STOCKS FALL MOST SINCE 2012

Equity markets closed out July in negative fashion last week, plunging more than 2% on the final day of the period. For the month, both the S&P 500 and Dow Jones Industrial Average were down 1.4%. Bonds also lost ground as the BarCap U.S. Aggregate Bond Index lost 25 bps. Last week’s 2.7% loss in the S&P 500 was the worst weekly return since June 2012.

The Federal Reserve avoided surprises in its regularly scheduled FOMC meeting on Tuesday and Wednesday. The group further reduced its quantitative easing program by $10 billion a month, while leaving the Federal Funds rate unchanged at 0-0.25%. Janet Yellen did not address the media following the policy update, but the FOMC release did indicate a few minor shifts in language. Regarding the labor markets, the Fed indicated that they remain concerned around the robustness of the labor recovery, despite improvement in the unemployment rate. They also noted that inflation has moved closer to their long-term target.

It was a big week for economic data, with major reports including nonfarm payrolls, the initial estimate of second quarter GDP, and the ISM Manufacturing index hitting the newswires.

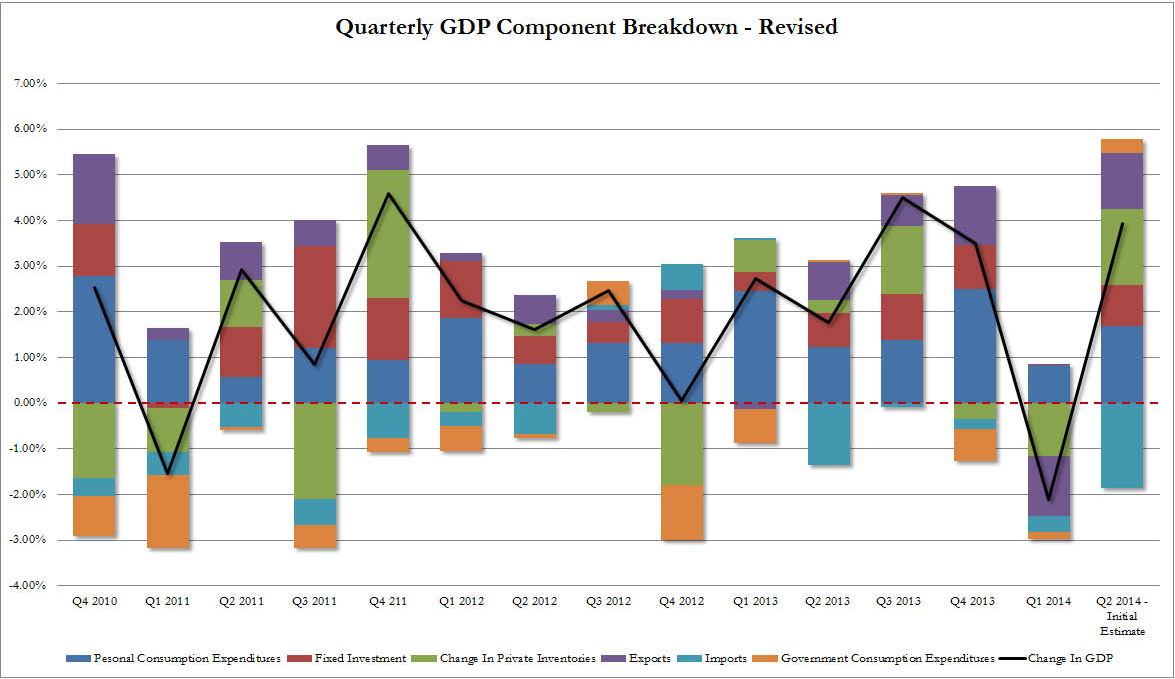

Second quarter GDP came in well above expectations, increasing at an annualized rate of 4.0%. The Bureau of Economic Analysis, who compiles the data, also released revisions for the prior three years. The revised data indicated that 2013 and the first quarter of 2014 was better than previously thought, while 2011 and 2012 were weaker than first estimated.

Source: J.P. Morgan

Growth was broad-based, with an increase in personal consumption expenditures, private inventories, and exports overcoming a larger headwind from imports. Government spending – driven at the state and local level – was also a significant positive contributor for the first time in two years. Overall, the data was encouraging and reflective of a strong rebound from a weather-afflicted first quarter contraction.

