Like two veteran poker players sitting across the table from each other, the Federal Reserve (Fed) and the bond market remain at odds. The Fed at one side of the table is careful about what it says and tries not to send the wrong signals, so the bond market will play its cards right. On the other hand, the bond market can develop its own interpretation of the Fed’s strategy, as has been the case in 2014 so far with the rise in bond prices and decline in yields. This week’s Fed meeting is unlikely to resolve the differences -- both may check -- but a host of top-tier economic reports may sway the course of play.

At the conclusion of the June 17 – 18, 2014 Federal Open Market Committee (FOMC) meeting, the Fed continued to forecast an average overnight borrowing rate of 1.1% for year-end 2015 and 2.5% for year-end 2016. Futures continue to indicate the bond market believes the Fed does not have an ace up its sleeve and that ultimately the central bank will not raise rates as high as it has indicated. Fed fund futures show the bond market is pricing in overnight borrowing rates that are 0.3% and 0.7% lower than the 2015 and 2016 year-end rates forecast by the Fed, respectively [Figure 1].

There will be no forecast update or press conference following this week’s Fed meeting, suggesting an uneventful outcome. The June 2014 meeting statement contained few changes compared to the April 2014 statement, and the Fed may likely stick to that course. Changes to the Fed’s opinion of the economy, labor markets, and inflation will be closely scrutinized. However, it seems the September Fed meeting, which will be followed by a press conference and updated economic forecasts, may prove more of a market mover for bond investors.

The Inflation Card

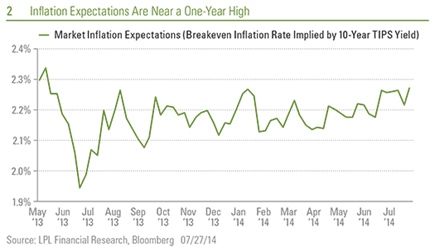

The bond market and the Fed have differing views on when the inflation card may be played. In her latest public remarks in early July 2014, Fed Chair Janet Yellen voiced concern over the lack of pricing power in the economy and a lingering risk of deflation. Yellen’s continued dismissal of the rise in inflation indexes in recent months was viewed as a bit complacent by the bond market. A Fed that may be slow to recognize inflationary pressures led to higher inflation expectations. The implied “breakeven” inflation rate indicated by the yield of the 10-year Treasury Inflation-Protected Security (TIPS) increased to nearly a one-year high [Figure 2]. Inflation expectations remain low when viewed over a longer-term context, but market and Fed views are slowly diverging.

Influential Player

Economic data is a player at the table and may hold greater influence. It is rare when a Fed meeting coincides with top-tier economic data such as the monthly jobs report, the Institute for Supply Management (ISM) survey, and a first look at second quarter economic growth (see this week’s Weekly Economic Commentary: Midsummer Madness) all in the same week. Together, this week’s three key reports may shed light on two important topics: 1) the strength of the economic rebound during the second quarter; and 2) the pace of economic growth early in the third quarter. The extent to which this set of reports exceeds or falls short of expectations may help determine the path of bond yields.

The 30-year Treasury has retraced 62% of the taper tantrum rise, as of July 24, 2014 [Figure 3]. Retracement levels of 50% and 62% have proven resistance levels in the past.

Additional economic weakness is likely needed to justify lower yields, since the lower yields already reflect questionable economic growth. Conversely, data showing that economic growth is on track at a 3% pace again in the third quarter may push yields higher as it keeps 2015 Fed rate hikes on the table and fosters expectations of a slight increase in inflation. Our play is that much of the news about a sluggish economy is already priced in and expensive valuations leave the bond market vulnerable to weakness.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-294427 (Exp. 07/15)