Farmland is a real asset that combines solid investment fundamentals with the potential for attractive cash yields, inflation hedging, and consistent returns from biological growth. Furthermore, farmland total returns tend to be uncorrelated with financial asset returns, offering genuine portfolio diversification for institutional investors. While institutional ownership within the asset class has grown steadily over the past few years, it still accounts for less than 1%1 of total global agricultural land ownership, presenting significant opportunity for sustainable yield enhancement through targeted farmland investment in certain regions.

The pages that follow present an overview of the key characteristics and potential risks of farmland investing, consider the routes for implementation, and make the case for a diversified, cross-regional approach to the asset class.

Farmland Investments Defined

Farmland investments consist of direct investments in rural land along with crop and livestock assets that produce food, fiber, and energy. Farmland investments focus on the productive capacity of the land base, and returns are based on the biological growth of crops and livestock, as well as appreciation of land and related assets. By their nature, farmland investments are long-term illiquid investments in real assets.

Investments are grouped into three general categories:

1.Row crop investments include annual crops such as corn, soybeans, cotton, wheat, and rice.

2.Permanent crop investments include perennial crops such as fruit and nut crops, which have both pre-productive and mature periods. Pre-productive or “greenfield” investments where trees or vines are planted on bare ground have a “J-curve” return profile. Some mature permanent crops, like almonds, peak in productivity and then decline, so orchard age is an important factor in estimating productivity and value.

3.Livestock investments include land leased to local operators for grazing or direct livestock ownership and operation.

Institutional farmland investing typically focuses on globally competitive agricultural sectors including:

■Corn, soy, wheat, rice, and other bulk commodity row crops that can be produced most efficiently at scale.

■Relatively storable permanent crops such as nut crops or wine grapes.

■Large-scale livestock production, including dairy and beef cattle operations.

Efficient global producers, such as U.S. corn, soybean, and nut crop, New Zealand dairy, and Australian beef producers, benefit from participation in export markets, and receive a globally determined price for their output.

Management Style: Leasing vs. Direct Operation

In many regions of the U.S. and some other parts of the developed world, row crop properties can be leased to high- quality local farm operators at fixed or variable rents that provide attractive yields to the investor. These farmers leverage the scale and productivity of their operations by owning some land, but also leasing land from investors in order to maximize their return on investment. In other geographies lacking a robust farmland rental market, particularly in developing regions, a lack of leasing demand from qualified farmers makes direct operation the best approach to maximize returns. In direct operation, the farmland investment manager employs a farm manager to operate the farm. While direct operation involves a higher risk/return profile because the investor assumes both price and yield risk, it is often the preferred management style for permanent crops and livestock as it ensures that the long-term asset is well-managed and value is maintained.

Property Management

Like most real estate investments, farmland investment requires specialized property-level management. While more intensive property management is required for direct operations, property managers also provide critical oversight of tenants operating leased farms. Property management may be vertically integrated with investment management or outsourced to third-party providers. Outsourcing allows the investment manager to hire the property manager best suited to manage each type of investment in each region and can be more cost effective as the fund manager need not invest in property management infrastructure in multiple locations. Utilizing a third-party property manager enhances transparency, as it allows for a true separation of fund- and property-level expenses.

Investment Vehicles

Investors can participate in the farmland asset class through direct investments or through the use of a specialist farmland investment manager, that may offer funds, co-investments, or separately managed accounts. For most investors, developing a well-diversified portfolio of direct investments is prohibitively complex and time-consuming. Investing in farmland through a farmland investment manager can provide the benefits of diversification, experience, and scale. Closed-end funds have a fixed term with some potential for extension, but are generally illiquid for the term. As with private equity, fund terms can vary widely. Open-ended funds and publicly-traded REITs provide more liquidity, but valuation at entry and exit can be an issue in open-ended funds, and the performance of public REITs can be influenced by capital market trends and other factors apart from the underlying farmland investment. Co- investments and managed accounts often require a larger minimum investment, but offer investors a greater measure of control.