Source: zerohedge.com

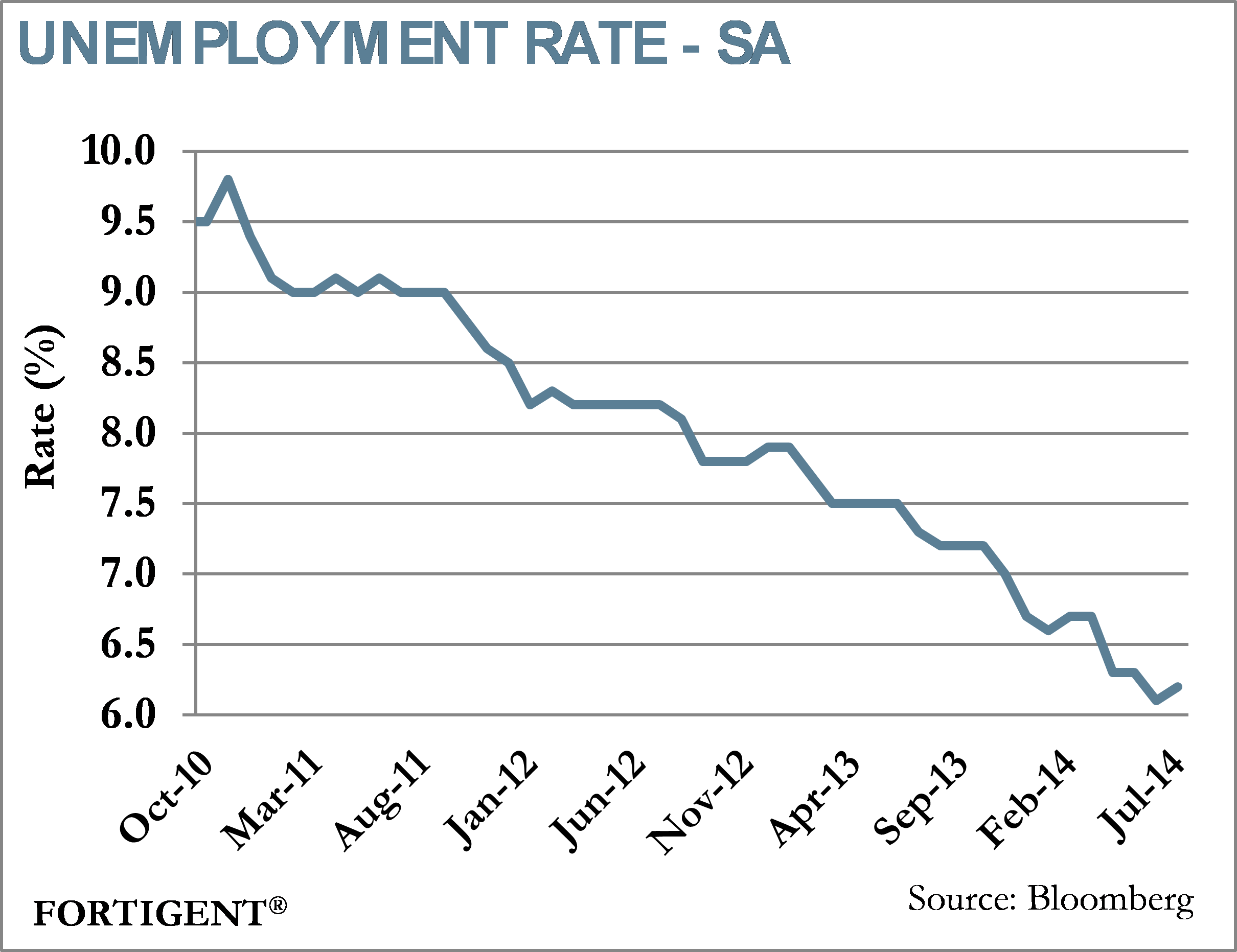

On Friday, the government jobs report came in below expectations; however, at 209,000, nonfarm payrolls posted their sixth straight month of gains above 200,000. That is the longest such streak since 1997, and has added to improving sentiment about U.S. labor markets.

