I turned to look but it was gone

I cannot put my finger on it now

The child is grown,

The dream is gone.

I have become comfortably numb.

Pink Floyd

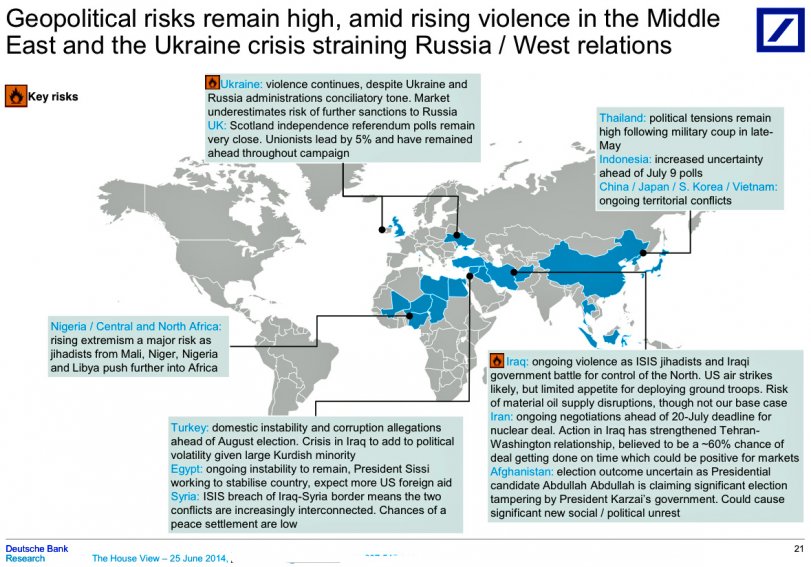

On Thursday, July 31st, the market had a one-day sell-off of 2%, the most negative day since June, 2012. You heard the market pundits and the talking heads of CNBC opine that the reason for the selloff was the convergence of geopolitical risks:

- Increased tensions between Western governments and Russia, exacerbated by the events of the last two weeks in Ukraine; additional sanctions forthcoming.

- The escalating conflict between Israel and Hamas in Gaza that is beginning to be a catalyst for a larger Muslim versus Judeo-Christian conflict in the Middle East.

- Argentina’s “technical” default on debt payments. This is the ninth such default since Argentina first issued bonds in 1824; nothing new here other than a hedge fund and a judge.

- The largest Ebola outbreak ever in Africa, which put health authorities across the globe on high alert.

- The renewed “contagion risk” that a Portuguese bank imposes on the rest of Europe if it defaults.

- The attempt of ISIS in Iraq to install a caliphate that would impose Sharia law on the territories it controls, thus allowing Abu Bakr al-Baghdadi to rule with the same sort of dictatorial hand Saddam Hussein (and you thought he was a bad guy) wielded for twenty-four years. All in the name of Allah, of course.

While all of these are valid concerns and could be viewed as reasons for a stock market decline, I contend that they had very little effect on investors, save those trading in the oil markets.

Thirty-four years ago when I began my career, any of these geopolitical risks would have been enough to send the markets into a temporary tailspin. There was no CNN, Twitter, Facebook, or smart phones to keep the ills of the world constantly on our minds. We had Walter Cronkite, with his memorable signoff, “And that’s the way it is,” to inform us of geopolitical events, and without the graphic camera footage we see today.

In today’s world we drink global news events from the fire hoses of smart phones, 24-7 television coverage from multiple networks, blogs, Twitter, Facebook, and various other media. The constant barrage of horrors inflicted by human beings on other human beings, graphically reported by a widening array of media over the past fifteen years, has, in my opinion, ultimately served to numb investors and the public at large. We’ve had to digest those horrors and fold them into our understanding of how the world works. I am never amazed anymore at how ready and willing some are to take lives in their struggle against whatever supposedly oppresses them, whether their reasons are political, economic, or religious.