Sources of Return

Returns typically consist of current income from annual lease payments or from annual crop or livestock sales, plus land and related asset appreciation. Appreciation reflects the income-producing capability of the investment based on anticipated future crop/livestock prices and yields. While soil quality and climate/water availability are relatively fixed determinants of a property’s potential yield, technological and management improvements can be brought to bear on individual properties to enhance yields and returns to investors. Capital improvements such as irrigation, laser leveling, and drainage can increase current income as well as future value, as improvements that permanently increase productivity are eventually capitalized into land values.

The timing of cash flow distributions from farmland investments is dependent on both the investment vehicle and the actual investments in the portfolio and how they are managed (leased vs. direct operation). Cash flow available to distribute will depend on the relative proportion of developmental (pre-productive) properties and cash-flowing properties in the portfolio. Lease payments are typically received before the farmer enters the field, while revenue from direct operations is received as crops are sold over time. A leased U.S. row crop property may produce a relatively consistent annual income return of 3-5%, depending on its quality and location, while some directly- operated permanent crop properties can produce double-digit annual income returns, but with significant variability due to annual fluctuations in price and yield. Closed-end funds typically distribute cash flow net of working capital reserves and cannot reinvest income in additional properties, while evergreen funds and separate accounts may choose to reinvest a portion of income and realized gains. A REIT must distribute at least 90% of its taxable ordinary income to shareholders annually in the form of dividends.

How Farmland Fits in an Institutional Portfolio

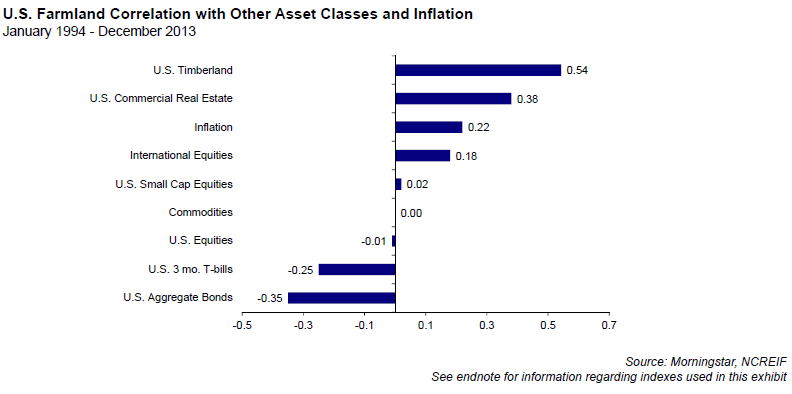

Farmland has historically generated attractive returns, with excellent capital preservation and portfolio diversification at a low to moderate level of volatility. Some institutional investors allocate to farmland in the context of a diversified real asset portfolio that may include investments in real estate, infrastructure, forestry, and farmland. Others may include farmland in private equity or other illiquid asset categories. The exhibit below shows the 20-year realized correlation of U.S. farmland to other asset classes. While exhibiting low correlation to financial assets like stocks and bonds, farmland investments can provide a bond-like current income stream from lease payments or more variable income from direct operations, along with the potential for capital appreciation. In addition, through thoughtful portfolio construction, the risk/return profile of a farmland allocation can be varied to meet different risk/return preferences.2

Portfolio Diversification

Farmland portfolios can be structured as a balanced mix of row crops, permanent crops, and livestock or can be focused on a particular strategy/sector or other variations across the spectrum from fully-diversified to targeted investments. Portfolios may include ongoing farming operations or developmental “greenfield” or timber conversion strategy investments. As described above, leased row crops offer the lowest risk/return profile because the farmer takes on the price and yield risk, paying the investor a modest bond-like rate of return before beginning to farm each year. Participating or crop share leases allow both the farmer and investor to participate in some portion of annual upside/ downside. Directly operated permanent crops and livestock can provide higher returns, but the investor is exposed to both price and yield risk, thus increasing return volatility and potential for operating loss. Mixing low-risk leased investments with higher-risk directly operated strategies (including developmental/conversion properties) can provide current cash flow along with upside potential. Focused portfolios invested in a single sector such as leased row crops or livestock may fit a specific investor objective such as a desire for stable but modest returns (leased row crops), or an interest in higher income and appreciation potential (livestock and permanent crops), but more diversified strategies can help mitigate non-systematic risk.

