"Tired of lying in the sunshine staying home to watch the rain

You are young and life is long and there is time to kill today

And then one day you find ten years have got behind you

No one told you when to run, you missed the starting gun..."

From 'Time' by Pink Floyd

Who would have guessed in 1973 that Roger Waters' meditation on life's fleeting passage would describe the dilemma faced by many today as they consider how best to save for retirement? The good news is that missing the starting gun doesn't prevent you from joining the race. We have all seen the calculations of how big our nest eggs could be if we started saving and investing at a young age, but those unable to do so still have an opportunity to build substantial savings. And let's be honest; putting aside a few dollars in our 20s or even 30s can be a challenge. Unfortunately, the necessity remains. The temptation to rely on government is risky and almost certainly inadequate as our Chief Investment Officer Nicholas Kaiser recently wrote in detailing the various challenges facing the future funding of Social Security.¹

So what to do? We'll help you focus on retirement planning through 401(k)s, IRAs, or similar tax-deferred vehicles, as you consider the following:

1. Retirement ages are being pushed back, life expectancies are increasing, and investment horizons are extending further into the future;

2. Even if you have not been able to save to date, it's not too late to start; and

3. Given an extended time horizon, how are your assets best allocated within retirement portfolios, and how should you think about risk?

Retirement and Life Expectancy

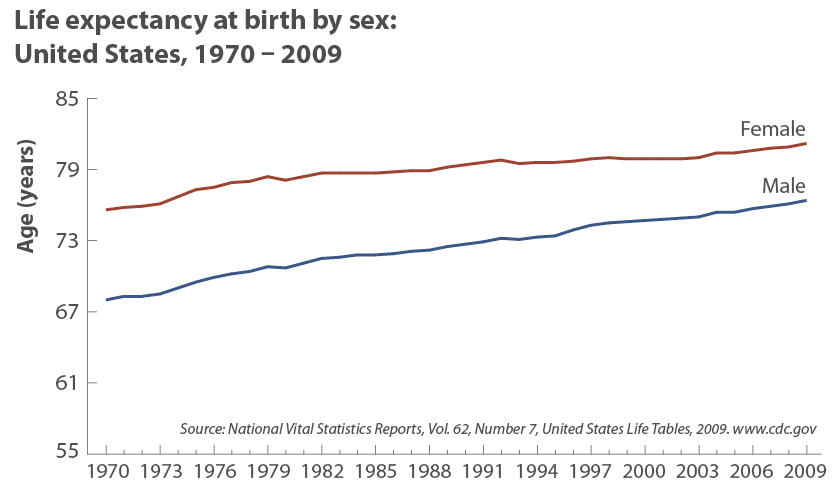

While the "full" retirement age to receive Social Security benefits has increased five years from 65 at the program's start in the 1930s to 70 today, it's likely to increase further.² A five-year increase in retirement age, however, pales in comparison to the rise in life expectancies over the same period. According to the Center for Disease Control, in 1937 the average life expectancy for both sexes and all ethnic groups in the US was 60. By 2009 it had risen 31% to 78.5.³

Living longer means you need to fund a longer retirement than in the past. If you are reading this report there's a good chance your life expectancy is even longer than average, meaning your investment horizon has been extended considerably. If you start saving in your 20s, you may have the benefit of investing for the next 70 years. This does not imply 70 years of capital appreciation since there will be a distribution phase, but even after you finish working you still need to grow assets if you are not to outlive your funds.

The Race Is Far From Over

The dictum to save early and often cannot be overstated. Nonetheless, maybe you did miss the starting gun. Perhaps you've even entered your fourth decade. Don't fret. You may still have 30 years of full employment, and your saving goals can be met if you start today, especially if you can take advantage of any 401(k) matching dollars offered by your company. At 50 it will be more difficult, and at 60 a possibly insurmountable challenge. Don't let your inability or lack of commitment to save in the past prevent you from doing so today and in the future. But we're not here to frighten you into action. Indeed, recent psychological research has demonstrated the existence of what has been termed the "backfire effect."4 Counterintuitively, we become more resistant to accepting a conclusion or taking action to change an outcome as the evidence becomes increasingly irrefutable or the future scenario being painted worsens.5 Don't think about the risks to Social Security or the uncertainty of having to rely on your children. Instead, envision the comfort of a secure retirement, the opportunity to take the long trip you've always dreamed of, or the freedom to study a topic of interest or to engage in a hobby or cause.