The face of war changed after the fall of the Berlin Wall in 1989. It is possible to wage war strategically against an enemy nation that poses a defined target, but decentralized terrorist groups such as Al-Qaeda can orchestrate conflict by means of vast numbers of cells scattered across Africa, the Middle East, and – lest we forget 9/11 – here in the USA. How do you fight a war where the enemy is constantly shifting and hard to find? I wrote in 2013 that we live in a G-zero world where we lack any one government’s leadership to prevent continued destruction. Russia flexing its muscle in Ukraine, China and Japan fighting over territory in the East China Sea, everyone fighting everyone else in the Middle East are just examples of our new world order. But to make the leap from global tensions to market sell-offs is a big jump; after all, these events have been going on for some time.

The market sell-off last Thursday, in my opinion, had more to do with economic risks presented by the end of Fed tapering and the possibility of higher interest rates. If you assess the likely impact of the Fed’s tapering course, keeping in mind the fact that we have not experienced a market correction of more than 10% since 2011, then predicting some type of correction in 2014 was a pretty safe bet at the first of the year.

In April’s letter I wrote the following:

The Fed is currently purchasing assets and creating money at a rate of $55 billion per month. At the $20 billion mark tapering gets real; and as Dr. Fisher indicates, he anticipates QE3 to end sometime this fall. But will QE programs and Federal Reserve intervention ever truly end?

The markets have become addicted to their investment cocaine, and once the supply is cut off, then cold turkey withdrawal ensues. In my opinion, when the pain becomes too great and the powers that be start catching heat, then Dr. Yellen and Company will see their tapering plans torn up like a Walmart tent in a tornado.

The US is not in economic decline. We are still the most vibrant economy in the world, driven in the present era by increasingly abundant energy and game-changing technologies, including biotech and nanotech. And we are a country rich in natural resources, particularly farm land and water. Despite Washington’s efforts to curtail our progress with a badly functioning healthcare law, deterioration in our education system, and reluctance to reinvest in infrastructure, our government has yet to derail the train of corporate investment and small-business entrepreneurship. We are now in the 60th month of a recovery that compares to an average of 95 months for recovery periods over the past three decades. Admittedly this recovery lacks the robustness of recoveries past, but nevertheless we continue to “muddle thru” with positive results. The Achilles heel of our recovery has been the explosion of the Federal Reserve’s balance sheet following the 2008 crisis and runaway deficits due our dependence on government spending for economic stability.

It appears that Europe and the UK, while slowing, are also still in positive GDP growth territory. I have voiced concerns in the past over the need for a central bank for the euro. Whether EU countries have the economic fortitude to let Germany dictate terms for forming the equivalent of our Federal Reserve remains to be seen. However, the convergence in thinking between German Chancellor Merkel, ECB President Mario Draghi, and other European central bankers would lead one to believe Europe will continue its course towards the formation of a central bank. In the interim Europe’s economy will be without reform or recovery, but we will not see a Eurozone collapse or even another crisis. Whereas the US is “muddle through,” Europe is “stuck in the mud.”

So, if the developed nations’ corporations are continuing to grow earnings and interest rates currently remain low, then what could cause a correction in the market as initiated by July’s sell-off – or worse yet, a bear market? The answers:

- The China banking mystery

- Emerging market deleveraging and corporate restructuring

- Unintended consequences of the Fed’s tapering

China – What is Going On?

For one, there’s a new sheriff in town, and the Central Discipline Inspection Commission (CDIC) is not hesitating to remove high-level government and state officials under the charge of corruption. This strategy of using anticorruption sanctions is an effort to intimidate reform opponents within the party as China enters a new era of economic and political reform. To date, 33 high-level officials have been investigated for violating laws, the latest being Zhou Yongkang, formerly a member of the all-powerful Politburo Standing Committee and head of China’s security. People like Mr. Zhou were thought to be untouchable, but with his ouster President Xi has left no doubt as to who is ruling China. And with his power he is pushing reforms long overdue in order to sustain the government, reduce the power of the party, and implement banking and economic reforms while simultaneously consolidating governance at the top.