Geographic diversification is also related to strategy choice. For example, globally competitive dairy and beef production might dictate investment in New Zealand and Australia, while leased row cropland is the norm in the U.S., but not necessarily in other geographies. In some regions, mixed-use properties that may include crops, livestock, and timber offer value-oriented opportunities relative to pure single strategy investments. Investing in emerging countries can provide greater upside potential, but at higher risk levels than developed country investments. Portfolios can be tailored to desired levels of diversification, but relative value and opportunity across sectors and geographies should be considered as well.

Investment Performance

Historical returns to direct farmland investments have been relatively high over the past two decades and particularly over the past decade as farmland investing has gradually gained popularity among institutional investors. Initially a long-term investment utilized by a small number of insurance companies and large pension plan investors, farmland investing has become more mainstream due to a convergence of factors: favorable supply/demand fundamentals, globally low investment yields in traditional “safe” assets like bonds, and increasing investor interest in diversifying real assets capable of providing an inflation hedge.

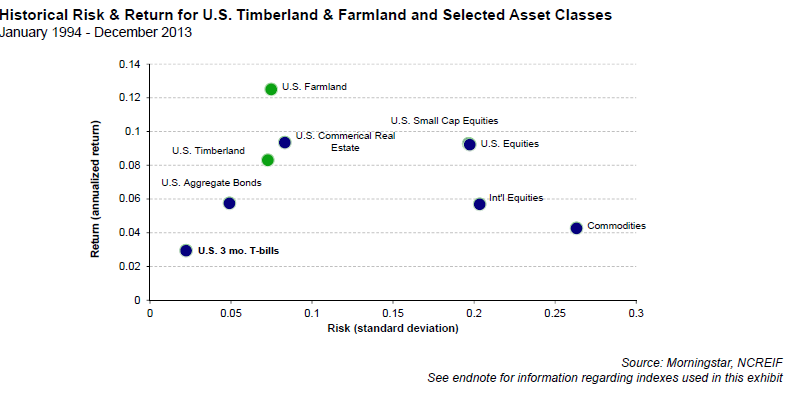

The National Council of Real Estate Fiduciaries (NCREIF) reports nominal annualized time-weighted total returns of 12.5% for its Farmland Index over the past 20 years and 17.5% over the past 10 years. On average, over the 20-year period, income has provided at least 50% of Farmland Index returns. Over both time periods, farmland, as represented by the Farmland Index, has generated higher returns than equity indices, with less volatility. It should be noted that this reduced volatility reflects in part the fact that farmland investments are not daily valued, but are typically appraised annually.3 The Farmland Index reflects the investment performance of a large pool of individual agricultural properties acquired in the private market for investment purposes only, and held in a fiduciary environment for the benefit of tax-exempt institutional investors, primarily pension funds. It includes property-level returns to U.S. farm properties only and is net of property management fees, but gross of fund-level fees. Given its tax-exempt, property-level focus, only the effect of property taxes is included in the Farmland Index. Despite its shortcomings as a benchmark for global agricultural investments funds, the NCREIF Farmland Index does provide evidence of trends in investment-quality farmland performance and is currently the only available index of its kind.

Supply-Demand Fundamentals

Given the strong performance of farmland in recent years, the question as to why today is a good time to invest is a reasonable one. The answer depends on global macroeconomic forces, but also on the specific global strategies employed and locations targeted for investing in farmland today.

The current outlook for farmland is driven by long-term positive supply and demand fundamentals that point to appreciation of both agricultural commodity prices as well as the land assets that produce these commodities. Given an increasing world population, developing economies that demand more meat in their diets, and a relatively fixed supply of arable land, high-quality farmland is expected to remain a valuable resource in the future.