The composition of job gains was encouraging, with robust increases observed in manufacturing and construction. Professional & business services were the largest source of jobs, adding 47,000 to payrolls. A smaller proportion of those gains came from temporary help services, which is typically a lower quality source of employment for the economy.

The unemployment rate edged up to 6.2%, following its rapid six-tenth drop between March and June. The labor force participation rate ticked higher by one-tenth of a percent. An alternative measure referred to as “underemployment,” which measures traditionally defined unemployed persons along with marginally attached workers and part-time workers who prefer to be full-time, also edged up to 12.2%.

Finally, the ISM Manufacturing Index reached a three-year high in July with a reading of 57.1. This was more than a point above expectations and indicates the U.S. manufacturing sector is expanding at a robust pace. New orders increased by 4.5 points to 63.4, while the employment component of the index gained 5.4 points. Production improved by a more modest 1.2 points, but remains above 60. According to the release, comments from the survey’s respondents were “generally positive, while some indicate concern over global geopolitical situations.”

BANCO ESPIRITO SANTO: OPPORTUNITY FOR THE ECB?

Over the weekend, it was announced that Portugal’s Banco Espirito Santo (BES) would be split into a ‘good bank’ and ‘bad bank.’ This came after the Bank of Portugal assured that BES could raise enough money from private investors to recover from the bank’s first-half loss of €3.58 billion.

Following the announcement, junior bonds sold off and the bank’s shares fell another 40% Monday morning. This is compounded by a year-to-date loss of over 88%.

Source: Bloomberg

The Bank of Portugal’s plan to rescue the bank, known as the Resolution Plan, involves splitting the bank into two: BES and Novo Bank. BES will remain the ‘bad bank’ housing shareholders and subordinated debtors. They will write down the bad assets, which are made up of exposure to the rest of Espirito Santo and all toxic assets included in the bank’s Angolan unit. This bank will be shut down over time resulting in a possible full write down of shareholders and creditors’ capital. Nova Bank will be the ‘good bank’ housing branches, employees, deposits, and senior debts. The bank will eventually be sold in order to recuperate taxpayers’ money.

As part of the Resolution Plan, Novo Bank will be capitalized by €4.9 billion with €4.4 billion coming in the form of a loan from the Portuguese state and €0.5 billion in cash, which has been levied on the banking sector and previous bail out programs.

The timing could not appear to be more contemptuous as the European Central Bank (ECB) recently took drastic measures to promote growth and stability within the still battered Eurozone region. Benoit Coeure, executive board member of the ECB, came out following the bank’s policy decision stating, “The only way out is by investing.”

Following BES’ first half financial results, the ECB cut off loan access to the bank, putting the Portuguese government in this conundrum. Given investors’ reservations on investing in Europe due to inherent risks that remain in the European banking sector, one may think that the ECB would stop at nothing to fully rescue BES, safeguarding shareholders in a post-Lehman world.

However, given the mere size and influence that BES carries in Portugal and the Euro Area, the ECB may be using them as the example for banking policy going forward. As opposed to Lehman Brothers, BES, and Portugal in general, are a much smaller economic footprint in comparison. This provides the ECB with an opportunity to set precedent without the potential of economic ruin.

