanese equities, as defined by the MSCI Japan Index, are attractive on an absolute and relative basis. Out of a universe of 32 countries, Japan has the 5th lowest price to book ratio (1.23x) and the 8th lowest price to cash earnings ratio (7.20x). Relative to history, Japan has the #1 ranked value profile. Japan’s current P/E ratio is 10.4x lower than its 5 year average P/E ratio. Furthermore, Japan’s forward P/E multiple is trading at a 10.6% discount to the MSCI World, the largest discount in 20 years.

Meanwhile, growth fundamentals in Japan are strong and have room to strengthen further. Out of 32 countries, Japan has the #1 ranked earnings per share trend and the #2 ranked year-over-year growth in earnings.

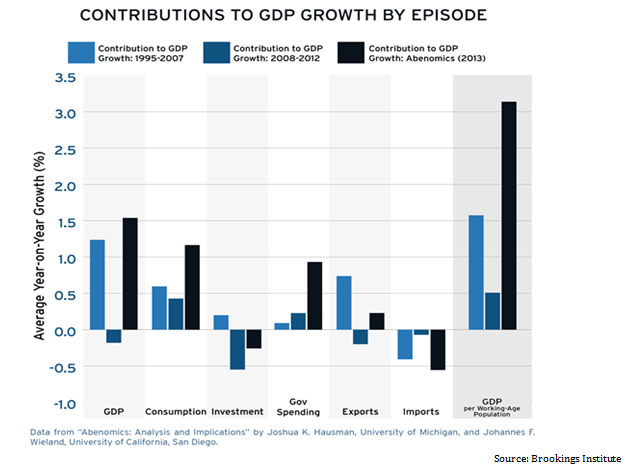

Importantly, there appears to be room for growth fundamentals to improve. The Brookings Institute estimates that the Japanese economy has an output gap of 4% to 10%. An output gap is the difference between a country’s potential growth and actual growth. The effects of Abenomics are believed to have closed this gap by 1%, leaving a meaningful gap still left to be closed. Furthermore, Japan’s return on equity, a key fundamental indicator, appears to have bottomed. The ROE of the MSCI Japan index currently rests at 8.46%, 28th ranked out 32 countries. While this ROE level is low relative to the rest of the world, Japan’s ROE trend is impressive and there appears to be room for a continuation of this trend.

Price Momentum & Share Buy Backs

The MSCI Japan Index (hedged for JPY currency risk) is up 8.4% since May 21st. This rally occurred after selling off more than 12% between January 1st and April 14th. Additionally, Japanese companies bought back US$2 Billion worth of shares in in Q1 2014, a 54% increase from Q4 2013 and a strong sign of attractive valuations and earnings growth.

From a longer term perspective, we may have seen a secular low in Japanese valuations and equity performance in late 2012. The Price to Book Value Ratio of Japan’s TOPIX Index contracted from 4.4x in December 1989 to 0.88 in September 2012. Over this same time period, a currency hedged U.S. Investor in Japanese equities experienced a 75% loss. Since September 2012 the Price to Book Ratio of the TOPIX Index has expanded from 0.88 to 1.23, while gaining 80% through the end of 2013. After some momentum consolidation in early 2014, this theme looks poised to push higher on the back of unprecedented government accommodations and a blend of attractive valuations and improving fundamentals.

Sources: Bloomberg, Accuvest Global Advisors, Brookings Institute

Disclosures:

This article was written by James Calhoun, a Portfolio Manager at Accuvest Global Advisors (AGA). This article is strictly informational and should be used for research use only. It should not be construed as advertising material. The opinions expressed are not intended to provide investing or other advice or guidance with respect to the matters addressed in this brochure. All relevant facts, including individual circumstances, need to be considered by the reader to arrive at investment conclusions to comply with matters addressed in this brochure. Charts and information are sourced from AGA and the MSCI, unless otherwise noted. Remember that investing involves risks, as the value of your investment will fluctuate over time and you may gain or lose money. You should seek advice from your financial adviser before making investment decisions. Investment risks are borne solely by the investor and not by AGA. AGA is an independent investment advisor registered with the SEC. All disclosures, marketing brochures, and supplemental firm sheets are available upon request.