Demand

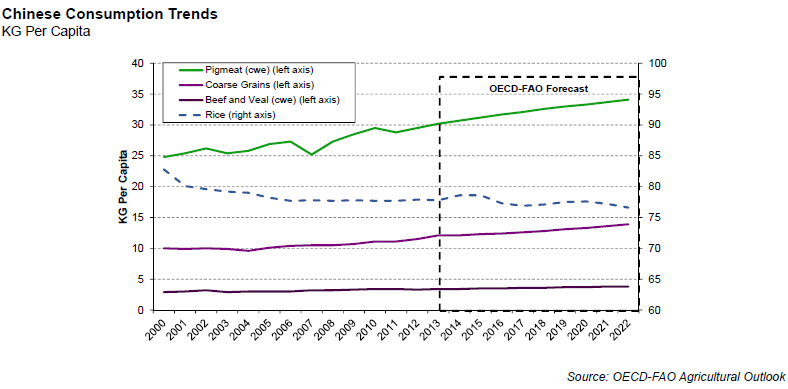

According to the Food and Agriculture Organization of the United Nations (UN FAO), global population, which is estimated to have reached 7.16 billion in 2013, is projected to increase to 9.55 billion by 2050.4 Between 2005-07 and 2050, under UN FAO’s baseline scenario,5 world food production needs to increase by 60% in order to meet the increasing demand. The forecast demand increase reflects additional population as well as the “grain multiplier effect,” that is, demand for grain to be used not as food, but as feed to produce livestock products such as meat and milk. According to the USDA,6 to produce one pound of chicken, pork, or corn-fed beef requires 2.6, 6.5, or 7 pounds of corn, respectively. As countries develop and their citizens gain wealth, consumption of animal protein (chicken, pork, poultry, beef, and dairy) rises, increasing demand for feed grains including corn and soybeans, and reducing demand for rice and wheat. For example, historical and forecast data from the OECD-FAO7 Agricultural Outlook in the exhibit below shows China’s demand for coarse grains increasing as its demand for meat increases, while rice demand declines.

Supply

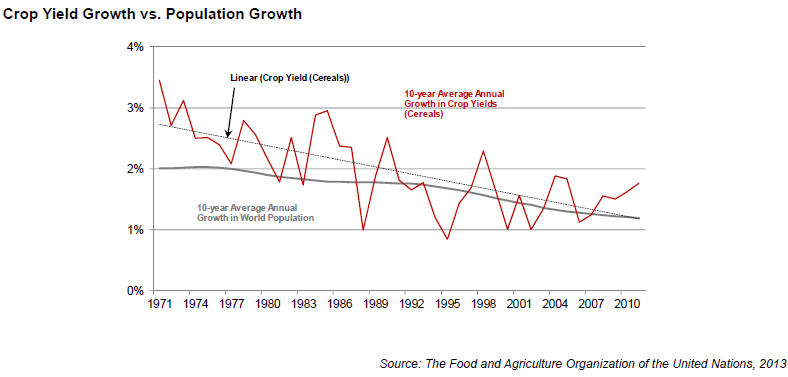

According to the FAO, most production increases will need to occur on the 1.5 billion hectares of arable land and permanent crops that are already being cultivated. Most land area suitable for crops is either already developed or environmentally sensitive. While some marginal land that is currently forested may transition into agricultural production if commodity prices dictate agriculture as the highest and best use, this is unlikely to have a meaningful impact. Despite some additional land at the margins coming into production in recent years, rising population has meant that arable land and permanent crops available for cultivation have been declining steadily on a per capita basis. Because future growth in farmland is limited, increases in food production must come principally from productivity increases. Following decades of crop yield increases brought about by improvements in plant genetics – as well as the widespread application of fertilizers and pesticides – such productivity gains are no longer outpacing population growth, as shown in the exhibit below. With demand growth poised to exceed productivity increases, farmland is expected to become an even more valuable resource in the years to come.

Food Security Concerns Also Drive Demand

Increasingly, countries lacking sufficient land or a suitable climate for farming are investing in large scale agricultural projects in countries with more plentiful agricultural resources, in order to secure future food production sources. Middle Eastern and Chinese sovereign wealth funds, among other large investors, have invested in farmland around the globe – from Australia to Brazil to Africa. Some of these investments have been welcomed as sources of capital to developing and other capital poor regions, but concerns have arisen in both developed and developing countries about the level of foreign investment and the potential for land grabbing.