Asset Allocation Considerations

Now that you're saving we need to tackle another important issue: how best to allocate your capital among various asset classes. Today we are confining our discussion to various tax-deferred retirement saving vehicles such as 401(k)s and/or IRAs, which have some special characteristics. We've already covered the potential multi-decade investment horizon. Another consideration is that your retirement assets generally cannot be accessed until age 59½, while withdrawals may be deferred until age 70.6 This leaves you with a long-term portfolio you will likely not tap until you begin to draw retirement income. Common sense dictates your goal should be to grow the assets as much as possible.

Three Risks

Most people think of risk as the chance of something bad happening. If you leave your car unlocked with the keys in the ignition, you risk it being stolen. Investment portfolios are often viewed the same way — as if it were possible to lose everything. If your portfolio consists of investments in friends' restaurants and oil wildcatting schemes, the risk of total loss is indeed real. When speaking of investing in stocks and bonds that comprise major market indices, however, the risk of total loss is vanishingly small. Therefore, when discussing retirement savings, "risk" refers to the volatility of your investments or the day-to-day rise and fall in value. While a decline in the value of your portfolio is generally considered bad, the long history of investment experience teaches us that such declines are temporary. They may be significant and they can be wrenching, but the market has always recovered. Undoubtedly, the 56% fall in the S&P 500 from the peak in 2007 to the bottom in early 2009 was painful, but the 178% gain in the index since that time has provided a soothing balm. With that in mind, there is another type of risk to be considered — the risk of losing purchasing power.

If I Had a Dollar…

We all know about inflation; it costs more to buy something this year than it did last year. After all, a piece of paper with George Washington's picture has no intrinsic value; it's only worth what you can buy with it. Inflation may not always be dramatic but it's constantly eroding the value of your money. If you stuck a dollar bill in a drawer 100 years ago it would be worth about 4¢ today. That's why Warren Buffet, arguably the world's greatest investor, calls cash the riskiest asset you can hold.7 No one wants a dollar saved today to be worth a fraction of a dollar in retirement. Protecting your purchasing power requires "real" (after-inflation) investment returns.

Are You a Long-Term Investor? Stocks Win

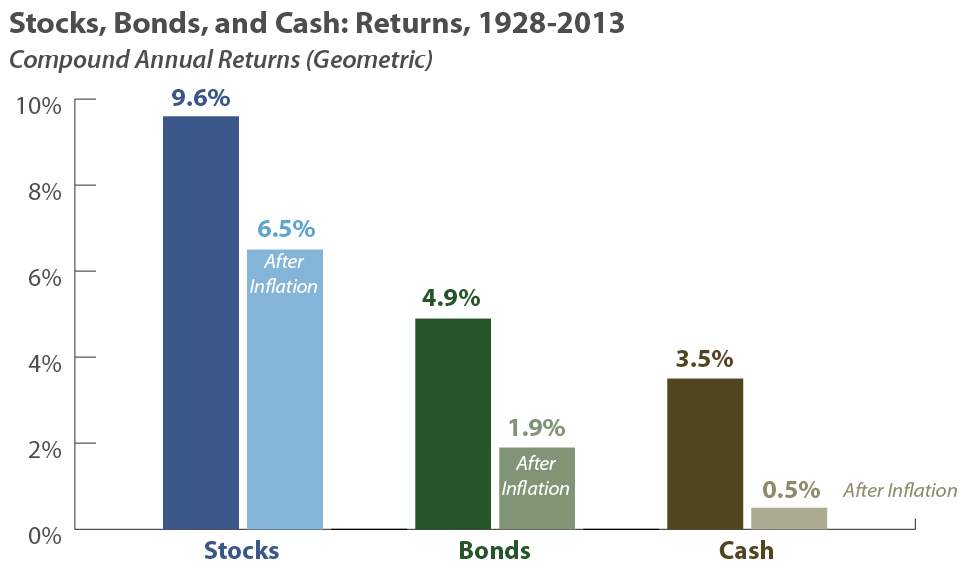

Sources: Saturna Capital, Federal Reserve Economic Data (FRED), Aswath Damodaran (New York University). This illustration is for educational purposes only and is not meant to be indicative of any particular investment nor does it provide an adequate basis for making an investment decision. Returns assume reinvestment of dividends and do not account for any transaction costs. Stocks are represented by the S&P 500. Bonds are represented by 10-year maturity Treasury bonds. Cash is represented by three-month maturity Treasury bills. Inflation is represented by an average national historical inflation factor of 3%.