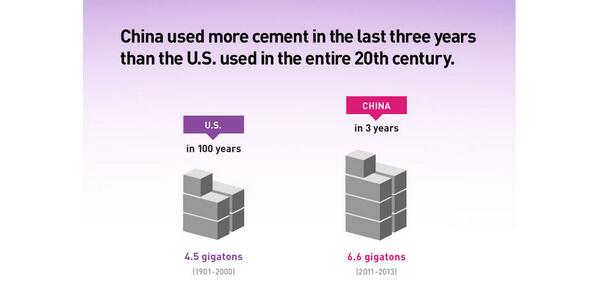

As for China’s economy, I must admit that the anticipated break down either by a loss of control in their banking system or social upheaval has not happened during the last decade of unprecedented growth. However, the lack of transparency of the Chinese financial system makes their role in the global economy suspect. The biggest risks to the Chinese economy lie in the financial sector, where government mandated construction projects and the need to employ millions of people have jeopardized bank solvency and raised the specter of defaults. Consider the following chart:

That’s a lot of cement!!! Where did it go and what was it used for? I have read articles about “empty cities” and watched 60 Minutes televise segments about entire towns full of thousands upon thousands of new apartments and condos where no one lives – ghost towns owned by middle class Chinese who, like US real estate investors, thought real estate was a safe investment because prices had never declined. The Chinese use their savings and borrow money to buy as investments not one or two but multiple apartment units that are not occupied. President Xi is being forced to reduce the moral hazard in the banking community and make clear what the central government is going to guarantee and what it isn’t. With more than $4 trillion in surplus, it is possible to proceed smoothly, although GDP will probably decline below the current 7.5% growth rate. The challenge is to prevent a consolidation of industrial production that eliminates jobs and to simultaneously avoid some form of financial crisis. Without a doubt there will be industries that go out of business, officials thrown in jail, and more government regulations forthcoming in attempts to negotiate a “soft landing” versus a “hard landing.” China is competing in the early innings of a ball game fraught with global consequences, and much of the trouble they face now and the risk they pose to the global financial system derives from a lack of transparency in their banking system.

Emerging Markets Restructuring

We used to say that if the US economy caught a cold, the rest of the world caught the flu. China, as the world’s #2 economy, has now reached a position where if it catches a cold, a large portion of the emerging markets catch the flu. Countries such as Brazil, Indonesia, Turkey, Russia, and others depend on China’s purchasing of their natural resources as a big part of their ongoing economies. Add to the potential China slowdown the fact that South Africa, Turkey, Indonesia, India, Colombia, and Brazil all face elections with no one party in a position to provide effective leadership, and you have the makings of a very bumpy ride in emerging market stocks in the near term. During the 1990s and 2000s, when the developed economies were expanding, the US provided the fuel for emerging market growth. Today that is no longer the case, as evidenced by the stagflation seen in many EM countries. Private-company debt has risen from an average rate of 14–16% to today’s 18-20%. Inflation in many of these countries is approaching double digits; and without the emergence of their middle class to stimulate consumption, many corporations will need to deleverage balance sheets and restructure debt. I see an opportunity here for firms such as KKR and the Blackstone Group to provide the capital needed to facilitate EM debt restructuring. We don’t own either of these companies, but they and other beneficiaries of emerging market debt restructuring are on our radar.

The Fed, Tapering and Government

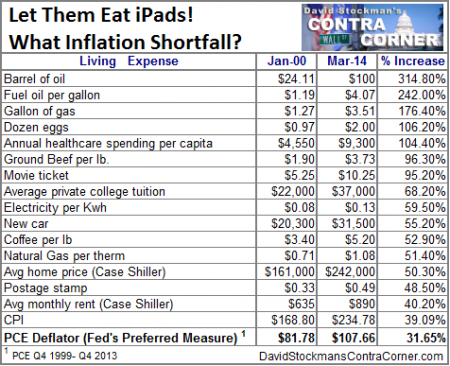

What about this chart doesn’t look right? Is it oil? Is it home prices? Or is it the CPI relative to real living expenses? I contend that since the crisis of 2008 the silent killer of purchasing power in the US has been the unseen hand of inflation that the Fed wields with its massive printing of money. Combine the past fifteen years of decreasing purchasing power with the Fed’s zero-interest-rate policy, and you get as an unintended consequence an economic system that robs the poor and gives to the rich. Maintaining interest rates at unprecedentedly low levels for an extended period of time has caused investors to take risks they ordinarily would not take. Investors have shifted from “safe” investments to riskier financial assets and real estate because they can earn little to nothing in “safe” investments.