Avoiding Bubbles

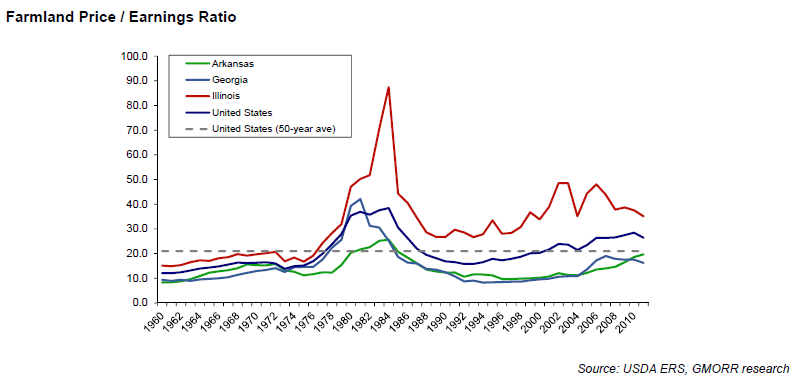

While long-term supply/demand fundamentals, including large-scale investor interest in the sector, should support farmland asset values in the long term, the recent surge in interest in the asset class has raised concerns about a near- term farmland “bubble” in some regions. Investors should carefully consider the relative value of the regions in which they invest as well as the risk/return profile of proposed regions and investment strategies. While global diversification can mitigate a number of risks inherent in farming, overpaying for a property can adversely affect investor returns. For example, looking at U.S. farmland from a price/earnings standpoint as shown in the exhibit below, farmland in Arkansas and Georgia appears to be relatively less expensive than in Illinois (Corn Belt), which has appreciated to a greater extent than regions such as the Mississippi Delta (Arkansas) and the Southeast (Georgia).

Value-oriented investors should therefore consider investing in lower-cost regions where relatively less capital has been invested to date, thus avoiding investment in potential bubbles.

When investing in properties with high-quality soils and adequate water availability, the prudent addition of capital can improve productivity, increasing the properties’ income and appreciation potential. In the U.S., improvements such as land leveling, irrigation, and drainage can boost lease rates and increase property values, while outside the U.S., improving farms in capital deficit regions can have an even greater impact on productivity and value. A diversified portfolio of both crops and livestock located in countries where land ownership rights are well-developed and adequate infrastructure exists (to allow for marketing of globally competitive crops) can mitigate the risk of investing in a single region or sector. Opportunities exist to bring sustainable management as well as capital and technology to capital-deficit or even financially distressed farms, mitigating the effects of prior unsustainable practices. For example, proper nutrient application, the addition of cover crops, and low-tillage techniques can improve cropland, while planting improved pasture grasses and enhancing access to water can improve livestock health and quality.

Risks Associated with Farmland Investing

In addition to the valuation risk associated with overpaying for an asset and the financial risk of utilizing excessive leverage, the main risks associated with farmland investing are yield and price risk and input cost risk, all of which can affect gross margins and thus reduce returns. Diversifying across agricultural strategies involving different types of crops and livestock in different geographic regions can help mitigate these risks. In some regions, yield, price, and input cost risk can be almost completely mitigated by leasing properties to local farmers who then assume all or part of these risks in exchange for a fixed or variable lease payment. Lease counterparty risk can be managed through prudent due diligence of lessee counterparties and diversification of lessees within the portfolio. Political risk can be mitigated by investing in countries that support capitalism and encourage foreign investment. Investing with managers committed to responsible and sustainable farmland management is also critical to minimizing risk.

Yield and Price Risk

Most of the factors that drive crop yields are controllable, to a certain extent, through the use of good management practices with the obvious exception being weather, notably rainfall. The negative effects of weather, however, can be reduced by selecting suitable varieties and hybrids for the expected conditions and by practicing sustainable soil management techniques to ensure that plants have access to the available water and nutrients at the appropriate times. To mitigate the risk of insufficient rainfall, irrigation can be used to improve yields in certain regions. Crop insurance is available in some countries to protect against low yields and crop failures, but the cost needs to be evaluated on a case-by-case basis. Investing in different geographies and different crop types can mitigate the effects of drought in certain regions and on certain crop types. Additionally, in the case of a drought or other yield-reducing event, crop prices generally rise, often offsetting, at least partially, the financial impact of the yield reduction. Thus, for a geographically diversified farmland portfolio producing commodities that are priced in global markets, properties in regions that did not experience a decrease in yield stand to benefit from the accompanying price increase. In direct operations, staggered forward crop sales over the period of the growing season can also help mitigate risk by locking in prices when they appear favorable.