Over long periods stocks have provided better returns than bonds or cash. Keep in mind that the stock return figures at right include the Great Crash of 1929, World War II, the October 1987 crash, the Dot-Com bust, and the most recent crash in the market during 2008 and early 2009. Even so, the stock market has outperformed other asset classes. While most people don't invest with an 85-year horizon, if you are 25 years old you will be investing for the next 45 years before you retire. That's important because bonds can out perform stocks over extended periods, but it becomes less likely as your investment horizon lengthens. Since 1928 stocks have outperformed bonds 73% of the time over all five-year periods, 83% of the time over 10-year periods, and 99% of the time over 20-year periods. Put another way, assuming the average after-inflation returns for the stock and bond markets continue, $10,000 invested in the S&P 500 Index today will be worth $66,650 in 30 years from now. The same amount invested in the bond market would be worth $17,637, although, even that is unlikely should today's low interest rates persist.

It's Tough Out There for Bonds

Over time bonds have provided lower returns than stocks, a situation that may be exacerbated by today's historically low bond yields. It would be difficult to assemble a bond portfolio yielding even 5% without submerging deeply into junky waters. Today the highest rated junk bonds (non-investment grade, rated BB and lower) offer a generic yield of only 4.24%8 so to achieve a higher nominal yield than that you have to dive deep indeed. Now your risk starts to resemble more closely that restaurant investment we mentioned earlier. If we stick with the safety of government-issued debt, the current yield on the US Government 10-year Treasury bond is 2.55%. Meanwhile, the pricing of Treasury Inflation Protected Securities (TIPS) indicates an expected inflation rate of 2.3%, leaving a paltry 0.25% annual real return.

But Bonds Do Have a Role

Stocks can decline quickly and significantly, as the multiple crashes listed above attest. So, as you near the time you will start making withdrawals from your 401(k), prudence suggests increasing your exposure to bonds, which are less likely to lose value over shorter periods and where your initial investment is protected. If you started investing at a young age and did well, you might even be able to live off the income from bonds in your portfolio.

Now That I Know More About Risks and Return, How Do I Invest?

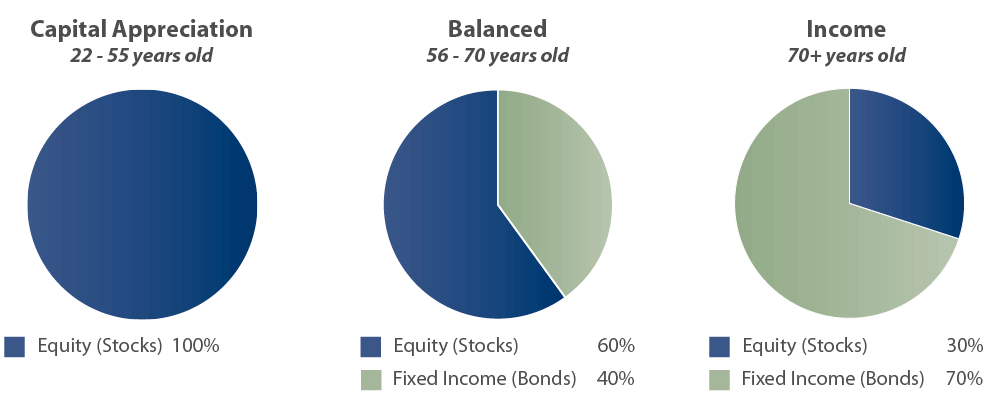

Traditional asset allocation often followed the "investor psychology" approach. Are you conservative, aggressive, or somewhere in between? We prefer to focus on your investing time horizon. In other words, are you:

- Young and focused on growing the value of your retirement portfolio;

- Approaching retirement and concerned about protecting the value of your portfolio; or

- Fully-retired and looking to live off income generated by your portfolio?