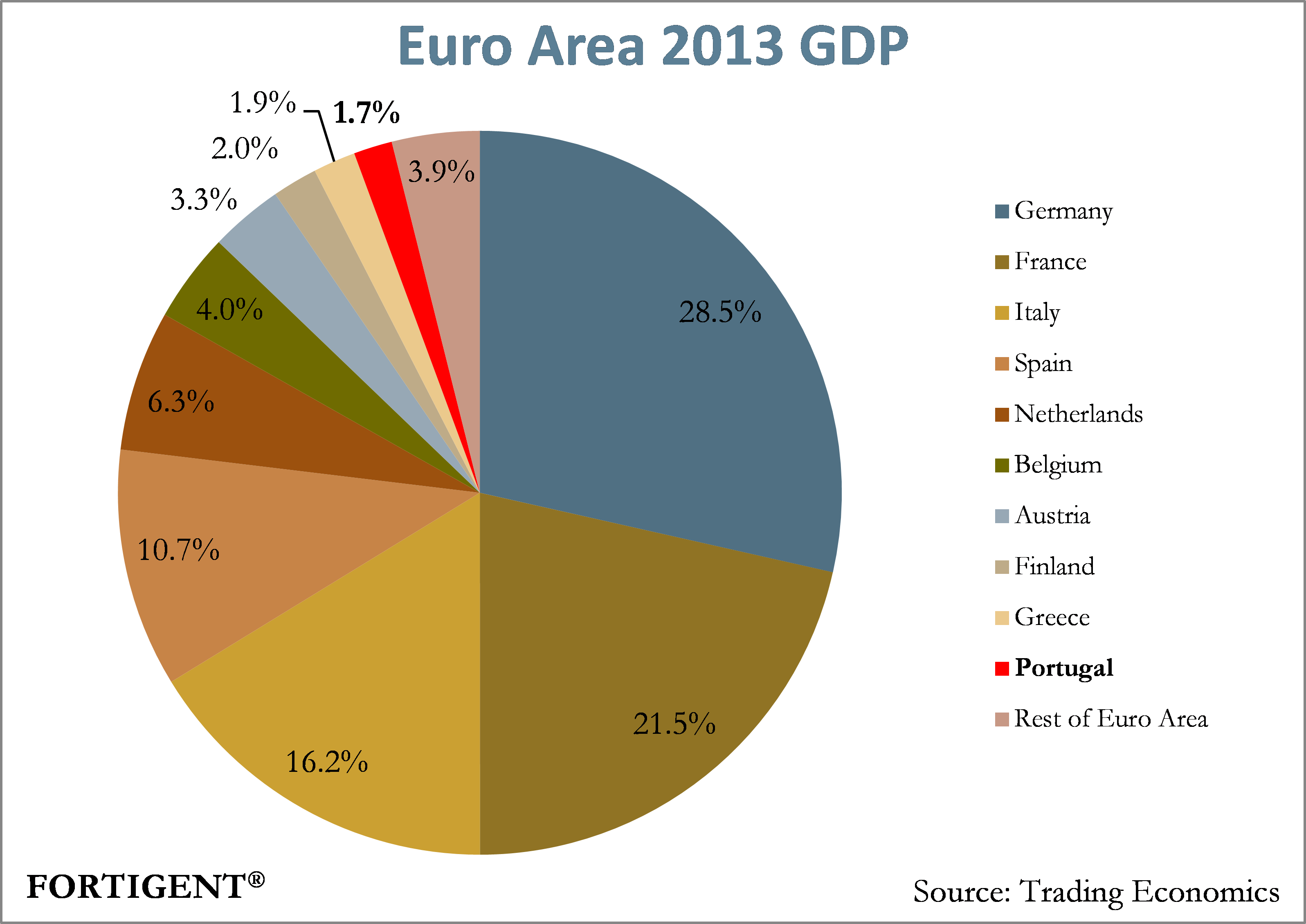

Portugal makes up roughly 1.7% of Euro Area total GDP (2013). Of Portugal’s $220 billion GDP, BES’ $100 million in assets make up less than 0.1%. While the extent of financial damage is yet to be fully determined, BES’ status in Portugal, and even more so the Euro Area, is nothing in comparison to Lehman Brothers, which filed for bankruptcy in September 2008 with $639 billion in assets and $619 billion in debt.

By placing the onus on investors, and not just taxpayers, when dealing with the fallout of a bank’s failure, the ECB’s effort in instilling investor confidence in the region remains to be seen. The objective was the same with Lehman when it was decided to let them fail in 2008. While size and impact of BES on the Euro Area region is less than that of Lehman on the U.S. and global markets, the decision will surely be more positive than in the case of the Lehman.

THE WEEK AHEAD

Economic data is relatively limited this week as the traditionally quiet August gets under way. This week, notable reports include the ISM Non-Manufacturing index, trade balance, and consumer credit.

Earnings season moves towards its conclusion with a med-heavy week of releases this week. This includes Walt Disney and Time Warner.

The European Central Bank meets this week amid softening economic growth and sagging inflation figures. Consensus does not expect major policy action at this meeting.

Separately, the Bank of England and Bank of Japan are set to hold their regularly scheduled policy meetings. Analysts do not anticipate changes announced from either venue. Emerging market central banks including Romania, India, Thailand, and Peru also meet.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value