Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

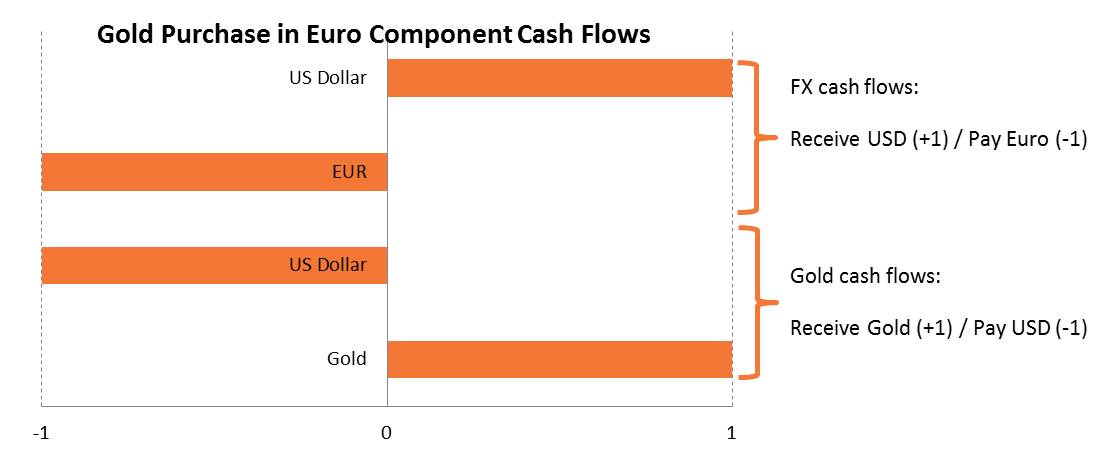

We are often asked how US based investors can construct a long position in gold that is financed in a foreign. In the discussion below we show the components of trade that gives an investor long exposure to gold that is financed with European euro. A useful way to understand how the portfolio would be constructed is to look at the cash flows associated with a gold transaction. Looking first at a gold transaction that is funded in dollars we show a diagram of the associated cash flows.

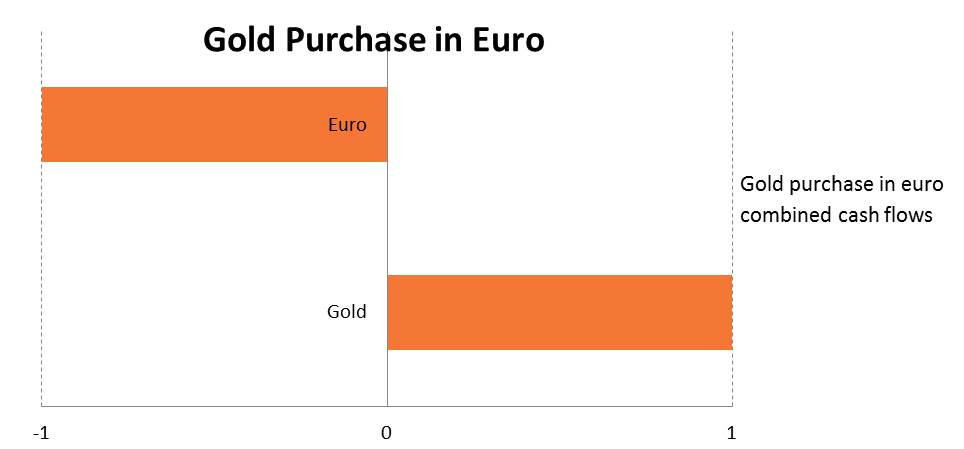

In a regular gold transaction the investor receives one unit of gold (+1) and pays one unit of dollars (-1). For a gold transaction financed in euro we must replicate the above cash flow but substituting euro for dollars. This is done by combining a gold purchase in dollars with an FX transaction where the investor sells euro and buys dollars. These cash flows are shown in the diagram below:

The two features to note are firstly that the asset position in gold is combined with a liability position in euro. The investor is expressing the view that they expect the price of gold to increase relative to the euro. When the euro falls in value on currency markets the value of gold expressed in euro will tend to rise. The second feature is that the dollar cash flows from the components net to zero and hence the investor does not have any direct exposure to the dollar.

The second feature is of key importance in the current environment where the relative monetary policies of the US Federal Reserve and the European Central Bank (ECB) are increasingly showing divergence. The Federal Reserve is close to ending its asset purchase program while the ECB is likely to launch its own asset purchase program in the coming months. For investors that hold gold financed in dollars, an environment of rising US interest rates and a stronger dollar will likely put downward pressure on the value of gold priced in dollars. One alternative for an investor that wishes to hold gold but has the view that the dollar may strengthen is to hold gold priced in euro. As shown in the cash flow diagram the investor is able to get long asset exposure to gold while at the same time avoiding expressing a direct view on the future value of the dollar. Further the euro may be an attractive funding currency to consider in the current environment given the growing divergence in the monetary policy stances of the Federal Reserve and the ECB.