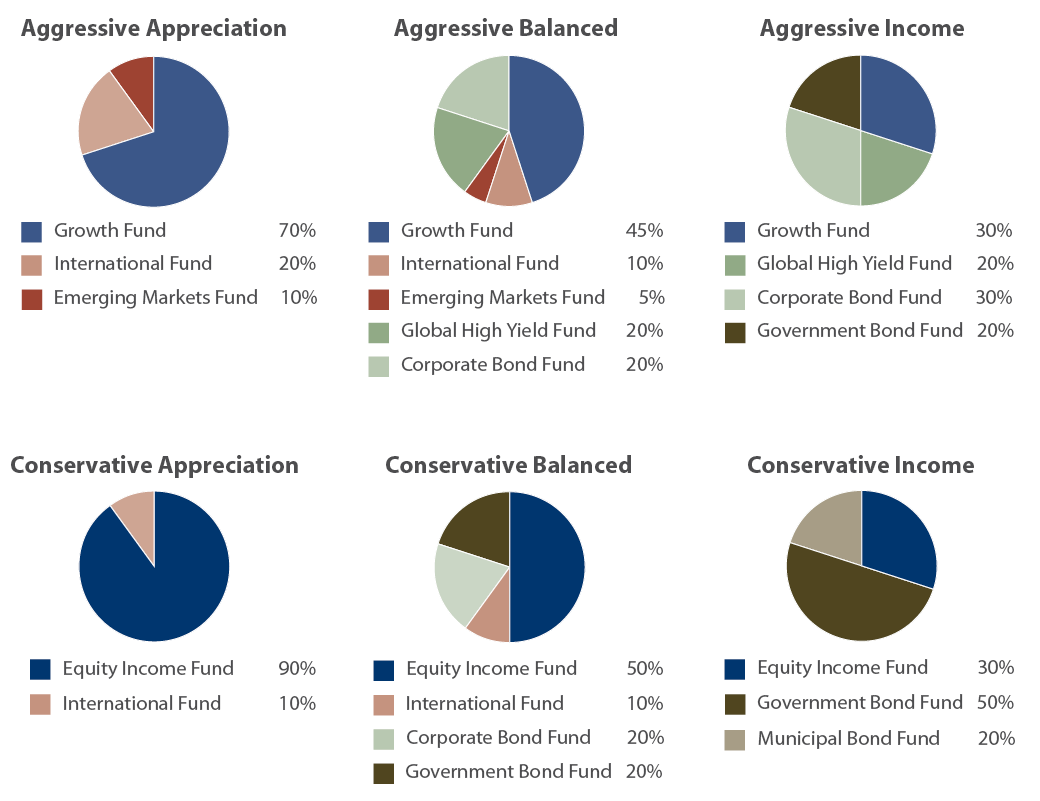

Investor psychology still has a role to play. If you are young and aggressive, you may include growth, international, or emerging market funds in your portfolio. If you are more conservative, you may invest solely in large capitalization domestic equity funds. If you are an aggressive person approaching retirement, you might employ a global high-yield fund that invests in high-dividend-paying equities as well as below-investment-grade bonds – a more volatile strategy than government bonds but one that may provide higher returns. Finally, if you are retired, depending on your life expectancy, you could employ a variety of bond strategies to meet your income requirements, including government bonds, corporate bonds, or tax-advantaged municipal debt.

Conclusion

The message we're attempting to convey is that investors often view risk from the wrong perspective. Your greatest risk is the erosion of your purchasing power, not the ups and downs of your portfolio. We have nothing against cash as a short-term allocation. If you're planning to put a down payment on a house in the next couple of months, go ahead and hold the money in cash. Financial advisors typically recommend keeping an emergency fund in cash or near-cash instruments that can cover your needs for six months. If your retirement account is large and you are able to comfortably live on the income generated from a bond portfolio, go ahead and do it. If, however, you have a multi-decade investment horizon and you wish to build wealth, history tells us equities are the way to go.