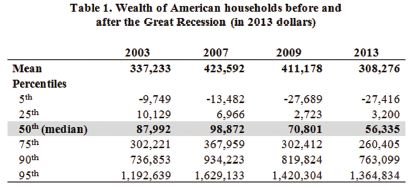

Some say stock prices are in a bubble; however, given the strength of earnings, dividend growth, share buybacks, a “muddle thru” GDP, and few if any alternatives to stocks, the market looks fairly valued to me. The average wage earner could not take advantage of the market move from 2009 to the present, and we see the effects in the chart below on the quintiles of wealth distribution in America. Continued Fed policies will continue to drive greater wealth to the top 5%, who already own the majority of the investable universe. The middle and lower classes will continue to become poorer.

The chart above shows that every income group still lags behind where it used to be, on average. The top 5% of households, for instance, have an average net worth now of about $1.4 million — but that’s still about 16% lower than in 2007. The top 10% have an average net worth of about $763,000, down about 18%. Yet that’s far better than the median household, which has lost about 43% of its net worth since 2007.

Summary

“May the odds be with you.” –The Hunger Games

As former heavyweight champion Mike Tyson put it, “Everybody has a plan until they get hit in the face.” I am not a Mike Tyson fan, but his point raises the question: what’s your investment plan? How do you manage risk in your investments? Do you have an investment discipline? How are you going to handle the market’s punching you in the face?

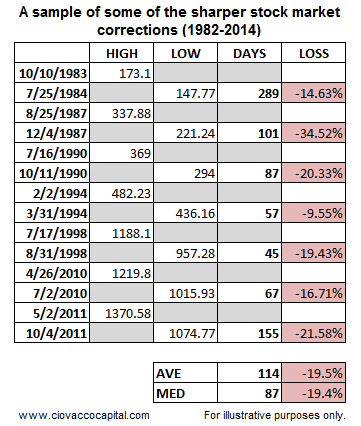

The following chart lists some of the sharper corrections from 1982 to 2014; now consider: what is your plan if the market declines 15-20% between now and year’s end?

I am not predicting that a market decline is certainly on the horizon; however, our asset allocation work at the end of June prompted us to raise our cash position from 4-5% to 11-12% during July. There is nothing cheap in the US large and small equity markets. Europe is enticing; but until Mario Draghi and the euro countries come to terms on a central bank plan, we will limit our exposure to the EU. Long-term we understand the need to participate in emerging markets, but given the risks posed by China, along with potential restructuring, we will be cautious.

We still recommend hard assets, particularly if Janet Yellen and company stick to their guns on tapering, as rising rates would appear to be the result of their actions. We include in hard assets oil and gas, mining, real estate, pipeline MLPs, and infrastructure. GDP will contiue to be the dominant fundamental for stocks, and a continued “muddle thru” environment would indicate more room to go on the runway of stock appreciation.

Because of the increasing odds of a market pullback and a possible disaster in the domestic bond market, we have increased our use of “liquid alternative” strategies in our portfolios. Institutional investment management tools are now available to smaller investors; and we can efficently gain exposure to mezzanine debt, private equity, long/short equity, long/short credit, and event-driven investment strategies. If you have not heard of liquid alternatives and are wondering how to utilize them to mitigate risk in your investments, then contact me and let’s get you up to speed on how these investments are defined and how they work.

“I’ve learned that people will forget what you said, people will forget what you did, but people will never forget how you made them feel.”

–Maya Angelou: April 4, 1928 – May 28, 2014

Good luck out there. Cliff

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Excelsia, Inc.), or any non-investment-related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Excelsia, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Excelsia, Inc. is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Excelsia, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

© Excelsia Investment Advisors