Input Cost Risk

With the exception of fuel and petroleum-based products such as fertilizer, the costs of inputs are generally controllable and predictable, and can be locked in each year prior to planting. Additionally, targeting investments in agricultural strategies and regions that have a competitive cost advantage over other regions can result in considerably lower input costs than those for the same commodity in other regions. For example, New Zealand, the largest exporter of dairy products globally, enjoys a competitive cost advantage in dairy production.

Summary

Strong demand for farmland can be expected to continue in order to meet the increasing global demand for food, fiber, and energy, as well as to satisfy institutional investor demand for diversifying, inflation-hedging assets that produce a biological yield. Given the relatively fixed supply of land capable of supporting agriculture, an investment in farmland can reasonably be expected to both generate current income and increase in value over the long term. While a range of strategies is available, a disciplined, value-oriented approach that targets globally diversified farmland portfolios with a commitment to environmentally sustainable management practices offers the advantage of avoiding near-term regional “bubbles,” while enhancing agricultural productivity and farmland value for the long term. Choosing an experienced manager with deep relationships, local knowledge, and the infrastructure to manage a globally diversified portfolio is critical to successful investment in farmland.

Endnote:

U.S. Farmland is represented by the NCREIF Farmland Index; U.S. Timberland is represented by the NCREIF Timberland Index; U.S. Aggregate Bonds are represented by the Barclays Capital U.S. Aggregate Index; U.S. 3-month T-Bills are represented by the Citigroup 3-Mo. T-Bill Index; U.S. Equities are represented by the S&P 500 Index; International Equities are represented by the MSCI EAFE Index; U.S. Small Cap Equities are represented by the Russell 2000 Index; U.S. Commercial Real Estate is represented by the NCREIF Property Index.

MSCI data may not be reproduced or used for any other purpose. MSCI provides no warranties, has not prepared or approved this report, and has no liability hereunder.

Russell Investments is the source and owner of the Russell index data contained or reflected in this material and all trademarks and copyrights related thereto. The presentation may contain confidential information and unauthorized use, disclosure, copying, dissemination or redistribution is strictly prohibited. This is GMO's presentation of the data. Russell Investment Group is not responsible for the formatting or configuration of this material or for any inaccuracy in GMO's presentation thereof.

1 Source: FAO 2011, Global AgInvesting Research & Insight Estimates 2012, Macquarie Agricultural Funds Management 2012.

2 Risk in this case reflects both volatility and other risks associated with farmland investing, which are addressed later in the paper.

3 Returns, standard deviations, and correlations are based on annual return series for each asset class. Annual total returns for farmland, timberland, and com- mercial real estate are based on linked quarterly returns, including annual property valuations; annual total returns for all other asset classes are based on linked monthly returns.

4 http://esa.un.org/wpp/Documentation/publications.htm

5 World Agriculture Towards 2030/2050: The 2012 revision (Summary) ESA E Working Paper No. 12-03 http://www.fao.org/economic/esa/esag/en/ 6 Source: USDA Amber Waves, February 2008.

6 Source: USDA Amber Waves, February 2008.

7 Organization for Economic Co-operation and Development.

Ms. Koeninger is the product strategist for timber and agriculture at GMO, LLC. She joined GMO in 2012 from her independent consulting firm, Farmland Advisor, LLC. Previously, Ms. Koeninger was a portfolio manager at Hancock Natural Resource Group, Inc. She earned her A.B. in English from Dartmouth College and her MBA from the Tuck School of Business Administration at Dartmouth College. She is a CFA charterholder.

Disclaimer: The views expressed are the views of Ms. Koeninger through the period ending July 2014 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security. The article may contain some forward looking statements.

There can be no guarantee that any forward looking statement will be realized. GMO undertakes no obligation to publicly update forward looking tatements, whether as a result of new information, future events or otherwise. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to securities and/or issuers are for illustrative purposes only. References made to securities or issuers are not representative of all of the securities purchased, sold or recommended for advisory clients, and it should not be assumed that the investment in the securities was or will be profitable. There is no guarantee that these investment strategies will work under all market conditions, and each investor should evaluate the suitability of their investments for the long term, especially during periods of downturns in the markets.

Copyright © 2014 by GMO LLC. All rights reserved.

© GMO