Footnotes

¹ Kaiser, Nicholas. "Recalibrating the Retirement Clock: Should 75 be the new 65?" From The Yardarm, March 2014. http://www.saturna.com/fromtheyardarm/2014_03.shtml

² While the Social Security defines full retirement age as 67, retirees receive maximum benefits at age 70. See Social Security Quick Calculator at www.ssa.gov.

³ Arias, Elizabeth. "United States Life Tables, 2009." US Department of Health and Human Services, Centers for Disease Control and Prevention, National Vital Statistics Reports, Volume 62, Number 7, January 6, 2014. http://www.cdc.gov/nchs/data/nvsr/nvsr62/nvsr62_07.pdf .

4 The Skeptic's Dictionary. http://www.skepdic.com/backfireeffect.html

5 Feinberg, M. and Willer, R. "Apocolypse Soon? Dire Messages Reduce Belief in Global Warming by Contradicting Just World Beliefs." http://www.motherjones.com/files/feinbergwiller20112.pdf

6 There are exceptions, such as withdrawing for a first home, for college tuition, or to meet major medical expenses. Plan participants may also borrow from a 401(k).

7 Alling, Jessica. "Warren Buffett Says This Is the Worst Investment You Could Ever Own." The Motley Fool, January 12, 2014. http://www.fool.com/investing general/2014/01/12/warren-buffett-says-this-is-the-worst-investment-y.aspx

8 FRED, Federal Reserve Economic Data, St. Louis Federal Reserve Bank, FRED, BAML US High Yield BB Effective Yield. http://research.stlouisfed.org/fred2/data/BAMLH0A1HYBBEY.txt

Copyright 2014 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 8 · No. 7

Saturna Capital publishes From The Yardarm Market Commentary & Analysis monthly. To subscribe, click here.

Saturna Capital does not share subscriber information with third parties.

Important Disclaimers and Disclosures

This report is intended only for the information of the reader and is not to be used for or considered as an offer or the solicitation of an offer to sell or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries or affiliates ("Saturna"). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any other service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied, or distributed to any other party without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks, and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable, and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will change over time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials, including any containing materially different information, are brought to the attention of any recipient of this report.

Under no circumstances shall Saturna, its employees, or any affiliate be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to making any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal, or accounting advice. Investors should consult their own tax, legal, and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of US federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing, or recommending to another party any transaction or matter discussed herein.

The Dow Jones Industrial Average is a price-weighted index of 30 of the largest, most widely held US stocks. The S&P 500 is an index comprised of 500 widely held common stocks considered to be representative of the US stock market in general. The Russell 1000 Growth index is a widely recognized index of large-cap growth stocks. The Russell 2000 Index is comprised of US small cap stocks and measures the performance of the 2,000 smallest US companies in the Russell 3000 Index. The NASDAQ Composite index measures the performance of more than 5,000 US and non-US companies traded "over the counter" through the National Association of Securities Dealers Automated Quotation system. The MSCI EAFE Index, produced by Morgan Stanley Capital International, measures the equity market performance of developed markets in Europe, Australasia, and the Far East. The MSCI Emerging Markets Index, produced by Morgan Stanley Capital International, measures equity market performance in over 20 emerging market countries. Barclay's Capital US Aggregate Bond Index measures the performance of the US bond market. The BofA Merrill Lynch (BAML) US High Yield Index tracks the performance of US-dollar-denominated below-investment-grade corporate debt publicly issued in the US domestic market.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price for, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuations that may have a positive or negative effect on the price or income of such securities or financial instruments. Investors in securities such as American Depositary Receipts — the values of which are influenced by currency volatility — effectively assume this risk.

Please consider an investment's objectives, risks, charges, and expenses carefully before investing. To obtain this and other important information about the Amana, Sextant and Idaho funds in a current prospectus or summary prospectus, please visit www.saturna.com or call toll free 1-800/SATURNA. Please read the prospectus or summary prospectus carefully before investing.

The Amana, Sextant and Idaho Tax-Exempt Funds are distributed by Saturna Brokerage Services, member FINRA /SIPC. Saturna Brokerage Services is a wholly-owned subsidiary of Saturna Capital Corporation, adviser to the Amana, Sextant and Idaho Tax-Exempt Funds.