U.S. economy showing improvement

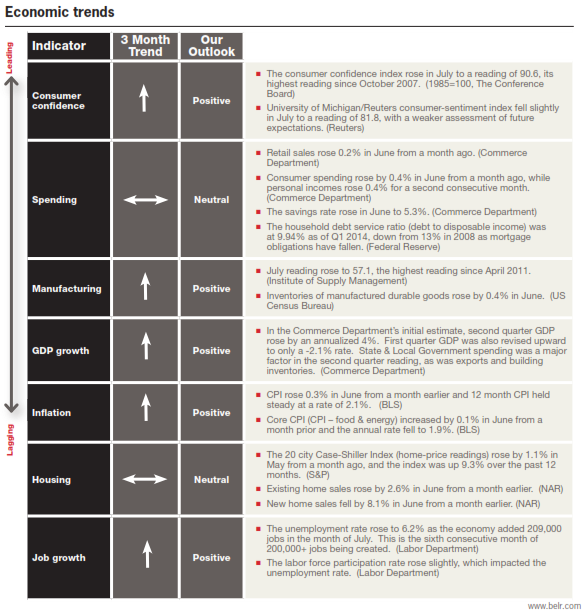

After a slow start to the year, the U.S. economy has bounced back strongly, with an initial estimate of 4% GDP growth during the second quarter. Strong signs from the manufacturing sector and six consecutive months of 200,000+ job gains have created a feeling of relative economic stability. The same cannot be said globally, however, as Europe continues to struggle with setbacks such as Italy falling back into recession. Geopolitical concerns are also weighing heavily on global growth and consumer confidence. Looking ahead, all eyes continue to be on the Federal Reserve and other central banks as businesses consider their future spending and hiring plans.

Bonds show relatively flat month in July

U.S. Treasury interest rates continued their gradual descent on the long end of the curve, but surprisingly began to push higher on government bonds with maturities of ten years or less. Investors digested a strong flow of positive economic information against the backdrop of expectations that the Federal Reserve will begin raising interest rates sometime in 2015. Aggressive areas of the fixed income market, such as high yield bonds, sold off during July after leading the bond market higher in the first half of the year. There continues to be pressure for interest rates to move higher, but adequate demand is keeping rates steady. With government bonds from countries such as Italy and Spain now paying a similar rate to the U.S., demand for Treasuries may not dissipate any time soon.

Stocks fall for first time in five months

The S&P 500 Index and the Dow Jones Industrial Average fell in July, fueled by a major decline on the last day of the month. Both indices ended the month in negative territory for the first time since January. Mixed second quarter earnings reports has helped fuel the recent spike in volatility and has some investors mulling a “stock correction”, as strong U.S. economic data could signal a faster pace for tightening of monetary policies. However, every short-term pull back thus far in 2014 has resulted in a rally that pushed the markets higher. It is difficult to predict when and if this trend will end, so it’s important that investors maintain their focus on their long-term investment objectives. While return expectations for 2014 are more muted compared to the last two years, a forward P/E ratio of 15.6x for the S&P 500 Index is in line with recent historic averages and may simply suggest more normalized rates of return for stocks going forward.

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2014 Bronfman E.L. Rothschild, LP